Govt levied 5% GST on fishmeal after Sept 2019. We are asking govt to remove the levy. If it is levied, cost will go up. By and large price is 89-90rs. Season has started and catches are normal. We can raise price if GST comes.

Price hike more than offsets the 5%GST on fishmeal. Next concall will give more colour on the impact on margin expansion because of the hike. Soya is moving up though

Latest Corona virus outbreak is apparently being linked to a seafood market in Wuhan city of China. Chinese government has shut the seafood market of Wuhan. This may be a bad news for shrimp exporters as USA, EU and China may pause import of shrimp from Asian countries for some time.

Essentially, as per the article, the virus is suspected to have originated from Bats. I don’t know if there is much migration to seafood. More likely, it would have to do with a person, who frequents the seafood market, that is contagious.

Given this, one would not expect more then a short term reaction as facts become clearer to us.

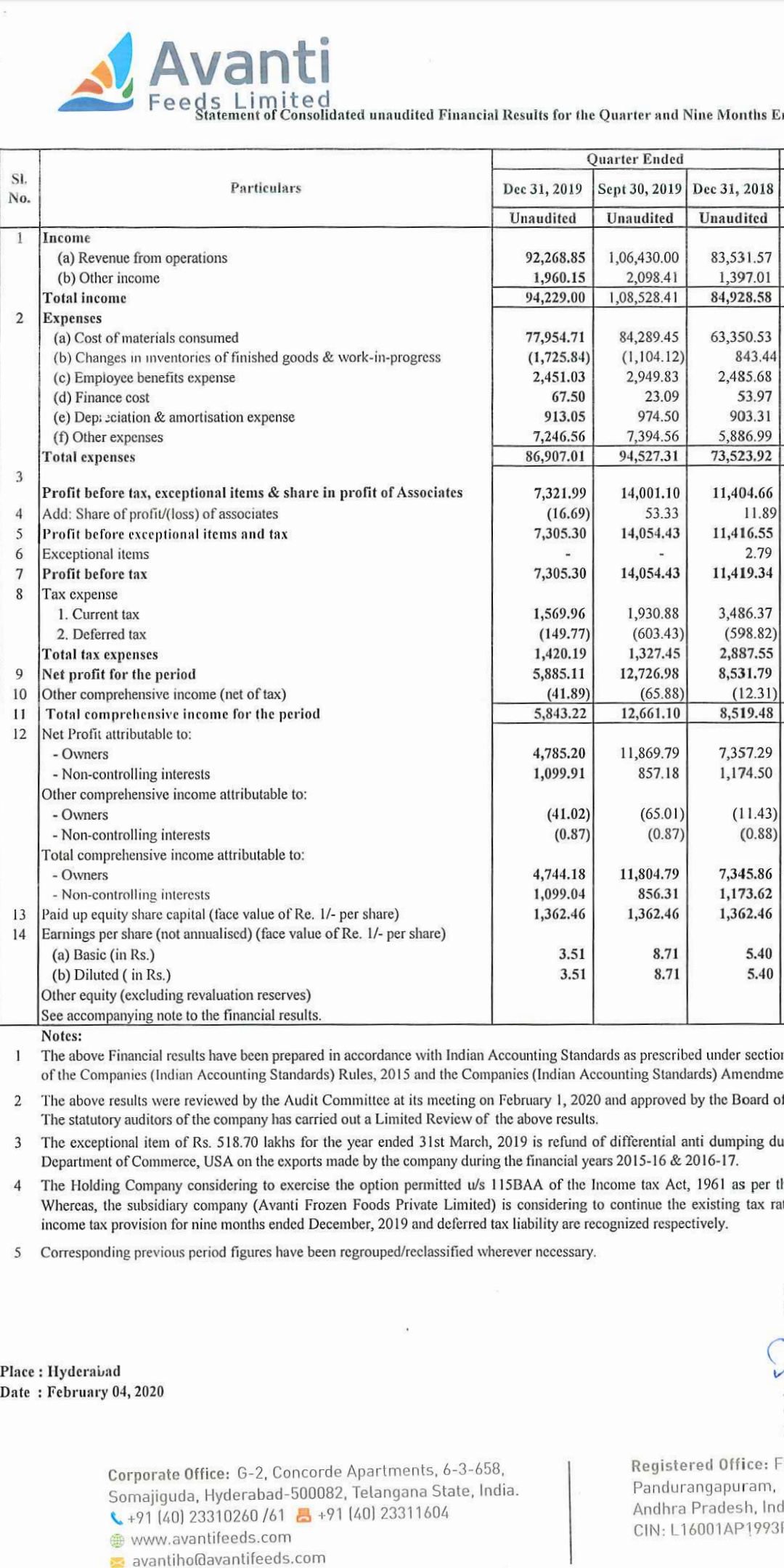

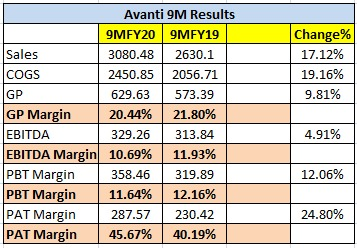

Sales growth was ~10%, which is good enough (expected was ~15%). Operating margin came down to 7% (expected was ~12% if you take Q2 as reference). This is because of higher Soya DOC prices in Oct and Nov, which came down in Dec and have now stabilised. Avanti’s increased feed prices by approx 8-10% two weeks back as well.

So, Q4 looks like a quarter where the cost pressure and realisation pressure won’t be an issue atleast. Will get a better understanding from the management concall.

I’d focus on 9M numbers. Avanti’s short-term gross margins would be volatile (on both sides) given many uncontrollable variables involved, especially until processing business becomes as big as feed business. 9M numbers look decent. Top-line growth is impressive.

Need to understand from management about 1) Corona virus impact on the industry and inventory surplus situation 2) Farmer’s reaction on hike in feed prices taken by Avanti 3) View on upcoming culture season

Most probably large part of margin hit would be due to higher cost of RM - Soyabean and GST on fishmeal. Earlier someone on our forum had shared about increase in end feed prices by 4-5 Rs per KG - so if that is true then the margins should come back in a quarter or so.

Just a few days back IFB Agro had come out with Q3 results and they had posted a loss in the feed segment. So probably this cost increase has happened for the industry and the industry would have taken a price hike.

If true then it will be positive in the longer term. Infact in case of sharp fall (more than 20% or so), it may be an opportunity to buy a very strong franchisee on a one off qtr.

It would be good to get an update on the impact if any due to Coronavirus.

Q3 is the weakest quarter for the industry and the key season (start of shrimp farming) starts from February or so. As per some of the feedback, there are expectations of strong growth for the industry for the coming year. This needs to be tracked.

Cheers,

Ayush

PS: Just sharing current thoughts. I may change my opinion/views if needed and may do the required buying/selling.

high shrimp stocks => low demand and prices

2)consumption hit during chinese new year due to coronavirus

3)Ecuadorian shrimp may be diverted to Usa due to fall in Chinese demand

Looks like a lot of headwinds in the short term atleast.Stock price too started to reflect this negativity.But if long term story holds,this might provide good accumulating opportunity

Marine Products Export Development Authority (MPEDA Chairman K.S. Srinivas told The Hindu on Friday said there was no alert from any country on seafood exports and shrimp and live items were being exported to China and other countries.

“The impact of coronavirus on seafood exports is minimal. There is no need for farmers or exporters to panic. The demand for shrimp and other varieties remains unchanged at the global level,” Mr. Srinivas said.

“We are exporting shrimp and fish from all major ports across the country. Exporters need not fear the spread of virus as the produce is being exported through containers, and India is not importing any product,” the MPEDA Chairman said.

when shrimp prices are down, processing profit go down but ability to raise feed prices go down.

when shrimp prices are high, processing pfrofit go up but ability to raise feed prices is good.

Spoke to a friend who is into shrimp farming in Rajole, Andhra. Below may not be indicative of the overall industry scenario:

shrimp prices r firming up and activity in the farms picking up. In Jan, during Pongal activity slows down in the farms and picks up there after

as of now, there has been no slowdown due to external factors ( like coronavirus etc).

He uses a Chinese brand ( Uni President) as shrimp feed. He says, generally large farmers and corporates prefer Avanti feed due to discounts offered by the company on bulk buying and various other incentives.

he says, such macro negative events have created brief lull in terms of consumption in the past . But, eventually consumption returns to normalcy

as of now, only Avanti increased feed price apparently. Rest r expected to follow.

Separately, water base results yesterday reflect the overall cost pressure in feed segment.

Need more such data points to gauge overall industry scenario.

Disc: invested. No transaction in last 3 months. Not a buy/ sell reco. Pls do your own due diligence.

Good presentation released by Avanti. As mentioned previously the processing business is on faster track, clocking in the highest quarterly volumes and revenues till date and is operating at 72% capacity only !!