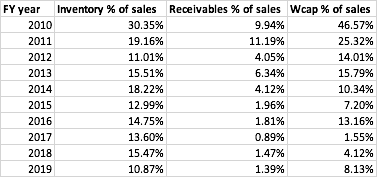

Their working capital has gone up because of increase in inventory (and not receivables). However, the numbers are broadly in historical range. [Numbers are below]

The way I deal with mismatch in CFO & PAT is I consider cash earnings as real earnings and do my valuations based on that (rather than accounting/accrual earnings).

Look at cumulative CFO over the last 7-10 years and compare it with cumulative profits. If its > 90% I use reported earnings as cash earnings. If thats not the case, I take CFO as real earnings and do my valuation based on CFO. In the case of Avanti, CFO ~ 80% reported earnings over the last decade.

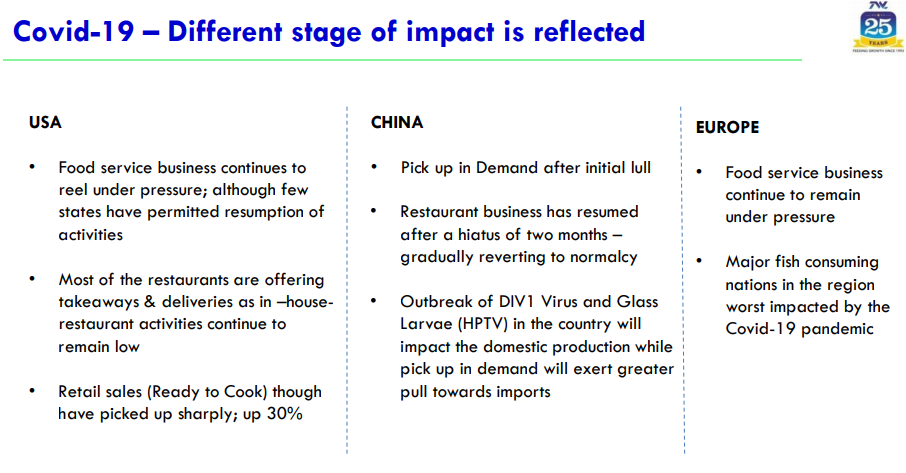

Heartening fact in the numbers is that despite news in public through March that virus first cases originated from a sea food market in Wuhan, China, exports to US didn’t see a major drawdown. Clearly, shrimp consumption pattern remain unchanged in the US during March against expectation of a complete washout. Although, not a guarantee that robust exports from India will continue in following months due to rapidly changing newsflow.

For last few years the management has been promising to invest excess cash reserves into newer projects/opportunities. But so far it has been nothing more than words of hope for investors. No plans in writing or indications of any timeline is unencouraging.

Currently the industry would be going through the lowest point in many decades due to ongoing COVID-19 created crisis. Such crisis creates an opportunity for stronger and bigger businesses to buy out smaller businesses at attractive valuation which are reeling from the crisis.

And in case of Avanti, it is sitting on Rs. 1000+ cr of cash on its b/s. I feel there couldn’t be a better time to have such a huge sum of money in your pocket.

If the management doesn’t find any opportunity to invest the money in current times, then there is good chance, the management just wants to hoard the cash and not worry about deploying capital in optimal manner.

Disc: invested for many years and getting itched for some quarters due to management’s capital allocation decisions

There can easily be a view that they being extra conservative isn’t too bad in current situation . Most of us with high allocation to equity have constant thought/wish on how great it would have been if we were a bit conservative in last 2 years.

Coming back to Avanti, I feel the sad part is not the managements intention but the Ground Reality that they are just not able to locate business as capital light and attractive as feed business. Just because it doesnt exist in first place !!

At some point management will have to reduce expectations and get ready to either find something reasonable like Shrimp processing or just start paying back through dividends / buyback.

We are possibly in for slow and steady business growth for some time, which again isn’t too bad if ‘STEADY’ part is understood well . I somehow feel that the market wants to value purely as commodity, while the actual sales have always been steady . It’s just margins which result in volatile EPS, but a positive long term trend of margin growth does show that may not completely be true

Hi Rohit, I tried speaking to couple of people in the industry and understood the following:

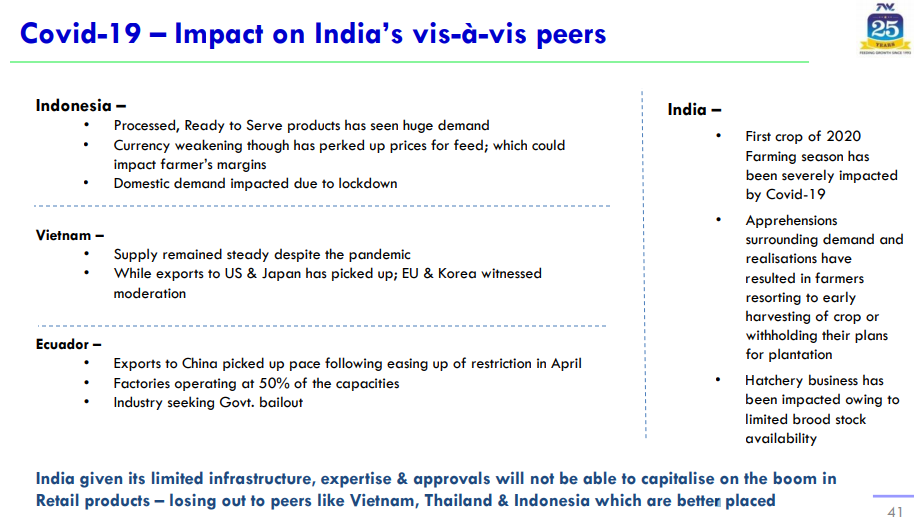

There was panic among farmers in Feb/March as Covid started spreading in Europe/America and many of them went for early harvesting as they were unsure about future. Prices fell at that time. Also the production was of lower count. Hence the first crop has been poor.

However, prices recovered in a month or so.

As the farmers were concerned about future, they have delayed the farming i.e… the second crop. However, as prices are stable now, things have resumed/improving.

So broadly people are saying that one may say that the season has got shifted by couple of months. And there will be drop in numbers for a quarter but most probably things will be back to normal for H2.

Other concerns are around the increase in input prices for the feed players - good thing is that price increase done earlier has been well absorbed by the market but there might be margin pressure for sometime.

On processing side - industry was operating at low utilization in March and April but things have been improving since. Players who were doing more of value-added products like RTE etc may do well in coming times.

Broadly, given the leadership of Avanti and a very strong balance sheet, there is value at lower/panic prices and strong long-term buyers come in on sharp falls or at certain valuation points.

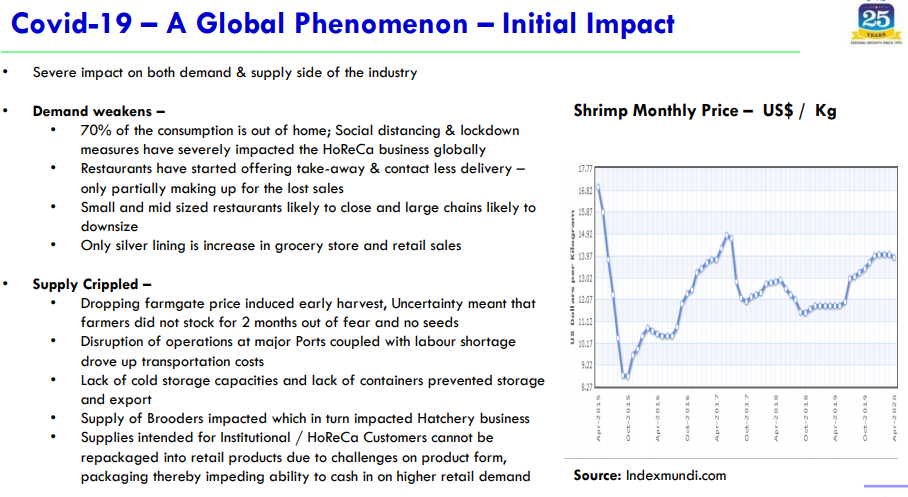

what about the demand side problems. in the presentation of waterbase they have mentioned that 70% shrimp is consumed in restaurants.dont you think the consumption of shrimp will go down for a long time, also it is a relatively expensive food. restaurant industry will be the last one to recover from corona.

@Shikhar there are other factors also - there were some articles about disease in key areas of China which may hit their production. So there are other factors also at play. At macro level its not so easily to analyse things.

@ayushmit govt just announced 50% msp hike for soyabean which should cut into the margins. Avanti went for a price hike only recently. What is you view on margin impact?.

Few weeks back I spoke with a farmer from West Godhawari ( Request vp members from coastal area to speak with farmers to get latest updates)

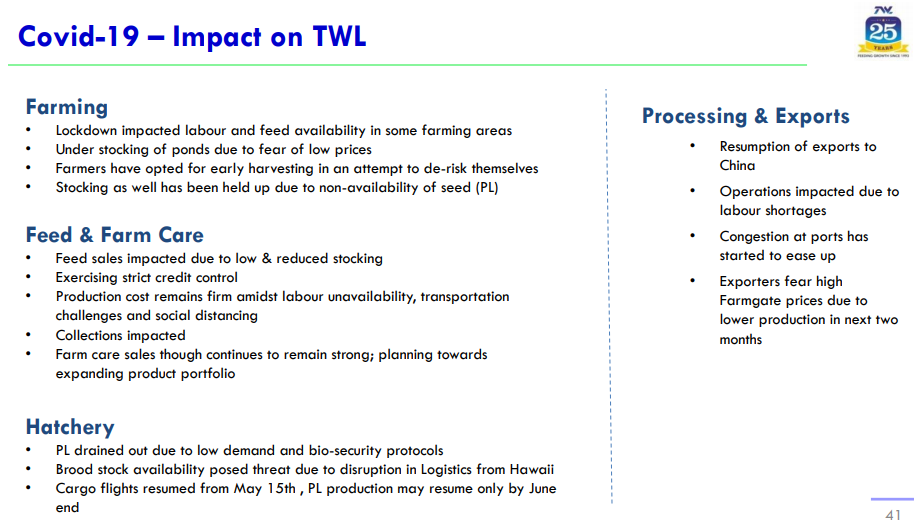

present shrimp price of 400( 30count) 300(40 count) 250(50 count). Price has dropped by 80 to 100 rs compared to 6 months back. 30-40 count price was dropped to 200 Rs. In summer it always drops due to lot of harvesting. During lockdown no shrimp buying was happening, feed supply was also problem due to logistics but things are much better now. Avanti feed 25 kg bag MRP of 2100. we get a discount of 20% on cash payment. Avanti feed price increased by 150 to 200 rs per bag compared to six months back.

Discl: invested

Thanks Ayush. This is very helpful. I was trying to connect with a few farmers but have only been able to get feedback from 2. I also hear the same thing that the panic was pretty high in March and one of these farmers had earlier decided not to go for sencond crop. Things seem to have stabilized a bit now and he decided to go for the next crop.

I am also a bit concerned about the demand panning out but as you rightly said there are multiple factors at play so lets see which way the things turn. I will be very curious about what management has to say in the next concall.

Like @rupaniamit, I am also beginning to feel that the management is being extremely conservative, bordering lazy with the cash. The issue with cash is that an acquisition in current feed segment will not make much sense for Avanti. They can probably set up their own plant to do that with speed and low cost. Something on shrimp processing might make some sense if they get a large capacity. Fish feed market doesnt seem to be promising and will be a very small start at best. Alternates (with a lot of imagination from my part) that can be more interesting would be an overseas acquisitions, or entering into B2C kind of segments. B2C will again be a long haul, but probably they should make a start given the integration that they would have.

Putting up a chart on Avanti. After the frenzy few years back when prices hit Rs 972 (adjusted), the margin contraction and slower volume growth caused a fall all the way to 271 around August 2019. Things were starting to fall into place again post that and it hit 770, but this didnt last long and stock fell to 251. Currently it has retraced 38.2% of the fall, which also happens to be a resistance level from past. The breakout from here could give some upside.