I listened to Avanti concall today and it seems management is very confident of maintaining topline at previous year’s levels.

The main risks to margins remain the volatility in raw material prices namely fishmeal, soya and wheat flour prices which have gone up significantly in first six months of calender year 2018 and now seem to be stabilising/cooling off. Of these, soya prices might not come down too much as it is protected somewhat by MSP announced by govt. There is high cultivation of soyabean and a rich harvest can curtail excessive rise in prices. Wheat flour prices I think will remain steady/go slightly down. Fishmeal prices is where some amount of relief can be there. This depends largely on the kind of fish caught. It remains a rich source of protein and till an alternative comes up is likely to remain important in the raw material mix.

The other variable remains the farmgate prices of shrimp. If the farmers can make more money due to higher farmgate prices, the company can raise feed prices to some extent. But it seems from management commentary that in the larger interest of the business equilibrium, it cannot get away with raising prices in accordance with higher raw material prices.

This comes across as a business with limited pricing power and hence a volumes and market share gains game.

Disease outbreak remains a sword hanging over the whole business. It can come about any time. Vietnam it seems is facing this issue now.

With so many variables affecting the business and poor pricing power, we need to make our minds what kind of valuations we can pay for this kind of business.

Management hinted at maintaining topline same as previous year. If just for the sake of calculations if one were to go by management commentary and project earnings (this can be way off the market because of changes that can happen in farmgate prices and change in raw material prices) on a topline of say 3400 crores management has guided for 12% margins. Operating profit could be around 400 crores. Other income of 50 crores takes the total to 450 crores. On this based on q1 depreciation of 9 crores, we can put in depreciation of 40 crores. So PBT comes to 410 crores. Company pays full taxes (as per last 2 years ) so tax comes to 135 crores. So we arrive at a net profit figure of 275 crores. Based on a current market cap of 5600 crores the price earning multiple comes to around 20 times FY 19 projections.

I would love to buy it at 10 PE  but it seems thats wishful thinking since company is a market leader and still gaining market share. So at around 15 PE maybe it is worth a definite entry and accumulation. This level is around 3700 crores market cap which warrants a 30% correction from current levels.

but it seems thats wishful thinking since company is a market leader and still gaining market share. So at around 15 PE maybe it is worth a definite entry and accumulation. This level is around 3700 crores market cap which warrants a 30% correction from current levels.

The other view can be that these are cyclically depressed earnings and happens once every few years and things tend to improve after a brief lull. That changes most calculations and perceptions and levels to buy. If one considers these assumptions then current levels also offers a good entry point.

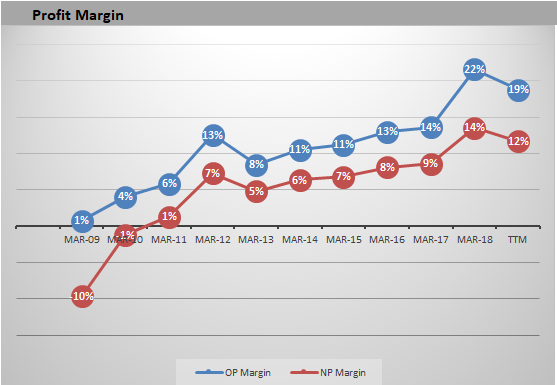

This is a company and sector where most positives and negatives are bunched up together. In fy 18, which was a bumper year, the farmgate prices were high, demand was good, raw material prices were abnormally low and company had a bumper year. Picture now seems exactly opposite with higher raw material prices, lower farmgate prices etc. The recent spurt in farmgate prices needs to be seen in terms of sustainability. i.e how long can these spurts sustain.

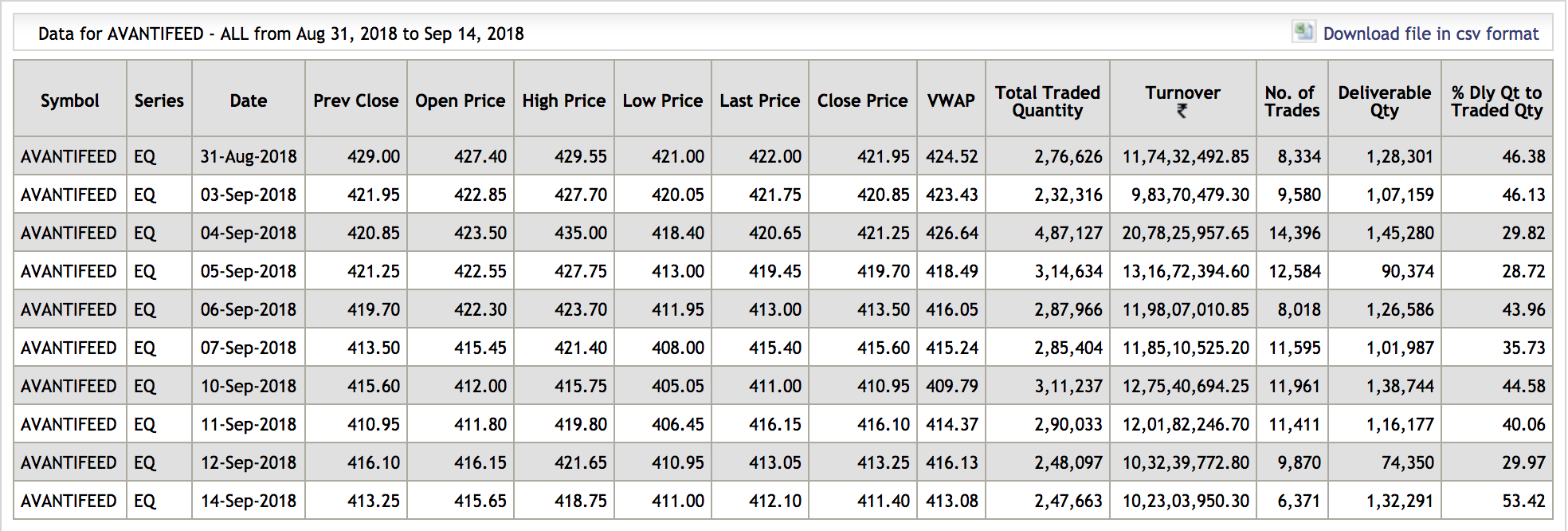

Technically till now there has been a series of lower tops and lower bottoms. None of the price rallies has managed to take out previous tops. Most rallies have finished closer to 50% retracement to previous fall or lower. Going forward the recent lows of 388-390 remain extremely crucial to watch.

disc: no position but under watchlist.

Thai Union and CP Foods stocks have been sedate.

Thai Union and CP Foods stocks have been sedate.