Yes there is a tail wind for Avanti which is going to benefit it for lowering the cost of its raw materials.

The 3 main sources of its raw materials are

Fish meal - 20% of total composition with value contribution of 36%. This is mainly made in India on the western coast karnataka, goa, maharashtra but I cant dig out from where does Avanti actually source them.

Wheat and wheat flour - 30% in total composition but only 10% in value contribution. Avanti itself is into wheat barn production but only worth 28L sales in 2016.

Soya Meals - This is almost 40% via input mix and costs 25% in value. The main area where this is picked up from is MP’s and Maharashtra’s Soya meal manufacturers. MP is the best place to grow Soya in the country.

The price of Soya has kept dropping over the months. If we check NCDEX the picture is evident even in the futures contracts up to Dec. Infact the price has dropped from 5000 18 months or so ago to 3000 and below now. July 2017 contract movement attached.

I do not have 2017 annual report.

Also have been speaking to a shrimp farmer in Andhra and he used to rely on Avanti feeds but he has recently switched to a Taiwan based company’s feed as he is not getting sufficient growth from Avanti. What could be the reason I wonder. Need to dig deeper.

Anyways ‘One man’s poison is another man’s…’ was my reaction after reading the above post. But perhaps capitalism works this way.

Tilapia fish can grow very fast and it doesn’t need too much of feed. It can manage with planktons. **The cost of feeds is much lower compared with shrimps. Again, in shrimp farming, you have to be careful in maintaining the water quality. Tilapia, on the other hand, is resistant to any kind of imbalance in the ecosystem.

Did some digging around and preliminary observations are as follows:

If we look at Avanti from a pov of providing feeds then it has most of the wherewithal to do this(obviously capacity expansion would be required). Why do I say this? If we look at the Nile Tilapia its feed constitutes over 50% of what Avanti does today, the other major ingredient is rice bran which is abundantly available in the regions it manufactures. Also the GIFT variety which is grown in India is far more resistant than the Nile variety. GIFT Talapia is a hardy variety and can survive undernourishment too. Soya is the major ingredient.

Source: FAO https://goo.gl/8XeUNC

Growth of Talapia culture: India has seen a burst of GIFT farming especially in Kerala. Like I mentioned above GIFT is extremely hardy and can manage to grow in poor conditions. Distribution of GIFT seeds has increased 70x+ from 2014 to 2017.

Source: https://goo.gl/BD0Q5S

Disease in Tilapia: FAO has come out with a warning two weeks ago on the Tilapia Virus. It doesnt affect humans but is lethal for the Nile variety. This has had a devastating effect on the Tilapia’s of Thailand (90% failed crop) and other countries also (not including India). Perhaps GIFT is disease resistant thats why. The disease is being evaluated in India as I type.

Source: https://goo.gl/SwstL3

As of today Avanti does have a fish feed product but its sales might be a mere shadow of what it does for shrimps feed. Will check the numbers.

So can it be a threat to the business , as the farmers may move to Tilapia fish as it requires less feed. Can it affect the Avanti’s business in Negative way. Please clarify

I think it all depends on how much profit is there for farmers from Tilapia fish vs Shrimp. As per the last concall, management has not yet analysed on the type of fish, market size etc, Also we need to understand how easy it is for the farmer to shift from shrimp to Tilapia fish.

Disclosure: Invested.

I was speaking to a friend who is in the shrimp business in Andhra. His evaluation did include Tilapia vs Shrimp when he started out. He went with shrimp because of the following reasons:

GIFT is a low risk - low reward business

The seeds of GIFT is not widely available

The pH of the water is not suited for Tilapia

What I understand is that the switch from Shrimp to Tilapia is prohibited by these factors. Even if seeds availability is increased drastically (as I pointed out in my last post) the pH and profitability might not be an attraction for existing Shrimp farmers.

For new players entering aquafarming yes Tilapia could seem attractive if they can set up the business.

From Avanti’s pov I think this is not a threat infact its an opportunity for them. The incremental effort to build this product line should not be much as they are the best people around to do this business. Plus the management is enterprising and I ‘guess’ they will continue to be enterprising if such an opportunity comes knocking at their door.

I hope my friend is ok with me sharing all this information.

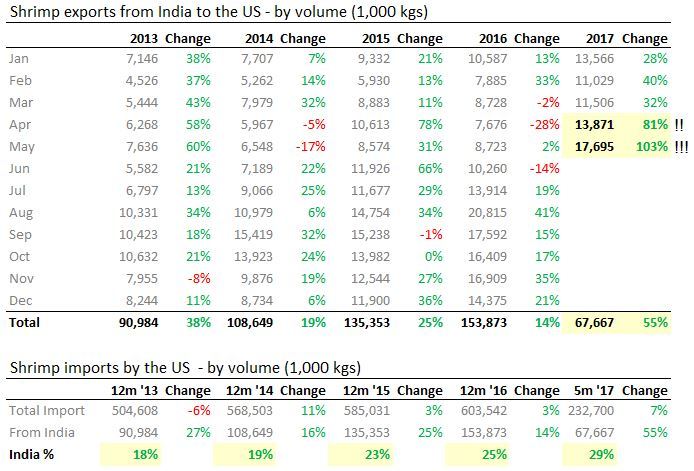

Keep in mind that frozen shrimp exports growth only confirms what we have seen in feed sales. It is a lagging and not a leading indicator of feed sales. i.e. first feed sales would go up which will result in higher shrimp production which in turn will result in higher growth of frozen shrimp exports.

However we can use these numbers to conclude that shrimp is a fast growing industry and that will help Avanti in the long run especially its foray into Shrimp processing.

Apex Frozen Foods in its DRHP has given a glimpse of how the growth and profitability of the processing business and it it looks good.

What I am able to make out from the Industry report and the news is that there was an expectation that the Anti Dumping Duty (ADD) might get lowered but instead it has been extended for 5 years. Perhaps this is taken negatively. This in my opinion would only be a short term reaction as the current business doesn’t not get impacted and continues as it is. Is there a future date will this be re-looked at within 5 years by the International Trade Commission of USA? The positive is off-course the green channel to the 140 players.

I guess the Avanti stocks performance in the markets in last few days is

due to such great news from the frozen shrimp export nos. Can we expect a

superb Q1 YoY. QoQ may not be great as Q4 was outstanding…

Note: Stock price has run up a lot in 2017. Please please read risks highlighted by Avanti veterans in the posts above, should you choose to put in new money at high level. Disc: Invested.

Hi @lohiyaakshay08 - If you are referring to selling by Mr. N Naga Ratna - i think its ignorable as this person has sold in earlier years also. And its natural for people who are not much involved in the company with some stakes to do some profit booking etc.

@spatel - thanks for sharing the data Do we also have data about total export from India? I’m just wondering that it could be that due to huge growth in internal consumption by China over recent years (China became a net importer from being a net exporter) could have resulted in replacement in supply to US by India over Vietnam etc.? And the right data to look for would be total export of shrimps from India to judge the industry growth (which i would expect to be at about 20-25% or so for the current calendar year)?

Do we also have data about total export from India? I’m just wondering that it could be that due to huge growth in internal consumption by China over recent years (China became a net importer from being a net exporter) could have resulted in replacement in supply to US by India over Vietnam etc.? And the right data to look for would be total export of shrimps from India to judge the industry growth (which i would expect to be at about 20-25% or so for the current calendar year)?

Do we also have data about total export from India? I’m just wondering that it could be that due to huge growth in internal consumption by China over recent years (China became a net importer from being a net exporter) could have resulted in replacement in supply to US by India over Vietnam etc.? And the right data to look for would be total export of shrimps from India to judge the industry growth (which i would expect to be at about 20-25% or so for the current calendar year)?