Arvind infrastructure: Godrej Properties in the making?

Investment Rationale:

-

They are trying to create a brand in real estate similar to godrej properties which they aim to make it into top 10 real estate brands in the country. Except for godrej there is no other, pan india, good real estate brand (Their website has its CEOs interview in business standard which mention this). Also their sponsoring the GIHED event (largest property event in Gujarat) and getting awards of Luxury project of the year (Uplands) and Emerging developer of the year-Residential (although most awards r purchased

) shows that they r investing a lot of money in creating a brand.

) shows that they r investing a lot of money in creating a brand. -

They r following asset light model i.e. not blocking capital in land and hence most of the project is executed on sales proceeds - which is only possible in future if they successfully create a brand and land owners come to them for joint development like godrej

-

Their current projects have revenue potential of 2500cr (as per the presentation on their website) thus even if u assume about 10-15% PAT margin for a real estate project (which is very very conservative) than the profit potential for all of its projects in next 4-5 years is about 250-350cr and today the whole company is available at 190cr market cap

-

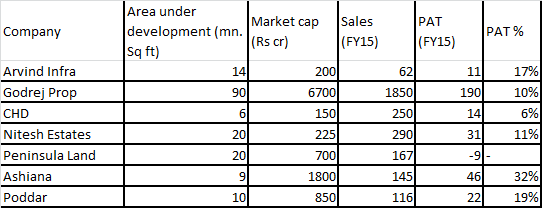

Another way of checking this calculation is that they r running projects totalling to about 1.5cr sqft as per the information memorandum…mostly in Ahmedabad and some in bangalore – taking profit per sqft of about Rs. 200-250 on a conservative side – the profit potential is 300-350cr and the whole company is available at 190cr market cap

-

Their largest project is Uplands in Ahmedabad where total revenue potential is Rs. 1200cr – as per the interview of its CEO on their website they sold stock of Rs. 200cr in such bad market till November 2014 – which was their full year’s sales target

-

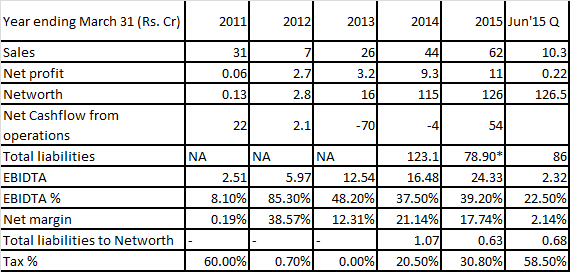

In 2015 they booked profits of Rs. 10 cr in the 6th year of their operation, even if they book say Rs. 100cr profit in 2018-19 (which is where some of their current projects r expected to get completed, so on a project completion method they will be booking profits in the year of completion) and it gets lets say 20 PE (Godrej gets 40 PE currently) than the market cap becomes Rs. 2000cr

-

As per the management interview all of their projects r cashflow positive i.e. their capital involved is negative

-

So in a nutshell – a good upcoming brand, good and clean management, available at dirt cheap valuation (less than next 4-5 years profits), with great business model, good cashflows.

Discl: Starter position at 70 levels

Relevent Links:

http://www.arvindinfrastructure.com/news_events.php

http://www.arvindinfrastructure.com/IM-Arvind%20Infrastructure%20Limited-24.8.15-Compressed.pdf

http://www.arvindinfrastructure.com/Investors_Presentation.pdf