But as per concall , Ecuador is more into commodity shrimps and avanti is into more of value added shrimp like tempura.Also Ecuador doesn’t do much of value added shrimp due to their lower population (it requires lot of labour to make value added shrimps as per concall). The value of shrimp exported to US is around 770cr out of their total revenue of 5500 cr . Also they have been concentrating on higher value added shrimp which don’t attract duty ( but have to check how tariff ll affect it ).They were also reducing exposure to US by diversifying to other countries like Europe & Middle East .

Also their current profitability majorly was because of lower raw material cost except for wheat flour which is also trending lower now with the arrival of new crop .

The Indian shrimp feed market reached $1.7 billion in 2023. It is expected to reach $7.1 billion by 2032

at a growth rate of 17.21% CAGR during the period, according to researchandmarkets.com.

Few takeaways from concall:

- Finished Feed prices is decreased by 3 rupees per kg, due to global uncertainty .

- MSP of soya is increased by government, which will increase raw material prices.

- Ecuador is having edge when it comes to overall duty (Antidumping, CVD, Flat tariff imposed by Trump). Management continue to emphasis on value added shrimp category, which Eucador cannot able to supply. How much this translate into numbers is still debatable?

- Aims to go for 10 crore revenue for newly launched Pet care division (Cat feed)

Disclaimer: Not holding

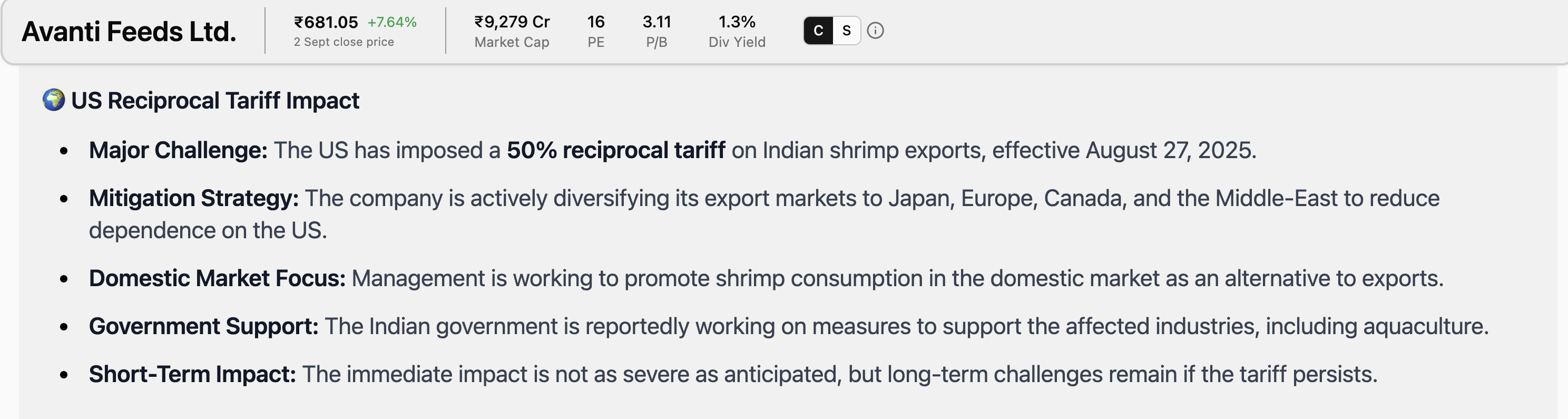

Any updates from the company with the 50% US tariff coming into play.

Key takeaways from the Q1 FY26 earnings call (about US tariff impact)

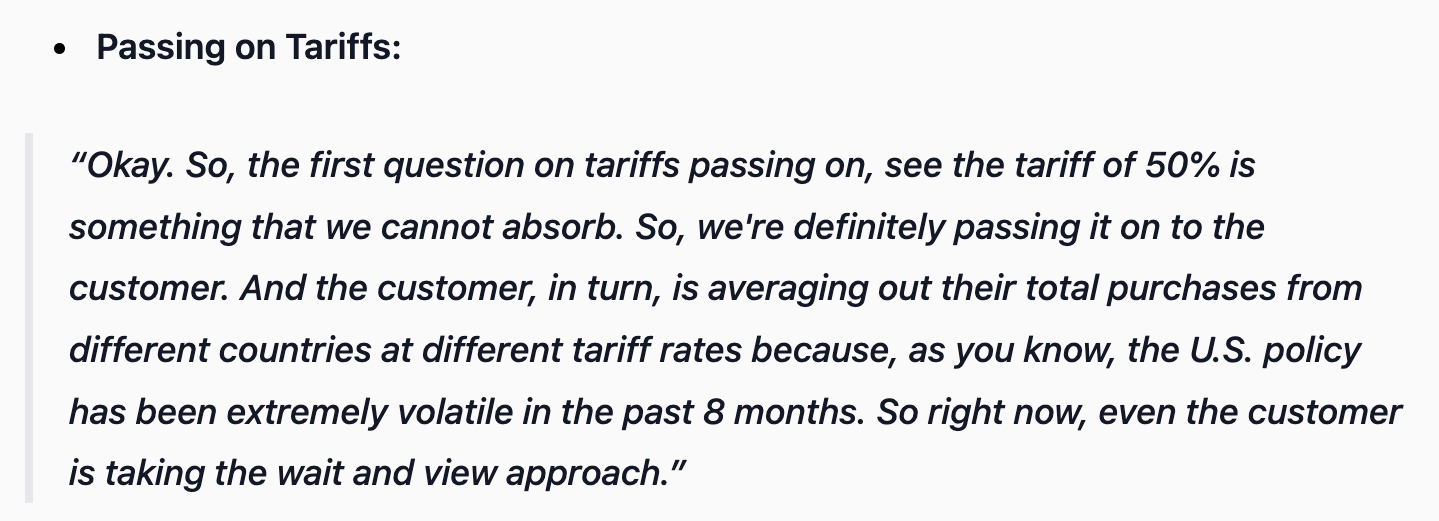

Management commented that they are passing tariffs to customer as 50% is something they can not absorb

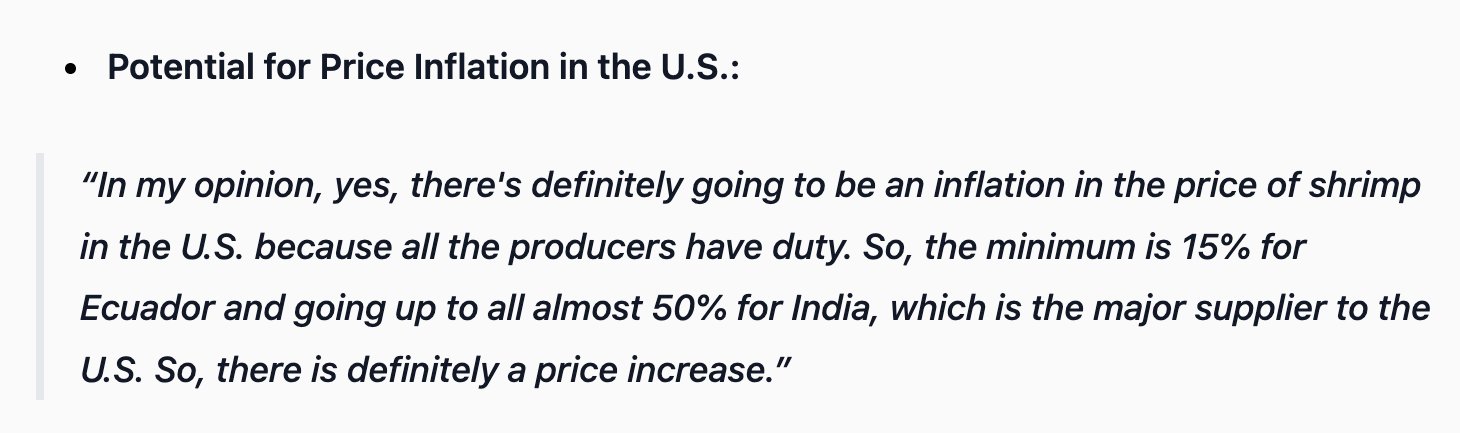

Inflation to follow in the price of shrimp in the U.S., as minimum is 15% for Ecuador to 50% for India

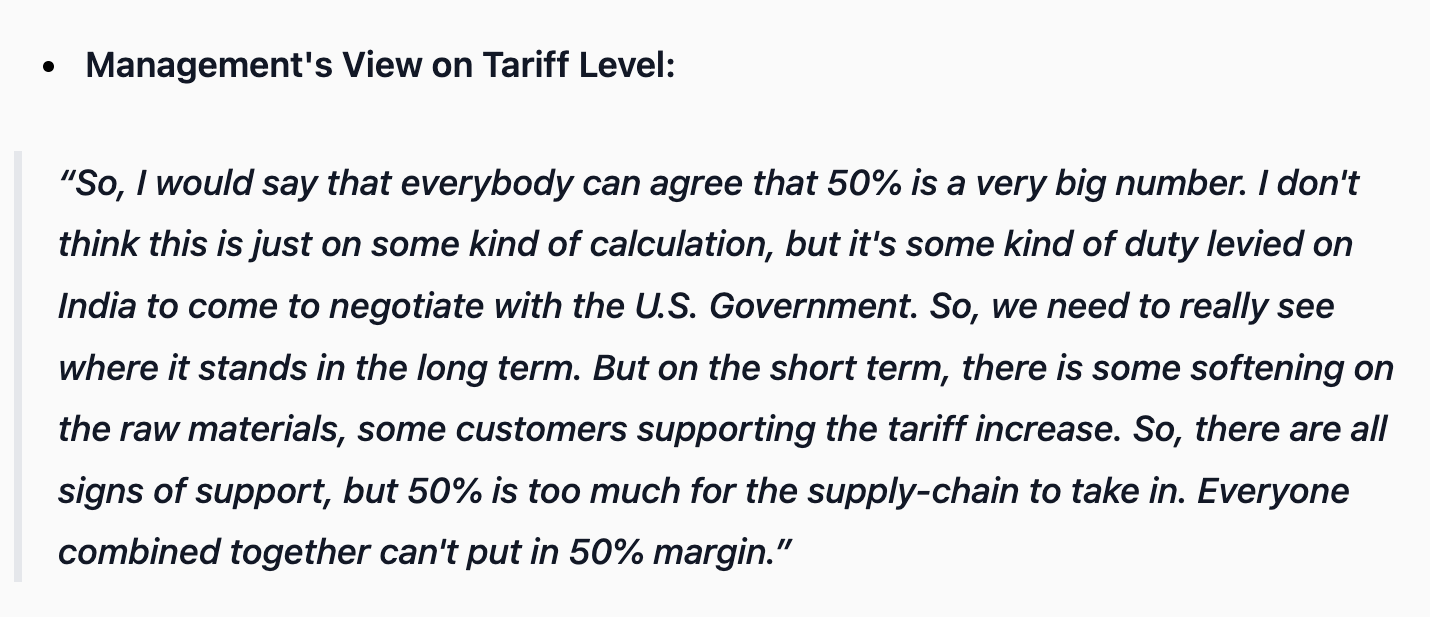

50% is a very big number for any supply-chain to take in

News are negative.

https://www.financialexpress.com/business/industry-andhra-50-export-orders-cancelled-shrimp-export-losses-pegged-at-rs-25000-cr-3978597/

Waiting for clarity

We are part of this discussion to understand Avanti Feeds’ evolving business model, financial strength, and diversification into new segments. The aim is to evaluate whether the company’s growth story remains structurally intact despite industry volatility.

Avanti Feeds was founded in 1993 and has a vertically integrated aquaculture supply chain with feed mills, hatcheries, farms, and processing facilities. Its subsidiary AFFPL caters to shrimp processing and exports, offering a fully traceable farm-to-fork supply chain to destinations such as Europe, the USA, Japan, Korea, China, Russia, Canada, and the Middle East. The company’s specialty lies in scientifically formulated, nutritionally balanced shrimp feed aided by worldwide technical services and compliance with international quality standards.

In FY25, revenue increased to ₹560.03 crore from ₹536.89 crore in FY24, evidencing sustained demand in the face of market stress. EBITDA widened to ₹79.85 crore (14.2%) from ₹59.44 crore (11.1%), and PAT rose significantly to ₹55.71 crore (9.9%) from ₹39.38 crore (7.3%), with EPS increasing from 26.2 to 38.8. Growth indicates enhanced profitability led by operational efficiencies, better other income, and improved export performance.

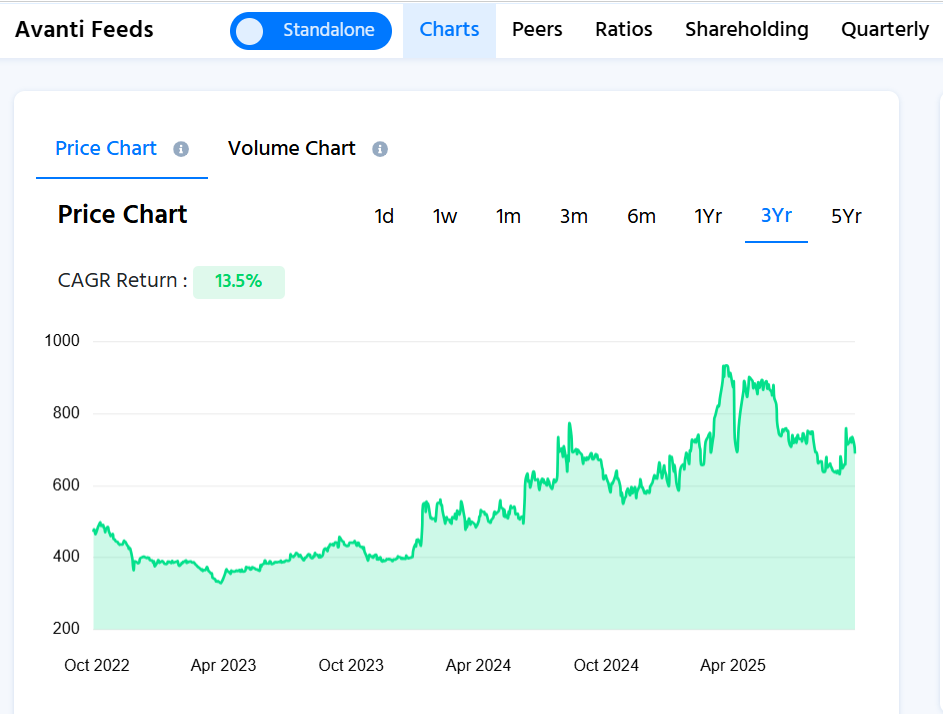

The one, three, and five-year CAGR is 9.3%, 13.5%, and 8.5%, respectively, indicating medium-term growth consistently. On balance, Avanti Feeds has a robust core shrimp business going hand in hand with prospective opportunities in the pet care and fish feed businesses, driving sustainable revenue growth in the face of risks emanating from tariff fluctuations and hatchery operating cycles.

Shrimp feed remains the highest revenue earner with strong growth in volumes, with processed shrimp exports sustaining steady volume expansion. The hatchery business witnessed a downfall due to operational cycles, and power and ancillary earnings, though lower, witnessed gains in efficiency. For FY26, the company anticipates feed sales of approximately 5.6 lakh MT and shrimp exports of 17,000 MT, with management having moderate confidence because of volatility in tariffs, while long-term outlook continues to be positive through diversification in domestic markets.

Avanti Feeds has also ventured into the pet care segment strategically through its Avant Furst brand. It introduced cat food in January 2025, and then tuna cat food and dog food (chicken and vegetable) in July - August 2025. Q1 FY26 sales of the segment were decent with a target of ₹10 crore in FY26, indicating an emphasis on high-margin, long-term growth. The company is targeting e-commerce business from September 2025, fast commerce from December 2025, and a new 30-acre manufacturing plant in proximity to Hyderabad, with completion within 18 months. Trials of fish feed are currently being conducted under Indian conditions with local production as a medium CapEx project on the anvil.

Would like to hear members’ thoughts on Avanti Feeds’ growth sustainability and diversification strategy.

- Can EBITDA margin improvement sustain amid tariff and raw material risks?

- Is pet care (Avant Furst) a serious long-term growth driver or just an experiment?

- Does the farm-to-fork integration provide a durable moat in the global shrimp market?

Positive for Avanti Feeds as this move can help the company diversify its exports: Australia clears shrimp exports from Andhra Pradesh

Short summary Avanti Earnings call( there may be some error as summarised with a day lag post listening)

- Company has been able to pass the tariff to customers and will impact if tariff issues persist beyond JAN 26. Mitigation plan is to diversify EU n APAC markets

- Primary raw material for feed is wheat flour and soya flour and both prices trending up due to Indian govt allowed a million ton of wheat for export driving prices up in domestic market and may impact margins.

- good response to Cat Food introduced in Jan 25. Introducing new flavour. Also launching new flavours in Cat food and dog food as well. Products are well received among pet owners looking for quality products. Currently imported from partner Thai Union(If I recall correctly)

- 30 Acre land converted from agri to set up pet food factory in Hyd. Expected to start production with tech from Thai Union by end of FY 27. Company expect to garner good market share prior to that.

- some resolution of trade issues in Russia EU n Oz markets provides alternative to US trade at risk due tariffs

-

https://avantipetcare.com/

——-

Disc: Invested

Source: Department of Fisheries India

What’s going on with Avanti, the stock broke it’s ATH? nearly doubled from where it was 2 weeks back.

From what I understood the major driver is the reduced import duties on Indian shrimp from nearly 50% to 18% effectively hands back 32% of the value to the supply chain.

Am I missing something? Is it just the reduced import duties?

This may be one of the reason as Soyabean is raw material for the feeds.

The stock has been under consolidation for more than 8 years. Given how strong the current breakout has been, does it look strong technically?

Fundamentally many headwinds seem to be behind. Management is focused on geographical diversification, value add products and new business areas for growth.

True, technical analysis wise long time breakout with very huge volume indicates that this uptrend might continue and sustain. And can potentially give a huge rally in the long run from the breakout levels.

Disc - Invested and biased

The company has not published presentation nor arranged earning concall, this is bit new as it has been consistent in doing so. In absence, I saw presentation of Apex and it gives good idea however it has exposure to exports to EU.

Anybody following closely has idea of Avanti doing Earning concall bit later (delays of some days) in case of KMP not available immediately after results?

Avanti in general does concall after a gap of few days if I remember correctly.

Finally, concall is scheduled on 3rd March 2026 to discuss Q3FY26 results and developments.