In Q2 concall, Avanti team mentioned that farmers are slowly returning back to shrimp farming with improvement in shrimp prices and rise in export volumes . I feel, slowly and steadily sector is coming back on track. While, we may not see major spike in Q3 (being lean season), I expect Q4 this year to be better.

Invested. Not a buy/sell reco. Pls do your own due diligence

Indian shrimp exports have been faring better than the broader market. Any particular reason for indian shrimp increasing market share? I know low cost is a competitive advantage. Anything else apart from that?

Why did the US consumption fall so significantly in some of the months (July)? I mean any reason for the consumption to be seasonal or cyclical?

Disc: Invested and small part of portfolio. Evaluating the risks/rationale to scale up/down the investment size.

To my knowledge, adverse climatic conditions in US at the beginning of this year led to a drop in consumption of shrimp and eventually led to buildup of inventory in US. This led to lower off take by US in subsequent months and also fall in global shrimp prices. Hence, we see there is a drop in June/July. Usually I believe, peak buying season of US customers from Indian exporters happens from July till October. Many exporting countries could not have coped up with drop in shrimp prices and would have temporarily suspended shrimp farming (even in India, there has been a drop in repeat crops during July- Sep due to which Avanti reported much lower Q2). Previously, countries like Thailand, China used to do larger exports than current monthly numbers. Thailand fell because of breakdown of EMS disease in the past (?, not sure if I got this correct) and China’s exports reduced over the years due to higher internal consumption and higher ADD being imposed by US. Have read in the past that, India has a great potential compared to few other countries to promote shrimp farming, due to favorable climatic conditions and vast coastline (not sure about cheap labor as haven’t seen any data pertaining to this). Will need to see, how the op drivers pan out in the coming quarters.

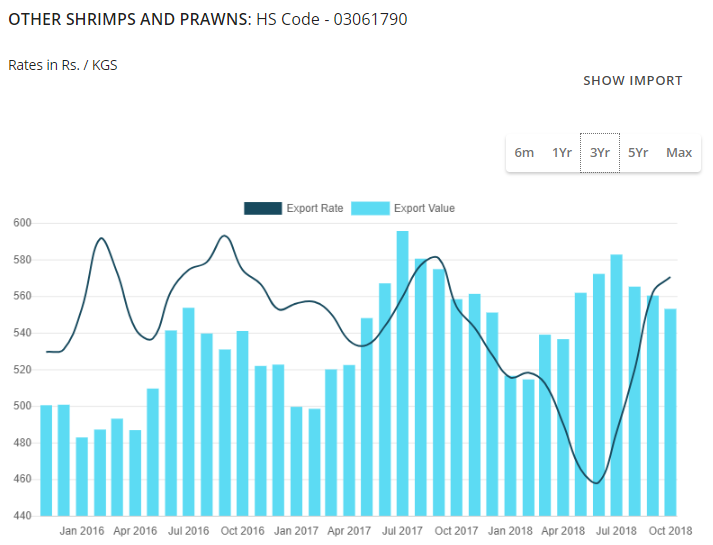

Here is the 3 year chart of Shrimp prices (based on exports from India). Usually they used to be in a range barring 3-4 month period earlier this year which brought the Indian industry (particularly farmers) into trouble and many of them skipped the second crop!

Interestingly the prices came back to normal 2-3 months back but the mood in market became very negative for the whole sector.

The above doesn’t means Avanti is a buy now or things are back to normal (in terms of growth etc).

Avanti needs to address on the growth prospects and utilization of cash going forward.

That’s very interesting, there is a lot of dissonance in discussion here because of 2018 which was an abnormally bumper year but if one takes the above graph, we should be back to 2017 levels, which are per se decent on most return parameters. Not that the stock is cheap at current prices but given normal growth rates and stable pricing we should be looking at a good 2020. Utilization of cash i agree with totally, the logic eludes me. Management has consistently been stone walling discussion on this point.

There has been a bit of technical bounceback here, sort of a pullback in a falling wedge. I suspect there is still time to go here before the curve flattens.

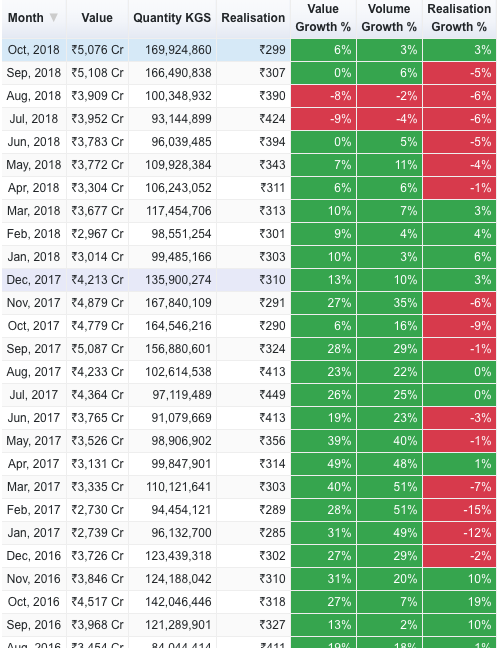

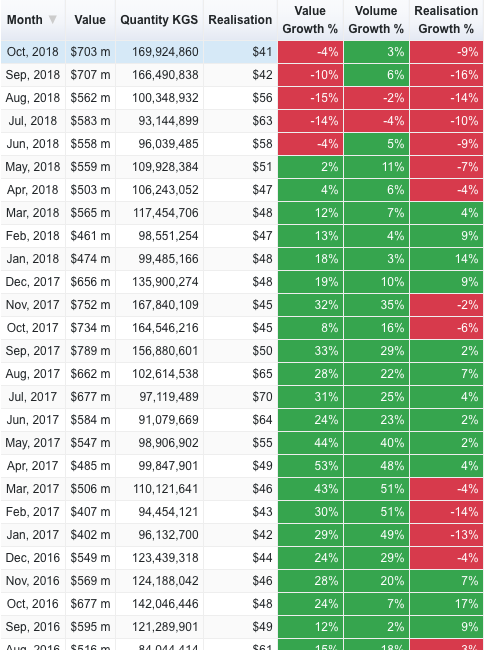

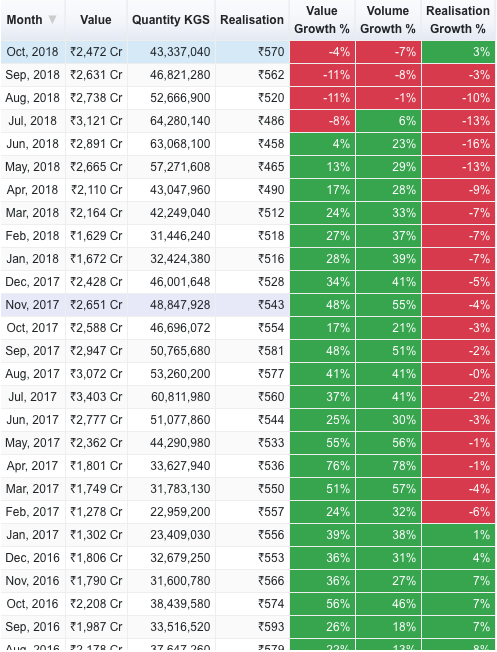

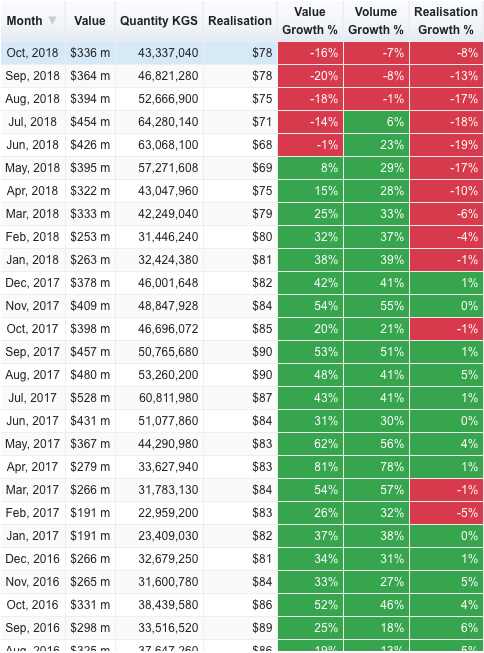

a) while shrimp exports to US have increased (yoy, mom) in Oct 2018, total shrimp exports to all countries have declined by around 7%

b) I am bit relieved to see realization on shrimp at 560-570 levels. If we notice, when it dropped to 450/460 in Apr-June, farmers have suffered losses and have decided not to go with second crop in Jul-Sep period (which led to a low Q2 for Avanti).

c) if these realization levels continue/improve further, farmers would come back during the next season (in Q4, Q1).

Avanti feed /processing plant current capacity utilization is around 70%/50%. Higher volumes in feed/processing capacity would further improve operating leverage and may improve the earnings in Q4/Q1. Icing on the cake would be, further drop in raw material prices (esp Fish meal, which has kind of retreated from historical highs attained during beginning of this year).

Just a small concern from a newbie, not sure if its valid or not. Avanti’s 10 year sales growth is around 41% while that of its earning growth is close to 80%. Is it a red flag? are they trying to manipulate earnings to increase share price? Though I do not foresee it based on management clean history, but a thought from this forum is highly appreciated.

This was a known norm already declared aroun middle of 2018. My feeling is that this tracing will consolidate the export to USA.Also its not only targeted to Indian export. Vietnam also unloading lots of illeagl shrimp consignment to both US and China.

HS Code level Data is not yet available for December. DGCIS is quite slow when it comes to this data. It takes roughly 6-8 weeks is what I have noticed. So we can at best expect it next week or a bit after that.