|

Aurobindo Pharma announced the results for the quarter ended December 2013 and recently held conference call .Highlights of the call by Capital Mkt: The Revenues realized at Rs 61.80 during the quarter compared to Rs 55 in Q3'FY13. The US formulation grew by 81% to Rs 931 crore during the quarter on the back of certain new product launches and reintroduction of certain cephalosporin's products (USD 9 million). The Aurolife US manufacturing base has improved the profitability driven by the higher capacity and enhanced order book. During the quarter, it has introduced 2 control substances in the US market. The Company is marketing injectibles which are doing well in the US market. It has introduced 7 products in the US in Cephalosporin's during the quarter. It expects to do them well going forward. It has filed 308 ANDA's and received 163 ANDA's approvals (25 tentative) with the USFDA as on 31stDecember 2013. The filings and approval for the various Units are as follows: Unit 3 (Oral non-betalactam products) â 117 filed, 114 approved, Unit 7 (Oral non-betalactam products) - 89 filed 30 approved, Auorlife â 20 filed 7 approved, Unit 4 (manufactures injectables) â 50 filed 8 approved, Unit 12 (Manufactures Cephalosporin's) - 20 filed 19 approved, Unit 6 (Manufactures Cephalosporin's) - 11 filed 10 approved and Auronext one product is filed as on 31stDecember 2013. In the Cymbatla market, the number of players has come down (originally 10) but it expects some new players to come into the market in the next 4-6 weeks timeline. It expects 6-8 approvals in the next twelve months and 15 approvals in the next 2 years over that in injectables. The initial lot is in shortage list but the market size is small. The Cephalosporin's business degrowth at the API level, mainly due to the fact that the market is competitive. The Company will focus on the margins i.e. on high value products, not specifically want to grow by losing the margins. The base business slightly improved in the last quarter. Excluding Cymbatla the top line would have grown by 15-20%. On the Margins, Excluding the Cymbatla improvement the margins were around at 22-23%. The Company indicated that all the business is firing well. For the next year, itexpects to grow in Auromedics, US and Europe to grow well. Also, the API business continued to improve. The drivers for the margins are US growth, Auromedica and Aurolife growth in next year. Also, the ARV's and API are expected to do well. The Company recently announced acquisition of Actavis's Western European Operations in 7 countries. The acquisition expands Aurobindo's front-end operations into five segments (generics, prescription products, over-the-counter products, hospital products and generics tenders) with approximately 1200 products and an additional pipeline of over 200 products. The Management estimates the net sales for the acquired businesses would be around EUR 320 million in 2013 with a growth rate of over 10% year-on-year. Although these businesses are currently loss-making, it expects them to return to profitability in combination with its vertically integrated platform and existing commercial infrastructure. The Actavis making EBIDTA loss is Euro 20 million and expects the break even for this business in the Second year. The largest of revenue contribution are from generics followed by hospital and tender businesses. The Company Capex is expected to be Rs 300 crore (including the maintenance capex) for the FY'14 The Gross debt is at Rs 3590 crore (majority in foreign currency) and the Cash in hand 196 crore as on 31stDecember 2013. The Company has repaid the USD 60 million of gross debt during the fiscal. |

Hi,

Valuepickrs who are tracking the stock closely…can we expect Q4 EPS to be close to or above 25? I am expecting EPS to almost double on a QoQ basis…would like to hear views of other people here…

The company has came up with excellent numbers for this quarter. There has a profit booking after the results at CMP 630 the stock looks interesting. Added recently to my portfolio. Bank of america has raised the target to 740.

Highlights of the call by Capital Mkt:

The sharp growth in US formulation sales is on the successful launch of new products coupled with reintroduction of cephalosporins coupled with market share gains in the existing product basket.

The reintroduction of cephlopsirn’s into the market from Unit 6 generated sales of USD 28 million during the year.

The Aurolife US manufacturing base improved Sales (USD 74 Million) and turned profitable during the year. The Auromedics (injectibles products) generated USD 37 million Sales during the year. The Aurolife is growing - 1) expansion of base business 2) New products awards.

It has filed 336 ANDA’s with US FDA as on 31stMarch 2014 and received approval for 191 ANDA’s (155 final approval). Out of the 191 cumulative approvals, net of 10 withdrawals during the year including 26 tentative by US FDA.

It has filings and approvals from various units are as follows: Unit 3 (Oral non beta-lactam products) â 118 filed, 114 approved, Unit 7 (Oral non beta-lactam products) 111 filed 33 approved, Aurolife â 20 filed 7 approved, Unit 4 (manufactures injectibles) â 55 filed, 8 approved, Unit 12 (Manufactures Cephalosporin’s) - 20 filed 19 approved Unit 6 (Manufactures Cephalosporin’s) - 11 filed 10 approved and Auronext one product filed as on 31stMarch 2014.

The Company moved from the non-regulatory to regulatory market for APIs’.

The Sales from the Unit 4 (injectibles) is 27% of total Sales in FY’14. It expects to launch 4 more injectible products by the end of FY’15.

The Recent launches Prandin and Avalox maintaining decent market share and stable. The Cymbatla is doing well and more players expected to come in June third week.

The R&D expenses are 4.6% of Sales for the FY’14.

The Oncology block expected to be commissioned by March 2015.

The Capex is Rs 350 crore (includes maintenance Capex) for FY’14. This is apart from acquisitions during the year. It expected to be in the range of Rs 400-500 crore for FY’15.

The Net Debt is at USD 537 million (majority foreign currency)as on 31stMarch 2014 declined from USD 604 million as on 31stMarch 2013. The Cash is USD 97 million as on 31stMarch 2014. It has repaid USD 67 debt I FY’14 and expects to bring down debt by USD 100-125 million in FY’15.It expects ARV Sales for FY’15 to be better than FY’14.

It expects to grow similar to what it is achieving for the past 2-3 years for the FY’15.

http://www.indianivesh.in/Research/ViewResearch.aspx?id=1

Indianivesh now comes with a buy report on Aurobindo Pharma with a target of 817 post good Q1 results

Highlights of the call by Capital Mkt:

The Aurolife continues to improve and post revenues of USD 26 million during the quarter. The operations are expected to further improve on the back of orders in control substances. It has 18 products pending with US FDA and 7 are control substances.

The Auromedics marketing the injectibles in US market and its revenues grew by 30% QoQ to USD 15 million during the quarter. It expects the sales uptick from the general injactables facility Unit 4 and expects 25% contribution to the Auromedics in FY15.

It has filed 376 ANDA’s with US FDA as on 30thJune 2014. It has filed 40 ANDA’s during the quarter out of which 12 are injectables. It has received 168 final approvals and 26 tentative approvals as on 30thJune 2014.

It has filings and approvals from various units are as follows: Unit 3 (Oral non beta-lactam products) â 119 filed, 114 approved, Unit 7 (Oral non beta-lactam products) 133 filed 36 approved, Aurolife (Oral non beta-lactam products) â 25 filed 7 (6 are control substances) approved, Unit 4 (manufactures injectibles) â 66 filed, 8 approved, Unit 12 (Manufactures Cephalosporin’s) - 20 filed 19 approved Unit 6 (Manufactures Cephalosporin’s) - 11 filed 10 approved and Auronext (Penem Injectibles) 2 products filed as on 30thJune 2014.The Revenues from the Europe witnessed sharp jump and inline during the quarter. This includes revenues from Actavis Rs 624 crore during the quarter.

There is growth in API’s business but mostly supplied to the internal purposes and growth will improved as the new capacities are coming up going forward.In Cymbatla there is price erosion but it is still profitable and the current market share is 40-45%.

The US market is growing on the back of inline business coupled with new product introduction business going forward. The US market growth expected to be driven by niche products, control substances and some me to products going forward. It still sees robust growth in US market going forward.

It didn’t expect any big opportunity up to FY’17 in the US market.It expects US FDA inspections/visits at Unit 7, Unit 4 and 3 in couple of quarter’s time.The EBIDTA margins without Actavis and the without the Cymbatla are 22% during the quarter.

The Company expects Revenue from Actavis to grow by high single digit to 10% for the FY’15. The EBIDTA loss expected to decrease to Euro 10 million in FY’15 compared to Euro 23 million previous year.The Company endeavor is to make Rs 400 crore as base for PAT level (including Actavis) going forward.The R&D expected to be 4.5% of Sales for the FY’15.The Tax rate expected to be 25% for the FY’15.

The Capex expected to be 600 crore for the FY’15 which includes maintenance Capex of Rs 120 crore. It is evenly spread among the API and Formulations.The Consolidated Gross debt is Rs 3337 crore and Net is at Rs 2695 crore as on 30thJune 2014.

The Debtor days declined to 92 days (traditionally 90 days) during the quarter compared to the 95 days in the previous quarter.

I think stock is ready to get re-rated from a PE of 16-18 to 20-24. The management has guided that they will be a able to book profits of 1600 crore for the current year. I think stock can provide good gains.

Highlights of the call by CapitalMkt:

The Aurolife growth is skewed towards control substances and the non-institutional business during the quarter. It grew in the range of 25-30% QoQ during the quarter.It has filings and approvals from various units are as follows: Unit 3 (Oral non beta-lactam products) â 119 filed, 114 approved, Unit 7 (Oral non beta-lactam products) 134 filed 36 approved, Aurolife (Oral non beta-lactam products) â 26 filed 9 approved, Unit 4 (manufactures injectibles) â 66 filed, 8 approved, Unit 12 (Manufactures Cephalosporin’s) - 20 filed 20 approved Unit 6 (Manufactures Cephalosporin’s) - 11 filed as on 30th September 2014.

The US base business is growing at very good pace. It indicated that experienced the channel consolidation from customers.The Cymbalta contribution is minimal during the quarter and expected further go down in the coming quarters.The Company filed 378 ANDA’s (40 in Q1 and 2 in Q2’FY15) with US FDA and out of theses 181 are pending for approvals as on 30thSeptember 2014.

The USFDA inspected Unit IV and gave process related observations and Aurobindo responded to US FDA and expects for further response from them.The sharp growth Europe market on account of Actavis sales during the quarter. Also, RoW market grew robustly and the key focus markets are South Africa, Brazil and Canada.

The Sales from ARV’s fell and qualitatively margins improved during the quarter. The margins are better than last year. However, it expects the robust growth in the H2 as the tender business skewed towards the second half of the year.The Vizag plant expected to be commissioned by the Q2’FY16.

The API growth expected to come from the Non-betalactam (not from the betalactam) due to expansion of capacities from Non-betalactam going forward. These were high margins compared to the betalactams.The Company confident on growth and expects growth momentum to continue going forward. It EBIDTA margins are expected to be sustainable at 22% going forward.

The R&D expected to be 4.5-5% of sales going forward.The Capex expected to be Rs 600 crore for FY’15 and expected to be in the range of 600-700 crore for the FY’16.The Net Debt is at USD 447 million as on 30thSeptember 2014 and decreased from USD 532 million as on 31stMarch 2014. The Cash and cash equivalents are at USD 83 million as on 30thSeptember 2014. It plans to reduce the debt by 25-40 million in the H2’FY15.

Screener.in doesn’t account for recent bonus 1:1 on 21st July. Hence P/E of Aurobindo shows at 14.99. Actual, its double = 30, which is at par with other players.

But good thing is that Aurobindo has a big pipeline of ANDAs and we are getting news of new drug approval almost every few days.

Anyone, tracking this closely?

yes i am following it closely. but i am a novice. still learning

Aurobindo Pharma on Thursday said it has received approval from the US

Food and Drug Administration (FDA) to market a generic version of

Prilosec delayed-release capsules, used to treat ulcer, in the American

market.

According to IMS, the product had an estimated market size of $422 million for the twelve months ot June 30.

In a separate statement, the company said it has received approval from the US regulator to market a generic version of Hoffmann-La Roche’s Boniva injection in the American market.

The company’s Ibandronate Sodium injection is indicated for the treatment of osteoporosis in postmenopausal women

I tried doing a basic search for the above products…

http://www.accessdata.fda.gov/scripts/cder/ob/docs/tempai.cfm

on this page I searched for Ibandronate Sodium. I didnt get Aurobindo pharma in the results

AURO got 2 approvals

Ibandronate for osteoporosis

Omeprazole for Peptic ulcer treatment

http://www.accessdata.fda.gov/scripts/cder/drugsatfda/index.cfm?fuseaction=Search.DrugDetails

http://www.accessdata.fda.gov/scripts/cder/drugsatfda/index.cfm?fuseaction=Search.DrugDetails

Closely following and invested in Aurobindo for almost 2 years now. Few notable points:

FY 14 numbers/margins/return ratios got a boost as company got day 1 approval due to a large drug (Cymbalta) and company did well to capture good market share in 180 days of exclusivity

Markets were not expecting the good show to continue in FY 15 and beyond due to large base of FY14, but still company delivered good y-o-y growth last year and sustained decent margins even after acquiring loss making operations in EU from Actavis.

Valuation multiples of Aurobindo compared to other similar peers have narrowed down to a large extent in last 2 years, however it still trades at discount compared to other mid cap peers.

Valuations also factor in margin profile, debt, pipeline, management’s past record, etc. Aurobindo does not screen best among all these parameters but when compared to other mid cap peers it does screen very good.

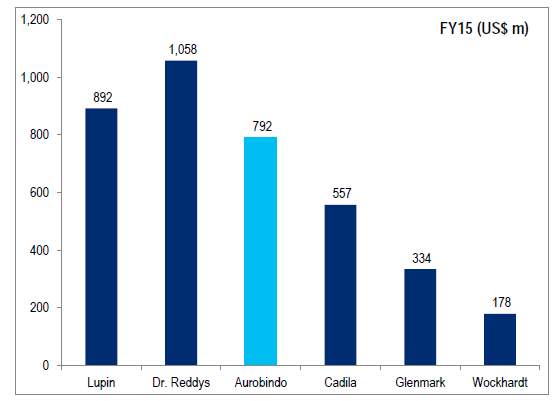

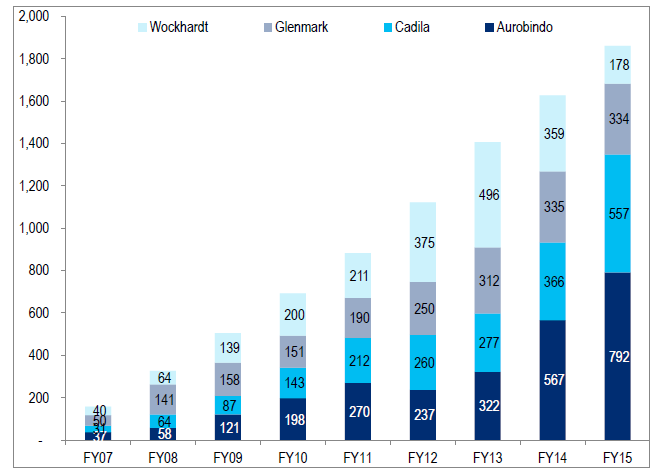

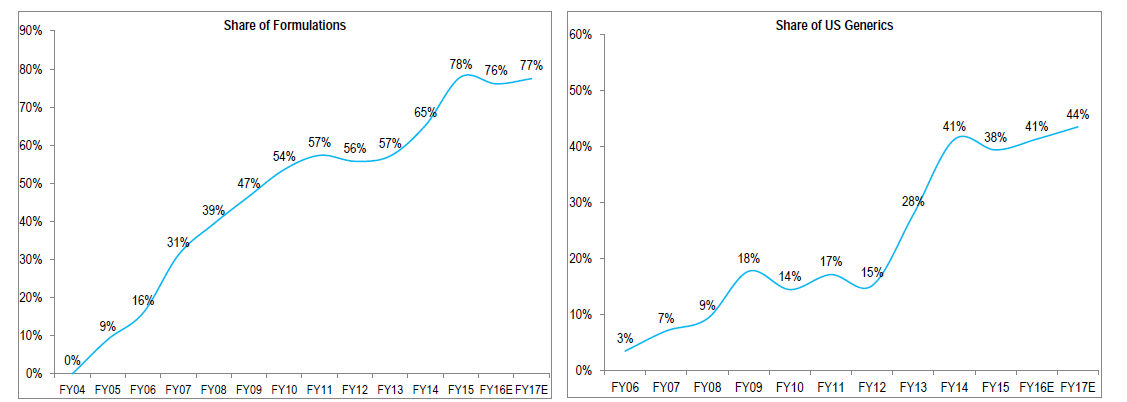

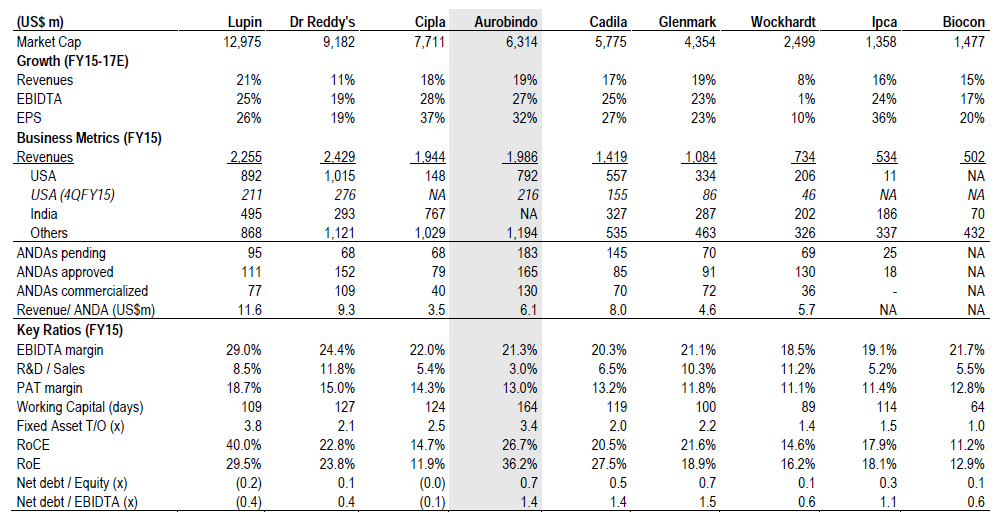

Some charts to put in context where Aurobindo stands

Revenue from US:

US revenue ramp up

Lastly, this tables sums it all

Overall, after N Govindarajan (current MD) came at Aurobindo around 2010 - the company went onto a different growth path. Street is still cautious about Auro’s sustainability of earnings and management quality (one the reputed broker on street have Auro’s TP at 414 vs CMP of 800+). One more reason for low valuations can be promoter group being closely related/linked to a political party in Andhra, which I believe is Ignorable. They recently hired Sanjeev Dani who was previously associated with Ranbaxy (google to find out about him)

I believe Auro clearly stands only behind Sun and Lupin in terms of scale/operations. Aurobindo have significant pipeline of ANDA’s (and backward integration) as can be seen from the charts and its injectable’s pipeline is also expected to contribute in a meaningful way in next 2-3 years. It should be noted that its current EBITDA margin of ~21% is including acquired loss making operations in EU, adjusting for that the EBITDA margins would be 25%+ (way above mid cap peers and comparable to large cap peer group). They target $3bn in revenue by FY18, read latest AR to find out more.

If USFDA plays no havoc - Aurobindo should do earnings CAGR of minimum 15% for next 2-3 years - that’s my take.

Disc: Invested and views will be biased.

Aurobindo Pharma receives USFDA Approval for Entecavir Tablets

Entecavir tablets are used to treat hepatitis B infection.

Aurobindo Pharma has received the final approval from the US Food & Drug Administration (USFDA) to manufacture and market Entecavir Tablets, 0.5mg and 1mg.

IMS data suggest, entecavir has an estimated market size of $294 million for the 12 months ending June 2015.

The company has now a total of 209 ANDA approvals from the US FDA.

entecavir approval.pdf (74.9 KB)

Aurobindo Pharma receives FDA Approval for Raloxifene Hydrochloride.

29 Aug 2015

Auro received the final approval from USFDAfor Raloxifene Hydrochloride Tablets 60mg.

It has estimated market size of US$404 Million for the twelve months ending June 2015 according to IMS.

This is the 45th ANDA to be approved out of Unit VII formulation facility in Hyderabad, India for

manufacturing Oral Non-Antibiotic products.It now has a total of 210 ANDA approvals.

Raloxifen.pdf (76.2 KB)

Hi @drrakesh

I was Searching the orange book of Pharma and for below two months found below approvals for Aurobindo Pharma:

TELMISARTAN

CETIRIZINE HYDROCHLORIDE

ALPRAZOLAM

RALOXIFENE HYDROCHLORIDE

ENTECAVIR

IBANDRONATE SODIUM

OMEPRAZOLE

Could you please help me in below points:

How to get Estimated Market size as you have mentioned for Raloxifene Hydrochloride in your post.

Also how much competition is there.

Regards,

Kapil

hi kapil,

Data about estimated market size you can find in company announcement section at bse & nse sites. Also IMS gives details about it.

About competition, what i do is reading various brokerage reports, company presentations, and of course google.

Also sites like pharma compass, drugs.com can help you.

I suggest you to go through this thread…

ValuePickr Generics Pharma Dashboards - Focusing on asking the right questions!

regards,

Rakesh

Anyone with technical analysis on Aurobindo please! What the charts say? Lupin showed resistance near 2100 3 times this year and we see bad Q2 results! How is Aurobindo looking on charts?

Aurobindo Pharma receives USFDA Approval for

Risedronate Sodium Tablets.

Aurobindo Pharma Limited announced that the company has received final approval from

the US Food & Drug Administration (USFDA) to manufacture and market Risedronate Sodium TabletsUSP, 5 mg, 30 mg and 35 mg (ANDA 200296). This approval is an extension of tentative approval received on 10th October 2012.

This product is ready for launch.

The approved ANDA is bioequivalent and therapeutically equivalent to the reference listed drug product

(RLD) ACTONEL® Tablets of Warner Chilcott Co., LLC Risedronate Sodium Tablets are used in the treatment of Osteoporosis.

The approved product has an estimated market size of US$113 million for the twelve months ending October 2015 according to IMS.

Aurobindo now has a total of 219 ANDA approvals (191 Final approvals including 10 from Aurolife Pharma LLC and 28 Tentative approvals) from USFDA.