arvind infra fy 16 concall.pdf (297.5 KB)

Given the pace of reform which would happen after UP results,Karnataka govt budget (Which happened today) - Positive for Arvind’s projects and RERA Arvind smartspaces should be doing incrementally better every years.Its a buy and hold for 3-5 years.Most small and unorganized players are struggling and it’s a great opportunity for branded and organised players like Arvind.Since they are yet to prove themselves and in general real estate low,valuations are pretty attractive.

Disclaimer:Have started investing for long term

Promoters stake increased by 5% plus with allotment of 25.75lakh warrants at Rs 88 per share.Its a huge positive with a vote of confidence.Today stock up 7.4%

Excellent results.Great strategic plan and Good corporate governance.Keep a watch on this company.Copy paste the below link to check the presentation on latest results.

file:///Users/sales/Downloads/Review%20Note%20Financial%20Results%20for%20Q3%20of%20FY%202017-18.pdf

[Review Note Financial Results for Q3 of FY 2017-18.pdf](http://Review Note Financial Results for Q3 of FY 2017-18.pdf)

Anyone still tracking this company…called Arvind Smartspaces now. The Q4 results going purely by financial statements were nothing much to write about. However, there seems to be some great transaction in the MIS Sales which are not yet recognized in reported financials due to the company following the project completion method and these revenues may be seen in upcoming quarters from Q2 FY22 onwards (I expect Q1 FY22 to be muted due to the pandemic) .

Their information disclosures have always been very detailed and the detailed Q4 information and project update is here

Their partnership with HDFC Capital has also gotten off the ground this quarter and as per the Concall the MD expects the launch of the project (horizontal project in Bangalore) within a year’s time.

Following the past discussions the company has flattered to deceive in previous years …but given the recent tailwinds for the real estate industry, impact of RERA wherein the branded players may be able to disproportionately gain, low debt levels, asset light balance sheet, focus on horizontal projects which may see demand due to COVID, and recent equity warrant issue to the CEO and MD are positives.

On the cons company seems to be very conservative and projects are concentrated in Gujarat and Bangalore. Also although backed by Arvind group this line of business has not featured as a priority for the group as far as recent media interactions are concerned so not sure how aggressively they may grow the business in the next few years.

Notwithstanding the cons, invested given the low debt and looking at their portfolio of executed and upcoming projects. Would love to have others thoughts if any of you are still following it.

Disclosure: Invested.

1 Like

44dc8c7d-a0bb-47c6-97e4-6a9e643cb0b2 (1).pdf (7.3 MB)

Good set of numbers for Q12022. Looks like the sales momentum continues. Not yet reflecting in the financial statements because of the the accounting standards but should reflect in the next 1 or 2 quarters.

Is there any live thread on Arvind Smartspaces/ Arvind Infrastructure

I thought this is live. As this community driven, if you fel it does not look like live, please make it live with meaningful posts!

is there anything changing? Last 5 years, looks like nothing changed in revenue or profit, rather they deteriorated as per screener when I had a quick look.

Numbers from investors PPT and screener are not matching.

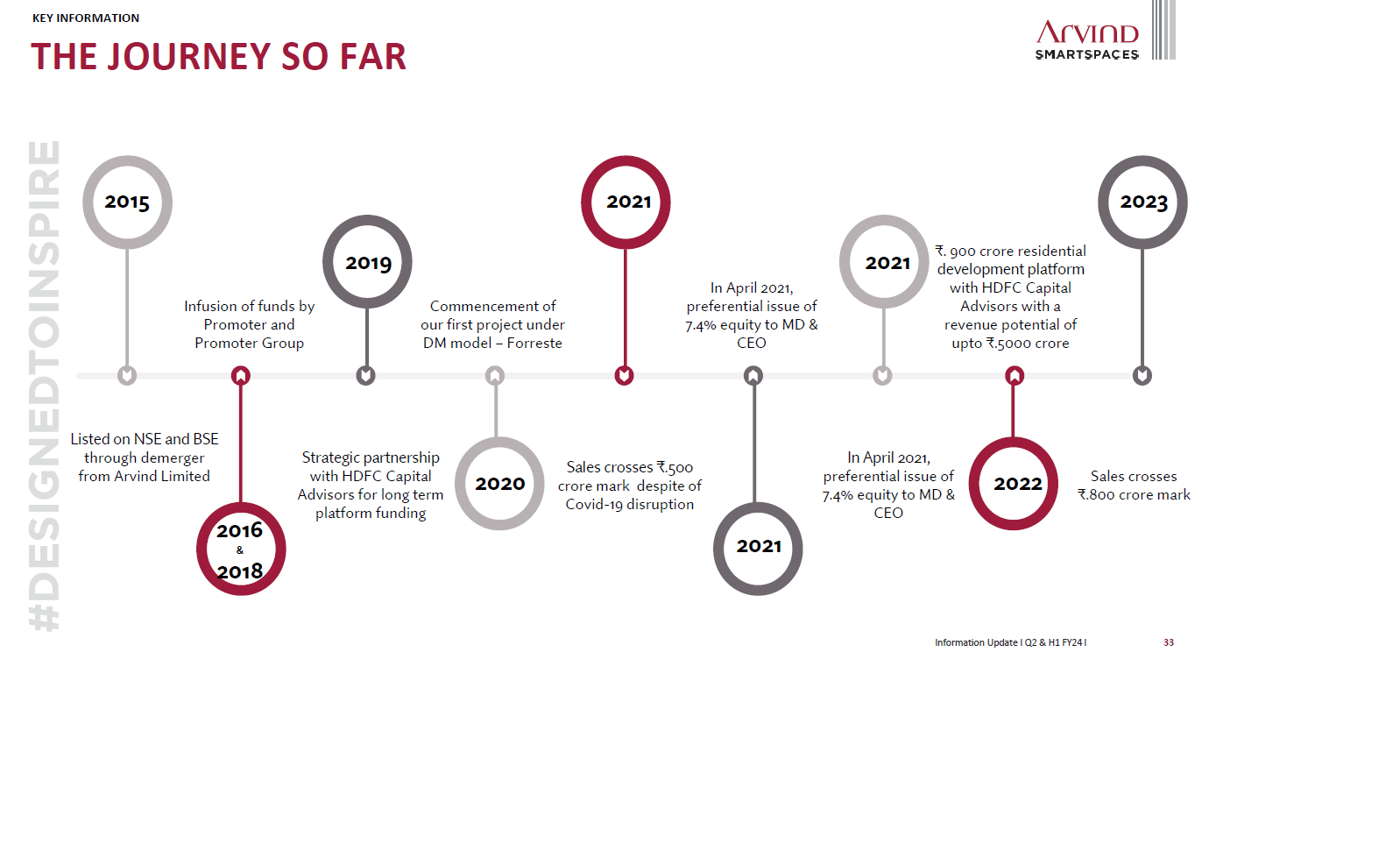

Sales 2021 - 500 CR

Sales 2023 - 800 Crore

They are projecting life time high of 1000 Cr sales for FY24 and are on track

I think this isn’t the sales (Revenue or Topline), it is a pre-sales kind of sales

As far as I understand , please correct if I am wrong.

They have three things,

Fresh sales (these are actual value of bookings)

Collections (Cashflow- based advances) ,

Recognised Revenue (RERA compliant- what % of built they deliver).

Ex: If a person books a 10Crore property (fresh sales) and pay 1 crore downpayment ( collections), revenue in this quarter ( zero).

Revenue Recognition: As per they deliver built as approved by RERA

The focus should be on Sales and cashflow, the recognised revenue is lagging and hence the entire Ebitda and statement doesnt give the right picture.

2 Likes

it is true and correct. They have an unrecognised revenue of 1900Crs

They usually deliver within 36-48 months, This 1900 crore will be recognised in next 3 years,at an EBIDTA of 20%, its ~400 crore in next 3 years, at a MCAP of 1600 crore, and Debt to equity of negative 0.3, Backing of Arvind group and HDFC as a 8-9% share holder. The operating MD was alloted 7-8% holding via warrants last year @110 last year and stock took off from there.

The way I see, If I can find a real estate company, where I trust the Management and also which has good DE ratio and I am sure it will not go kaput, I am comfortable investing.

This seems to be safe bet in terms of Price compounding at 25-30% CAGR for next 3-5 years.

2 Likes

Axis securities initiated coverage with target price of 1085. More than the the target price, the stock has now entered the main stream distribution, in few months, some more brokers will start coverage, now they will sell to their clients both individual and institutional.

The liquidity and participant of the stock will increase. After few quarters it might get included in broader nifty500/ 750 kind of index.

Most of the big realestate companies are are 4-8x mcap of their sales, Arvind is at 3x with better debt profile and lot of dry powder.

Above is a very rosy picture, but sometimes looking at upside is also important.

PS: Invested, biased with more than 15% in portfolio.

2 Likes

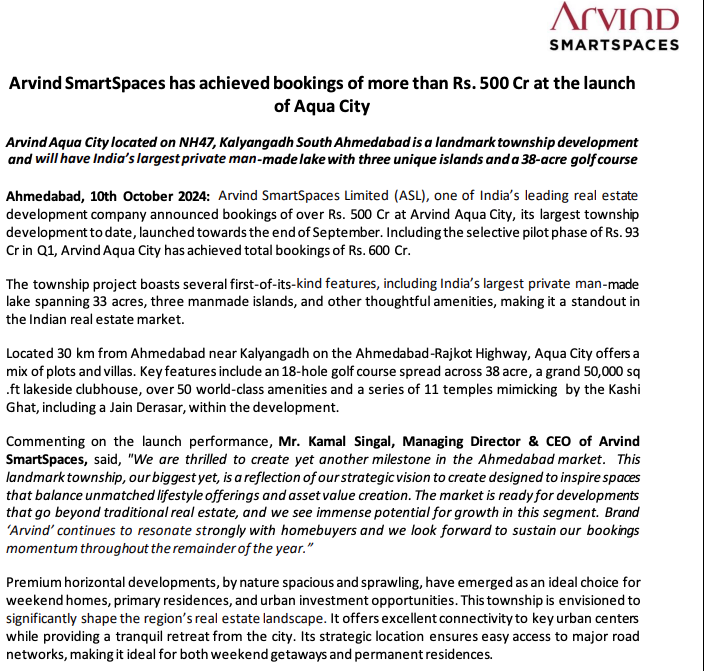

Step up in pace of project additions :

Arvind has launched 4 projects, and it is expecting to launch min 6-8 projects during FY25 as multiple projects are in active discussion to get signed in the coming quarters

Brand recall

Using its strong brand recall in Ahmedabad & Bangaluru markets as it has managed to quickly ramp-up its foothold in housing market in these regions. They also entered into Surat with a large deal and already scouting for deals in MMR region.

MMR region can be big approx 20% of the project mix.

Personally, i guess we can model Arvind Smartspaces to be at par with other leading listed players. They are asset light and they did show consistent growth in pre-sales, they also have faster turnaround visible via OCF generation.

Pre sales in FY26 43% CAGR over FY24-26E

Embedded margin 27%

Do note OCF conversion ratio here is 50% of collection coz of shorter cycle for horizontal projects. (79% of its total project portfolio consists of horizontal projects)

Dec

5.08% when they started last week

Stream of Promoter buying :

Its 5.14% as of today

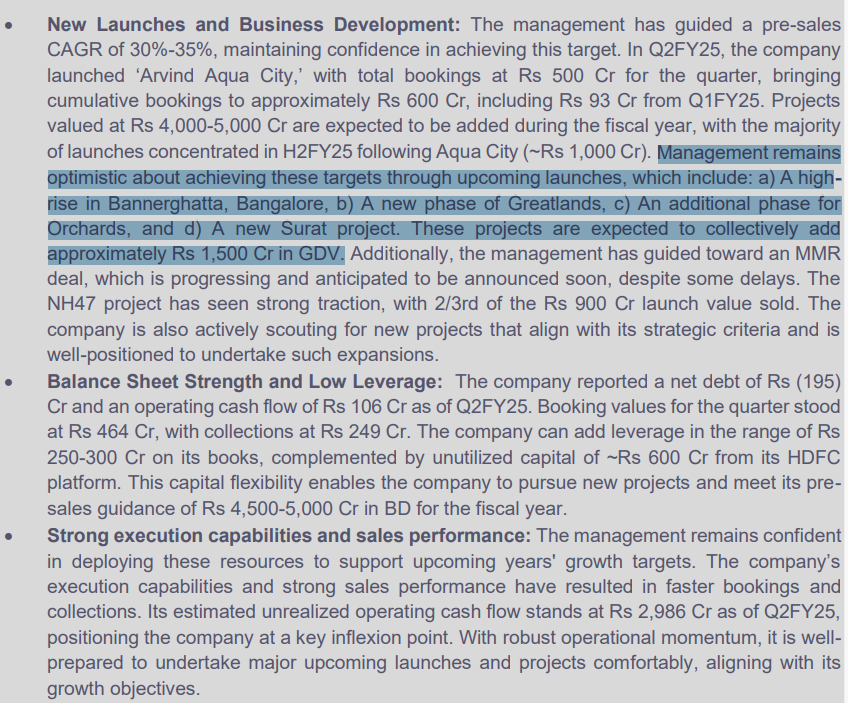

Promoters seems to be buying in this 5-10% correction. FY26 figures also look promising. Management seems +ve on achieving targets via upcoming launches.

- Bannerghatta bangalore

- New phase of Greatlands

- Additional phase of Orchards

- New Surat project

Collectively approx 1500 Cr GDV

Cashflows are super important : many mangements don’t talk about ROCE OCF - But Arvind Smartspaces are talking about this - something to note for a long term investor

Do note OCF conversion ratio here is 50% of collection coz of shorter cycle for horizontal projects. (79% of its total project portfolio consists of horizontal projects)

Arvind SmartSpaces enters Mumbai Metropolitan Region (MMR) with a ~Rs. 1,500

crore horizontal township project

4 Likes

Arvind SmartSpaces enters Mumbai Metropolitan Region (MMR) with a ~Rs. 1,500

crore horizontal township project

3 Likes

Large holder buying again from open market. Checkout the Px movement during the last 1hr please. Seem like a bullish sign given this particular person has been buying at higher levels too

Results

Arvind Smart Spaces Limited reported the following booking and collection figures for Q3 FY25:

- Bookings for the quarter stood at 224 crores, compared to 280 crores in the same period last year. This decrease is largely attributed to lending approval delays in the Bengaluru real estate market, which impacted one of their plotted launches.

- Collections grew strongly by 18% year-on-year, reaching 229 crores versus 194 crores in the same quarter last year.

It is important to note that while the Q3 bookings were down compared to the previous year, ASL’s 9-month performance has been the best ever in terms of both booking and collections. The 9-month booking value was 890 crores, a 14% year-on-year increase, and the collections for the 9 months reached 725 crores, a 10% year-on-year growth. These figures indicate a strong overall performance despite the specific challenges faced in Q3.