Overall good performance

Company also undergoing huge capex in a 50:50 JV with an English firm to produce Yellow and Red Pigments.

Discl: Invested

Overall good performance

Company also undergoing huge capex in a 50:50 JV with an English firm to produce Yellow and Red Pigments.

Discl: Invested

Excellent results by Asahi !

Usually, Q3 is a dull Qtr for them as most of their customers are overseas marquee clients who follow calender year (Jan to Dec) as financial year. So in their last quarter (October to December) they go slow on buying to close the year with very low inventory.

But, despite this, the 25% jump in volume and revenue is huge plus for Asahi. it reflects on demand buoyancy and company’s increased marketing strategy.

The JV with TTC has already started and should ramp up in Q1. China is a major player in Azo pigments. With all buyers in international markets adopting for “China plus one” strategy, Asahi TTC should find it easy to sell their entire production and probably go for an expansion in FY 22. The expansion of next phases should be very “capital lite” as land, structure and utilities are already available at the site and only machine lines need to be installed.

further, TTC being an mammoth in colors The JV should find it easy to start new product ranges. TTC can be a ready buyer for them.

The fresh and young blood in form of Arjun Jay krishna (son of Gokul Jaykrishna) is clearly bringing in new vigour in marketing, quality and cost control.

all in all future looks very bright. It can well turn out to be “chupa rustum” of sunrise sector of speciality chemicals.

Disclosure: invested

How much can this JV contribute to the topline?

Let us look at how the company performed in FY2021 as the result are out.

Income statement:

(in lac)

| FY2021 | FY2021 | % Change | |

|---|---|---|---|

| Revenue from Operation | 28,308.02 | 28,363.98 | -0.20% |

| Cost of Raw material + Change in Inventory | 15826.15 | 17480.74 | -9.47% |

| Profit before tax | 4,363.91 | 2,326.79 | 87.55% |

| PAT | 3,194.62 | 2,282.63 | 39.95% |

The Revenue is flat compare to last years.

There seems to be no revenue from the JV yet, as the standalone and consolidated Revenue from the operation is almost the same.

The Profit has increased significantly, this could be due to the Crude oil prices correction in the first three-quarters of FY2021.

| FY2021 (lac) | Q1 | Q2 | Q3 | Q4 |

|---|---|---|---|---|

| Revenue from Operation | 5782.32 | 6228.21 | 7249.71 | 9047.78 |

| Cost of Raw material + Change in Inventory | 3128.34 | 3089.18 | 3784.62 | 5824.01 |

| Raw material cost as % of revenue | 54.10% | 49.60% | 52.20% | 64.37% |

As seen in the table the raw material cost was low in the first three quarters. Management has pointed out in the previous AR how the Curd oil price affects the Raw material price.

I think this advantage will not be present in FY2022 and the company needs to get the new plant to start the production of AZO pigments to have better results.

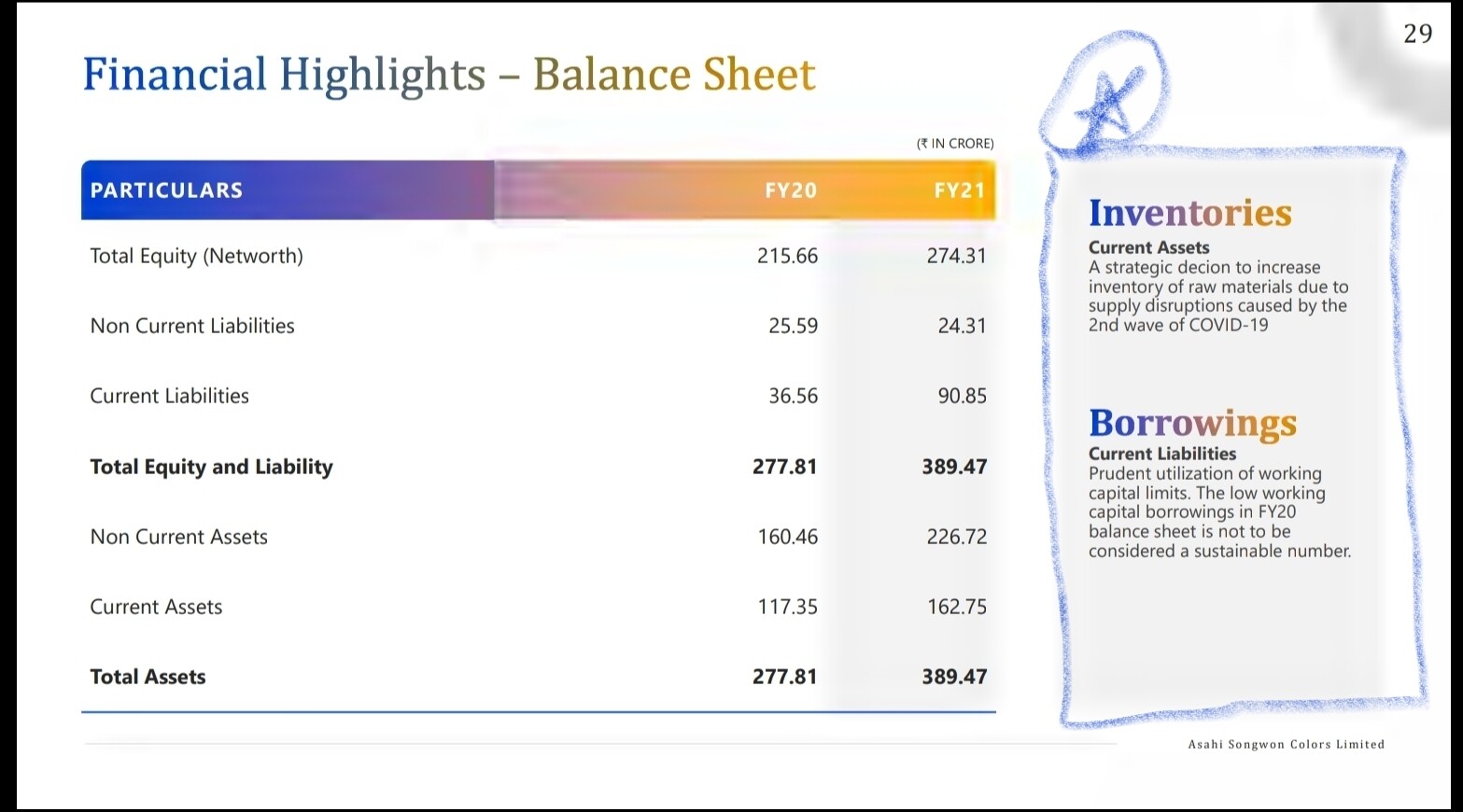

Working capital:

There is a spike in the Inventories and Trade receivable.

Also, Other current asset has increased.

![]()

This caused the Operating cash flow to reduce to 8 cr and increased the current borrowing by 33.85 cr.

![]()

Hopefully, once the new plants start operating and the working capital issue is reverse the company can start showing positive FCF next year.

Looking forward to reading the AR to understand.

Disclosure: Not Invested, in the watchlist.

They had their maiden concall today (a positive sign?)

The JV plant at Dahej for Azo pigments (yellow /Red/Orange) is done at a cost of 82cr creating a capacity for 2400MT.

Market is 70% in china and indian players together can certainly take a small share.

Further plan is to double capacity the moment they reach 50% utilisation.

Testing and sampling for both bulk pigments and few high margin pigments already started.

Having global MNC’s as clients for blue pigments they feel it ll be a quicker ramping up than it took for blue!

Plan to take it to 30% utilisation by the end of the year maybe 50% too…

we would be disappointed if we cant double our scale in 5 years!

Management was bullish and said that after 5 years of consolidation we have found our runway for growth. They said few years ago most of the clients suggested that indian manufacturers wont be able to compete with china but tide has turned due to various issues like rising geopolitical tensions, supply chain constraints and esg issues taking a front seat in china.

Execution needs to be tracked as story seems good

Shareholding:

Promotors have been buyers with some buying in the last quarter too.

Dolly khanna ji has taken more than 1% stake in the last quarter.

Discl: invested.

CFO of company resigned recently and joined another listed company named Arvee. I could not find reason for resignation. Any inputs?

How much range of revenue will company do in next 3 qtrs with new JV? Even a rough range will do

Bad result q3fy22

https://www.equitybulls.com/category.php?id=306317

Disc: invested

Asahi Songwon Colors acquires Atlas Life Science; Enters into API business. Details of same is as follow:

• Asahi Songwon Colors Limited has executed today i.e., April 18, 2022, a Share Purchase Agreement (“SPA”) with Atlas Life Sciences Private Limited (“ALSPL”) and certain identified promoters of ALSPL for acquisition of 100% stake in ALSPL in three tranches from certain identified promoters and other shareholders of ALSPL.

• The acquisition of shares under first tranche of 78% stake in ALSPL is completed today i.e., April 18, 2022 for a consideration of INR 48 Crores. Remaining shares representing 22% stake in ALSPL will be acquired in two tranches (representing 11 % stake in each tranche) for a consideration determined based on EBITDA prevailing for the period October O 1, 2022 to September 30, 2023 and October 01 , 2023 to September 30, 2024 respectively, in terms of the SPA.

• Atlas Life Sciences Private Limited is one of the leading manufacturers of Active Pharmaceutical Ingredients (API) and Bulk Drugs. ALSPL product portfolio includes Pregabalin, R-Compund, Phenylephrine HCL, Gliclazide, Amisulpride and Levosulpiride.

• Financial details of ALSPL:

o FY 2018-19 151.87

o FY 2019-20 82.26

o FY 2020-21 109.28 EBITDA 6 .92

My views:

From FY21 Financials it seem EBITDA margins of ALSPL are 6.33% which are very low and hence margin will be hit at the consolidation level. Clarity on the same is required from the company.

But otherwise it might give scale to there operations at consolidated level

Attaching the document

Asahi Songwon_ALSPL.pdf (317.1 KB)

Disc: invested. This is not a buy/sell recommendation. Please do your own due diligence.

Co. came out with press release on recent acquisition Few points on the same:

• Atlas is a leading manufacturer of Anti-convulsant, Anti-psychotic and Anti-diabetic APIs with a strong focus on product and process research.

• ALSPL’S Assets:

o Has a fully operational WHO GMP certified manufacturing facility in Odhav,

Ahmedabad

o Has a 4,000 square-foot state-of-the-art R&D facility

o Has a 5,000 square-foot corporate office

o Has a 15,000-square-meter land parcel in Chhatral with EC permission for 32

products, for future expansion activities

• SALIENT FEATURES:

o Incorporated in 2004 having 80 - member team strength.

o Key Products include • Pergabalin • R-Compound • Levosulpiride • Amisulpride •

Glicazide • Phenylephrine.

o Market leader in Pregabalin

o Established R&D center with team strength of 15 people

o 10 products under research and development, including 6 new molecules and

intermediates for existing products.

o Currently plant running at optimum capacity utilizations.

• KEY HIGHLIGHTS OF THE TRANSACTION

o The 78% acquisition of Atlas Life Sciences Private Limited will be financed through a

mix of INR 28 crores of internal accruals and INR 20 crores of debt.

o Asahi Songwon Colors will acquire an additional 11% stake in Atlas Life Sciences

Private Limited each year for the next two years based on performance metrics,

bringing the company’s equity stake to 100% by the end of FY25.

o Beginning Q1FY23, the existing plant will contribute to Asahi Songwon Colors

Limited’s consolidated financial results

o Mr. Jagdish Sheth, the current promoter of Atlas Life Sciences Private Limited, will

serve as a Joint Managing Director until March 2025.

o Asahi Songwon Colors will establish a new plant on the vacant land parcel in

Chhatral in order to backward integrate the existing products and introduce newer

high-value products.

o The Company intends to break ground on the greenfield project in Chhatral in July

2022.

o The greenfield project is estimated to cost INR 44 crores and will be funded through

a combination of internal accrual and debt.

o Co. aspire to more than double the existing EBITDA margins after the acquisition,

thus achieving much higher ROCE

Attaching the press release for same

Asahi_ALSPL_Press.pdf (198.1 KB)

Disc: invested. This is not a buy/sell recommendation. Please do your own due diligence.

does any one what is the management’s long term plan for entering into API business? Is it complementary to the existing business or company is venturing into new space? and what is their right to win in this space?

Asahi came out with an interesting press release.

Asahi.pdf (257.6 KB)

Asahi will use the proceeds of the land sale to reduce debt and capacity utilization of the plant has improved from 55% to 70%. The yellow line in Azo pigments has reached optimum utilization and a brownfield capex is being done to double the yellow line.

Along with this capex for the intermediates and api is ongoing. Overall management expects to reach 700-750cr turnover in next 2 years.

Aarti industries and Sudarshan Chemicals have both said in their conference call that the demand scenario for pigments is improving.

Asahi was struggling for the last two years after expanding capacities as the downcycle started. As demand improves margins should normalize and debt should reduce as there is no other capex plan.

Disclosure: invested

Asahi has good investments in last 2 years both in Azo and API, if they work out along with debt going down from peak debt that they mentioned in concall, it should be doing well. management seems decent, so hoping performance follows outlook.

disc: invested