Agree with author’s views but given the sharp run-up in small caps w/o corresponding increase in earnings, any steep correction in markets may result in large caps with longetivity of growth and visibility of earnings a much safer long term compounding option.

It is softer things like these which reflect ‘Quality of Management’ towards business as part of the wider QGLP process for stock selection.

Three years ago, the promoters agreed to bring in the risk capital to ensure there is no impact on the ASL business. As a result, the control (of the e-commerce business) was with them so far. Now that we have got visibility around the cost structure in the future, ASL and its board is now confident about investing further in the business.

This deal was always on the horizon and was just a matter of time for it to happen. We now felt that it was an opportune time for the ASL promoters to transfer the balance shareholding in AEL thus making it a 100% subsidiary of ASL," he said, adding that additional stake in AEL is getting acquired from ASL promoters and promoter family.

Competition is healthy especially if your competitor is unhealthy and hopefully sick and absent during the competition.

I just love this guy. What brilliant thoughts on succession planning. Keep going KB. As long term investors in ASL, we need competitors like yourselves.

MOSL_FY’18_Q3 Update_Sell Call.pdf (298.0 KB)

DMART-25-1-18-PL.pdf (312.5 KB)

Sell calls are important to review as it forces you to challenge falling into confirmation bias trap.

3 Likes

Motilal Oswal Focussed 35 holds Dmart bought at a price of 1181 per share (116,699.00 shares bough for 13.79 Crores ) based on the holding details. Question is will they sell that holding based on their own call?

http://www.moneycontrol.com/mutual-funds/motilal-oswal-most-focused-multicap-35-fund-direct-plan/portfolio-holdings/MMO031

4 Likes

Good point. I however, prefer following rupee vest as it shows a more accurate dataset. Here, it sows that MOSL holdings has been intact at 333000 shares since IPO. Knowing their investment philosophy, they are desperately waiting (like many other DIIs) for price to crash so that they can accumulate a truckload as such investments fits perfectly into their QGLP framework.

The Fund (MOST Focused 35) is holding the shares from IPO month (March 2017). It is quite possible that the Fund Manager would be waiting for March to claim LTCG, and thereafter may sell. All other schemes of Motilal Oswal like MOST Dynamic Equity Fund, MOST Focused 25 and MOST Long Term Fund have already exited Dmart in June/Sept quarter. Since, the holding was comparatively smaller in the latter funds compared to Focused 35, STCG may have a greater impact on NAV, and hence the Fund Manager may have considered holding it for tax gains.

PS: An overall heat-map shows 76 schemes selling 2 lakh shares and 39 adding 1.3 lakh shares in the last quarter.

http://www.moneycontrol.com/mf/user_scheme/mfholddetail_sec.php?sc_did=AS19

while mosl has given a sell call with TP of 920,I feel that this stock will never come to such a low price, given its performance till date.Do these calls become an impediments in our decision making? Which of these analyst are most reliable to follow?

Depends on your time horizon Atul. If you have invested for 3-6 month horizon, then the current price +/-20% will be the range, but if you have invested for the next 3-5 years, then such short term calls shouldn’t bother you unless fundamentals deteriorate substantially, which I doubt will be the case.

Is STCG applicable for mutual funds? Buying and selling are part of their business and their taxes are based on the profits. So I don’t this logic is correct.

Thanks for raising this @chandrasekariy_

I may be wrong, but, in my opinion the FMC charged can be considered business income for MFs but not the profits from buying/selling scrips. Since, MFs are in nature of a trust with accumulated funds from individual/HUF/institutional investors, the gains on selling scrips should be considered income for the investors.

Do share your understanding if you have deeper knowledge on the subject. At my end, I would be checking with my CA friends to understand the tax implications on MFs more precisely.

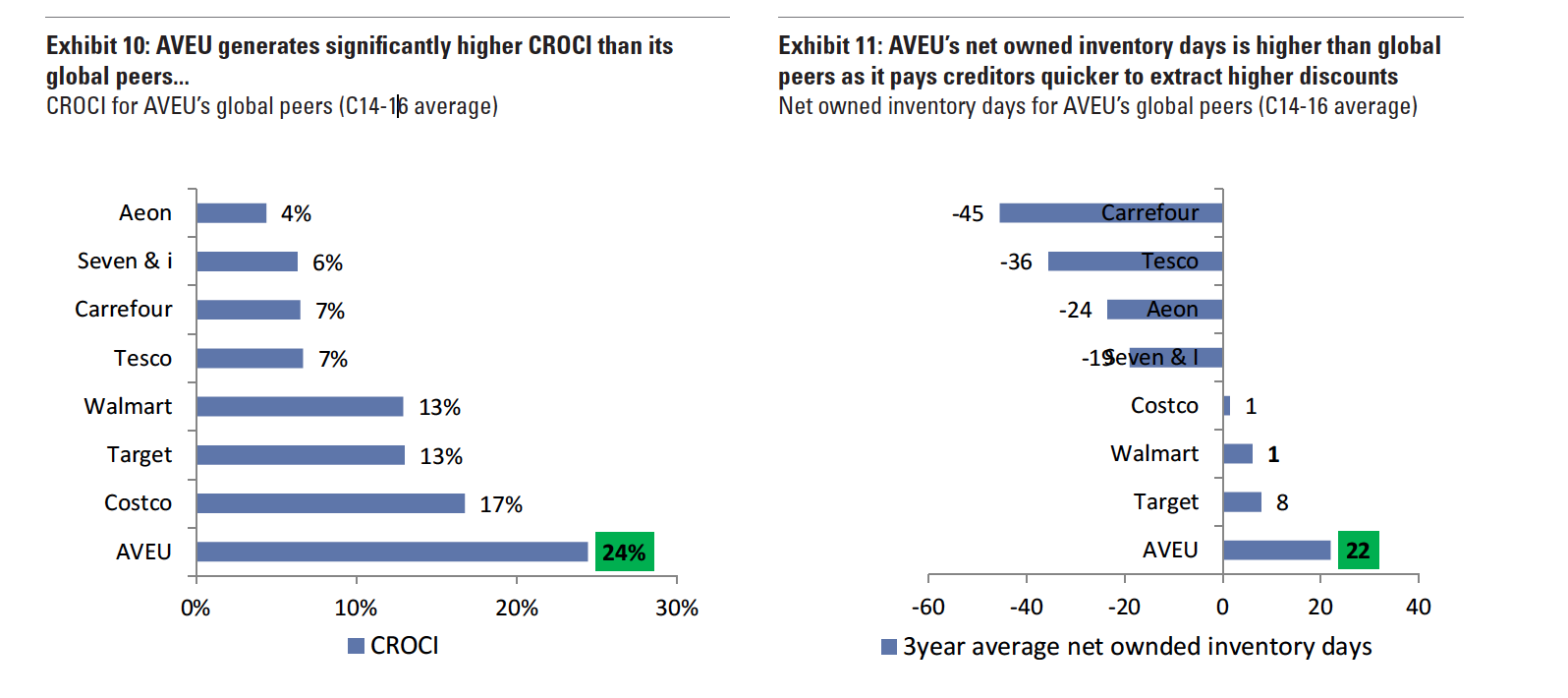

As I understood,the investor days of avenue supermart are higher than the upper ones even though it pays efficiently.Is it not negative when compared to peers ?Or my understanding is incorrect.can u clarify?

Unsure if its negative / positive. Inventory Days are higher than global peers ( but lesser than the indian peers as per the same GS report). This is being justified in the report as due to early payment to creditors. If you paid for your inventory only a day before you sold it, you effectively held the inventory only for a day and hence your funds were tied up only for 1 day. But since you paid right when you bought the inventory , the money to buy that is tied up for more days , until its sold. Though it seems like paying your creditors later than earlier is common business practice , but DMart has chosen to do the opposite to extract the discounts when buying inventory (as per the report).

1 Like

Can u pls share the full report link, tnx

2 Likes

Its already there on this thread.

1 Like

Many thanks…