This is excellent research. Thanks alot brother.

Hi, I came across this stock while searching for interesting micro-caps.

What surprised me the most was this.

Not only this business is cash positive since last decade but also all the debtor days, cash conversion cycle and working capital day cycles are drastically reducing. It’s definitely rare to find such a business at such valuations. So the point is - though it’s in Agri business, it doesn’t look like a classical cyclical commodity business.

And its undervalued on almost all parameters like PE of 15, P/S of less than 1 and PEG ratio less than 0.41 with a good promoter’s holding of 52%.

And on top of all this, it touched its all time high of 429 with one of the highest daily volumes on Friday 22 August 25.

Looks very interesting business to dig further.

Not invested as of now.

1 Like

Chairman Speech Summary [https://www.bseindia.com/xml-data/corpfiling/AttachLive/25cbc957-99d9-4f67-9a61-fd080703cb18.pdf]:

- New products launched include Aries Ecoshield, Majorsol Soybean & Pulses Special, Calmax, Zinc HD Gold, and innovations in equipment

- Domestic capacity utilization was 76.32% of installed 95,400 MT capacity, with the UAE plant producing 8,751 MT of specialized sulphur products serving both Indian and global markets

- Ongoing infrastructure expansion including the new Sulphur Bentonite facility in Jebel Ali, UAE, a new plant in Lucknow, and expanded office space in Vijayawada.

Future Scope:

-

Targeting Rs. 950 crore in gross revenue for FY 2025-26.

-

Financial Year | Annual Booking (₹ Crore) | Standalone Sales (₹ Crore)

----------------±---------------------------±---------------------------

2021-22 | 574.00 | 547.52

2022-23 | 664.04 | 609.97

2023-24 | 739.35 | 664.03

2024-25 | 830.44 | 778.35 -

Bookings for FY 2025-26 have surpassed ₹830 crores early in the year, reflecting optimism and strong dealer confidence

2 Likes

Hello all

I have come across this company by accident .There was news in business line about China stoped exporting fertilsers to India.

Possitive points

1.Raw material is not sourced from china

2.Its not in general category of business(NPK) its supplying micro nutrients

3.Orders are fixed in terms of advance from dealers

4.This has created CC(Working capital) requirement to zero

5.I had a talk with my relative who is dealing with fertiliser and asked product performance.As per him products are very good quality. Depends on soil, ingrdienits are changed, competitors are ICL,Mahafeed etc.It can be used to all crops.

6.Not subsidy based ,no price controls from government

7.finacial parameters like D/E ratio ,NPM,Working capital requirement are improved excep OPM which is declined

Negative points

Monsoon dependent

Please let me know your views

Regards

atul

Negative point

1 Like

Very well covered. Hope you have gone through my post on it on this page.

One major risk is the regulatory one. If the government decides to regulate the prices of all micronutrients, then all bets are off. ( recent case in point being the IEX)

ALSO Chinese dumping risk is always there.

Personal opinion.

Not invested.

ARIES AGRO – A Turnaround story & an Import Substitution Play

• ABOUT:

Incorporated in 1969, AAL manufactures and markets micronutrients. Aries Agro Ltd offers products in the primary, secondary and microfertilizer sector, ranging from individual elements to mixed specialty plant nutrient fertilizers.

Aries Agro makes high-yield products like chelates, water-soluble fertilisers, crop-specific blends, etc., that remain outside India’s subsidised group of bulk fertilisers. What this means is that Aries’ specialty products aren’t shackled by price caps or subsidy distortions. They enjoy better margins, their market is nascent and their import bill still looms large.

Products: Company offers bio-degradable complexes of plant nutrients, water soluble NPK fertilizers, value added secondary nutrients, natural and biological products and water treatment formulations. Currently, company has 134 brands customized based on crop, and Agro climatic requirements, with 21 organically certified products

It introduced the chelation technology for manufacturing micronutrients in India and is the market leader in the same. The company is the largest player in the domestic chelated micronutrients market and has steadily developed a strong marketing network to educate farmers and market its products.

Headquartered in Mumbai, the company has six manufacturing units in India in addition to an overseas subsidiary for sale of chelated micronutrients.

Overseas Subsidiaries:

Golden Harvest Middle East FZC (GHME; 75% subsidiary) and associate company Amarak Chemicals FZC (Amarak; 49% of equity stake held by GHME). In FY23, company opened a unit at Fujairah

Export Countries:

Nepal, UAE, Taiwan, Australia, New Zealand, Chile, United Kingdom, etc.

Promoter: The company is led by Dr. Rahul Mirchandani, Chairman and Managing Director, who brings over 30 years of experience and strategic depth, having been consistently ranked among the most innovative CEOs. He also holds key industry leadership roles, such as President of the Indian Micronutrient Manufacturers Association.

The promoters have been in the micronutrients industry for more than 50 years and have established the company as a market leader despite the high gestation period for product acceptability.

INVESTMENT THESIS

• TURNAROUND IN OPERATIONS

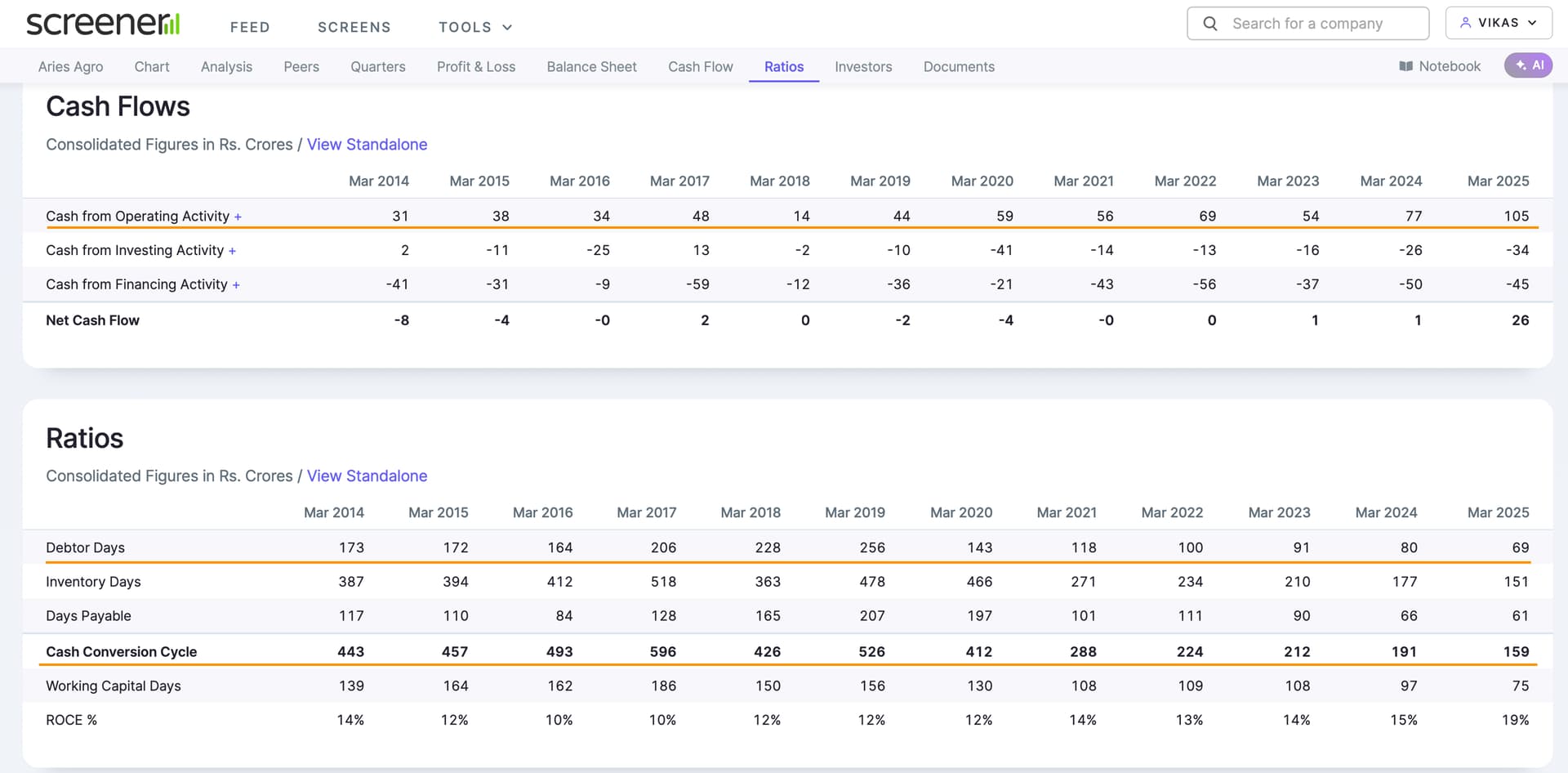

The Compelling reason to look at Aries is how the business itself has changed meaningfully in the last five years. From FY20 to FY25, revenue climbed steadily, profits nearly doubled and the balance sheet shed weight.

o 5-year sales growth rate – 16% CAGR

o 5-year EBITDA growth rate – 10% CAGR

o 5-year PAT growth rate – 32% CAGR

o 6-year reduction in Debt/Equity ratio – Reduced from 0.91 to 0.16

o 6-year reduction in Working capital days – Reduced from 156 days in 2019 to 74 days in 2025

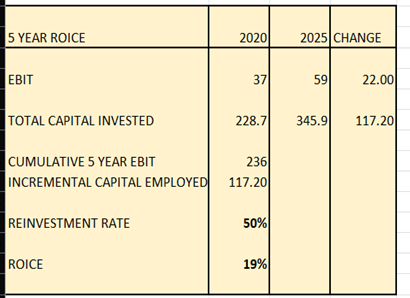

o ROCE improved from 12% in FY20 to 18% in FY25.

o ROE improved from 4% in FY19 to 13% in FY25

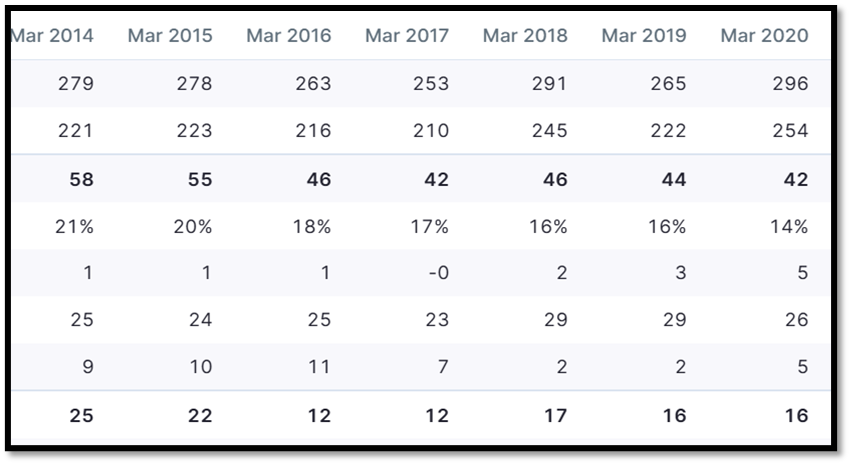

Before we get into the reasons for the turnaround, we have to first look at what went wrong in the period of 2014-15 to 2020

WHAT WENT WRONG:

There were two reasons for the poor performance of Aries from 2014 – 2020

Income statement from 2014-2020

- SHUTDOWN OF UAE OPERATIONS: M/s. Amarak Chemicals FZC, which is a Step-Down Subsidiary of Aries Agro Limited, had an installed capacity of 60,000 MT p.a. The manufacturing unit suspended its operations due to continued lack of power and movement restrictions in key raw material inputs (Molten Sulphur availability).

This led to reduction in sales and reduction in EBITDA margins.

- POOR WORKING CAPITAL MANAGEMENT AND HIGHLY LEVERAGED BALANCE SHEET: Aries’s Balance sheet was highly leveraged and it’s working capital days were highly elongated. This led to higher finance costs and thus profits went down. Thus, leading to poor rates of return on capital

As you can see, ROE was abysmal, finance costs were taking 2/3rd of operating profits and Balance sheet was leveraged.

- Competitively Aries didn’t seem to have anything special. Some comments from Valuepickr Forum in 2018:

“Check from the trade, every Tom, Dick & Herry is selling micro nutrients. There is no product differentiation. Longer credit and higher margins to trade are the only ways to sell. All MNCs and Indian players are having 5-6 micro nutrients products in their portfolio. How this small company would be able to compete, that is a big question mark.”

“Believe me, I am in distribution business of Agro-chemicals. There are 100 other companies selling micro-nutrients similar to Aries. Sales are all linked to longer credit period and higher margins and retailers/distributors like me shift our purchases every year. There is no brand pull from farmers level for the non-established brands like Aries. Customer is dependent on retail -channel for credit so trade decides which brand to push.”

Aries leveraged balance sheet, elongated working capital cycle and poor returns on capital were all demonstrative of the above competitive comments. Even though EBITDA margins were in the range of 16-20%.

But change was coming and one can see from 2020 numbers that improvements were beginning to take place in the background.

**THE TURNAROUND AND HOW IT HAPPENED:**

o STRENGTHENING BUSINESS MODEL & FUNDAMENTALS

THE ADVANCE BOOKING MODEL AND OFFTAKE ASSURANCE:

What drove the shift was not just what the company sold but also how it ran itself. The leading factor was its strategy of deploying advance booking: asking farmers and dealers to pre-book their orders digitally and in advance. Through its ‘booking bazaar’ app, dealers could commit months ahead of the season. That visibility turned production from guesswork into planning. Its factories planned production more rationally and scheduled dispatches, managing inventory efficiently.

The company actively seeks advances from its distributors, which serves the dual purpose of managing the working capital cycle efficiently and securing guaranteed off-take for its manufactured products. This model provides high visibility into future demand.

Although the customer advances entail an interest component that impacts the operating margin, the management accepts this cost as a calculated trade-off. The expense on the operating margin is significantly outweighed by the substantial reduction in the risk associated with high inventory carrying costs and reliance on external, high-interest fund-based working capital limits.

(Of course, there is no free lunch. Aries pays interest on dealer advances and offers booking discounts, which inflate finance costs and compress reported margins. But the trade-off of headline profitability for cash-flow stability has still made the business sturdier.)

By securing off-take assurance and transferring the capital carrying risk to the distribution channel, AAL ensures financial stability and accelerates its deleveraging efforts.

Furthermore, the advance booking model provides an institutional buffer, ensuring a large portion of the revenue pipeline is secured irrespective of immediate seasonal concerns.

Pre-booking would not have worked without trust. Aries built that over decades through product demonstrations, soil-testing drives, weekly farmer meetings and agronomy sessions. Farmers saw yield improvements and began asking for Aries’ products by name. Dealers, reassured of demand, were willing to put cash down early.

The results showed up in working capital. Receivables shrank, inventory turns improved and credit dependence fell.

o BIG IMPROVEMENT IN FINANCIALS:

Every metric is showing substantial improvement.

Customer advances have increased a lot in FY23-FY25 showing increased trust in the company from dealers.

(Return on incremental capital employed has been very healthy over last 5 years)

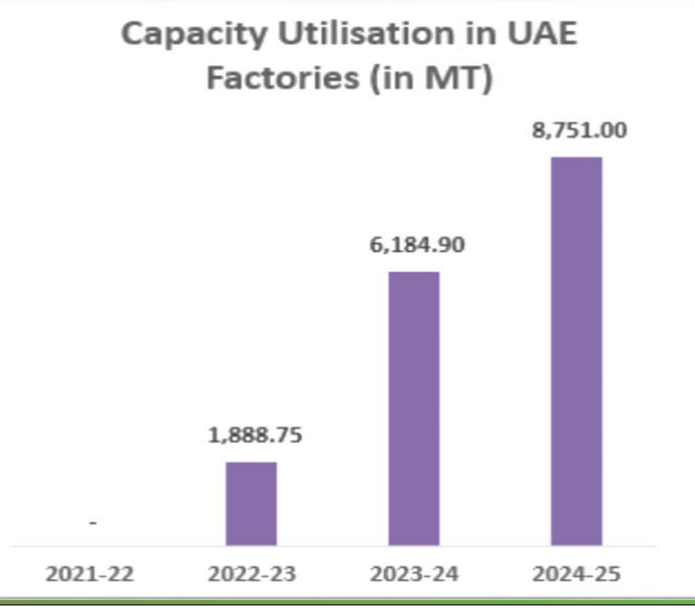

The company’s India plant utilisation climbed from 67 per cent in FY21 to 76 per cent in FY25, aided by steady production schedules and fewer costly expedites.

Its capital discipline, as the company channeled cash into reducing debt, automating plants, expanding warehouses and funding incremental capex, also helped the business improve.

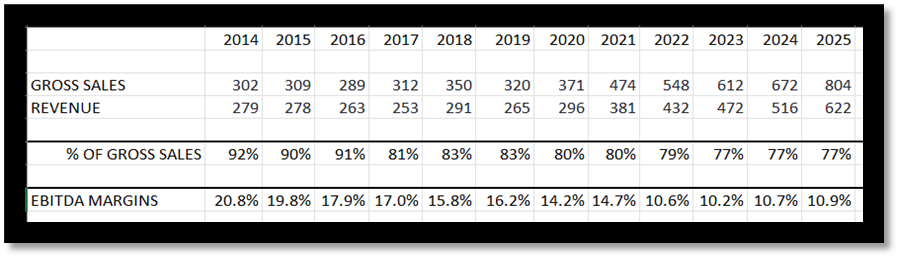

o EBITDA Margin evolution with advance bookings model

Ebitda margins have declined as the rate of discounts have increased. Discounts have Increased in proportion to advance bookings.

And this has directly resulted in improved cash flows and working capital metrics. Advance bookings lead to neatly planned production which is very important for reduction in inventory carry because of big number SKUs. Inventory days were 212 in 2020. Now down to 85

Aries management has sacrificed front line ebitda margins to strengthen overall business fundamentals over the long run. That’s actually very rare and saluteworthy.

Even though Ebitda margins were 15-20% from FY15 to FY21, ROCE was only 10-12%. Now it’s reached 18% (15% in FY24,14% in FY23. Consistent improvement)

o

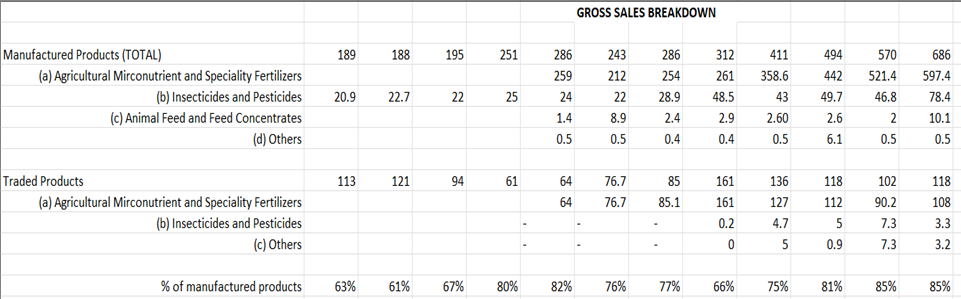

% of manufactured products increasing consistently over % of traded products in overall gross sales. Another sign that fundamentally business is improving.

And now the transition Period is complete. Ebitda margins will be maintained/improved only. Advance bookings and discounts help have dealer loyalty. Sales growth will continue at a healthy pace.

o UAE OPERATIONS TURNAROUND:

In fiscal 2020, the company roped in a UAE-based partner, Odyssey Global, and divested 26% stake to mobilise resources and restart operations.

Operations were restarted in FY22 and have been gaining momentum.

This has helped increased profitability and revenues.

Evidence for UAE operations gathering momentum. Purchase of goods from associates was nil in 2021

I believe Company is sourcing raw materials from UAE factory and finished goods through wholly owned subsidiary Mirabelle Agro. Mirabelle commenced operations in 2022 and had a big jump in sales and profits in FY25 – Directly corresponding to increasing UAE operations.

-

Mirabelle Agro Manufacturing Private Limited –

During the year under review, the Company achieved turnover of Rs. 5,268.18 Lakhs compared to Rs. 1,371.96 Lakhs in the Previous Year. The Company has earned Profit of Rs. 746.47 Lakhs compared to Profit of Rs. 28.89 Lakhs in the Previous Year.

The Company started its Trading Activities during the Financial Year 2020-21 and Manufacturing activity in Financial Year 2021-22. The Company is fully operational and engaged in both the Manufacturing and Trading activities. The Company also added the Plant Protection Range to its Product Portfolio.

Loans and advances of Rs 75 crore were stuck in the UAE company. Further, with the help of the joint venture partner, the company has been able to recover loans and advances and is expected to recover Rs 10-15 crore per annum going forward. In FY25 company received Rs. 12 crores in lieu of loans and advances given to group company GHME (o/s reduced to Rs.44.39 crore as on Mar.31, 2025) and is expected to receive repayments of Rs. 10 crores this fiscal (Rs 5 crore already received). Evidence –

![]()

(This was 73cr in FY22)

With operations in Amarak gaining momentum in Fujairah, the group expects to penetrate international markets.

UAE CAPACITY EXPANSION: Amarak Chemicals, part of Aries Agro, has announced plans for a new $14 million plant nutrients manufacturing facility in the Jebel Ali Free Zone.

The new facility will specialise in the production of 60,000 metric tonnes of sulphur and allied value-added products annually.

The strategic rationale for this capacity addition is twofold: it provides a cost-effective and sustainable supply source for raw materials to India, thereby reducing dependence on imports, and acts as an export hub serving the GCC region and beyond. This lowering of import dependency is specifically projected to contribute to the medium-term improvement of AAL’s operating margins.

So, with UAE operations expanding and Indian operations having undergone a significant turnaround, Aries is set for strong and sustainable growth for the future.

• IMPORT SUBSTITUTION THEME:

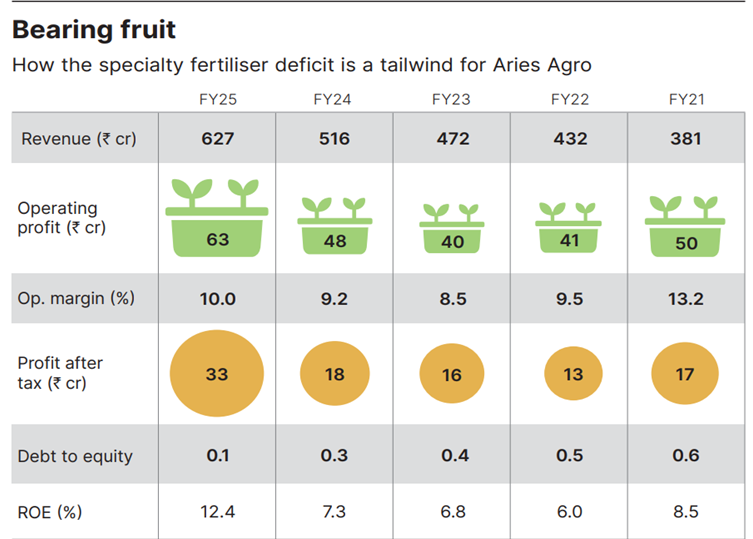

As China halted its specialty fertiliser shipments earlier this year, India caught the chill. Local prices spiked as the country’s heavy reliance on imports for its farming nutrition was laid bare. But every cloud has its silver lining. This is especially true for domestic specialty fertiliser players for whom this adversity hides an opportunity: filling in the import-dependent supply gap.

The market opportunity: The market backdrop is equally promising. India’s water-soluble fertiliser market, where Aries primarily operates, could grow to $650 million by 2030, a growth of 7–8 per cent a year. India’s annual consumption sits near 0.6 million tonnes but 80 per cent of it is imported.

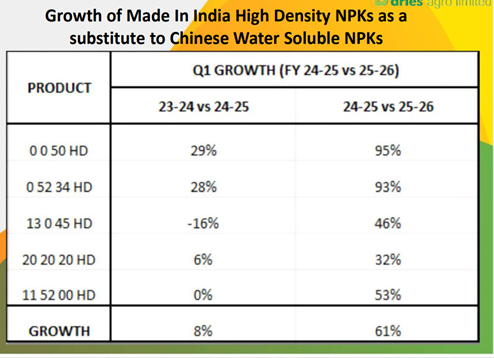

Over the past decade, Aries deliberately cut import dependence and developed in-house substitutes like its high-density water-soluble fertiliser line (high concentration of nutrients with small water-soluble particles for better absorption)

Aries’ own sales of water-soluble fertilisers have surged from 2.7 crores in FY22 to 24 crores in FY25, more than doubling each year. Yet, given the sheer scale of imports, the headroom remains vast. Every tonne produced domestically substitutes imports, trims volatility and feeds the government’s indigenisation push.

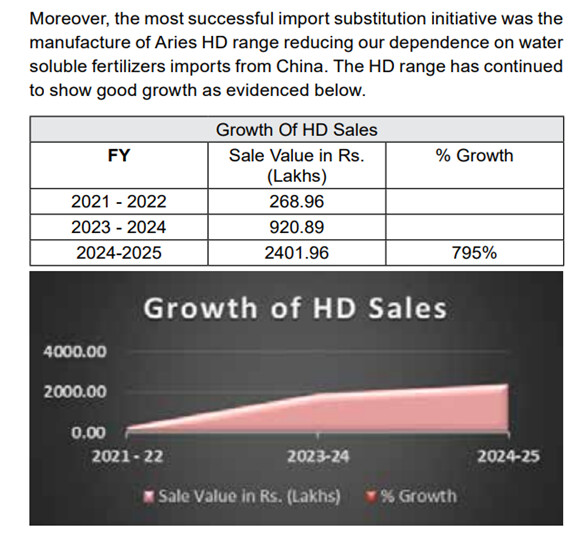

Aries is progressively reducing its import dependence. Moreover, the most successful import substitution initiative was the manufacture of Aries HD range reducing our dependence on water soluble fertilizers imports from China. The HD range has continued to show good growth.

Our Make in India and import substitution initiatives have reduced our percentage of imported raw materials from 51pc in 2018-19 to 18pc in 2024-25.

Going forward Aries should continue to benefit from import substitution tailwind.

• STABLE GROWTH & LONG RUNWAY FOR GROWTH IN INDUSTRY:

Indian micro nutrient market is witnessing promising growth attributed to increasing awareness regarding crop nutrition across the agriculture industry in India. The growing population, emergence of advanced technologies, and government facilities that boost the adoption of micronutrients to improve crop health and yield are anticipated to fuel the market growth in the coming years. India’s water-soluble fertiliser market, where Aries primarily operates, could grow to $650 million by 2030, a growth of 7–8 per cent a year.

The extensive farming practices such as the wide use of chemical fertilizers and burning crop residues in the past have led to the degradation of Indian soil. This has also negatively affected the health of consumers. However, the awareness regarding soil health has increased among farmers in recent years. The growing knowledge about the maintenance and improvement of soil health has significantly improved Indian agricultural practices. The increasing knowledge of the positive relation between soil health on plant growth and yield is expected to amplify the growth of the agricultural micronutrients market during the forecast period.

In India, intensive farming and changes in environmental conditions, such as increase in global warming, are the major factors, which contributed to the depletion of micronutrients in soil. Hence, crop cultivation in micronutrient deficient soils has adversely affected the crop yield, thereby leading to crop losses. Additionally, lack of adoption of timely soil testing has hampered the sustainable production of agricultural crops in India.

Thus, fortification of fertilizers with essential micronutrients is an efficient solution to eliminate the aforementioned problem as various micronutrients are able to deal with a wide range of soil conditions/problems. Moreover, the increased demand for high-quality and fully-developed fruits, vegetables, other horticulture, and ornamental crops worldwide is projected to play a crucial role in augmenting the demand for micronutrient enriched fertilizers. Thus, micronutrient fertilizers are gaining widespread recognition as they are the best fit for modern sustainable agriculture.

One of the biggest priorities/challenges worldwide is to increase the yield per acre of arable land. Arable land is always in limited supply so governments of every country are trying to figure a way out to get more from the same space. This makes the business a very important one, giving me some confidence on the sustainability of it.

• CAPEX:

The company has signed a contract for a new Sulphur Bentonite facility in Jebel Ali UAE. Amarak Chemicals, part of Aries Agro, has announced plans for a new $14 million plant nutrients manufacturing facility in the Jebel Ali Free Zone. The new facility will specialise in the production of 60,000 metric tonnes of sulphur and allied value-added products annually.

The company Broke ground on a new plant in Lucknow and expanded its office in Vijayawada.

63cr capex done in last 2 years vs 68cr capex in prior 6 years.

• GROWTH GUIDANCE & MARGIN IMPROVEMENT:

FY26 Sales Guidance: Our Annual Booking for FY 2025-26 has already recorded bookings worth Rs. 830.44 crores from 1,717 dealers across 26 states. We are targeting Rs. 950 crores in gross revenue for the current year.

“Revenue is expected to grow at 8-10% over the near-to-medium term driven by increased awareness among farmers of the benefits of micronutrients owing to education initiatives undertaken by the company.

Operating margins were stable at 8.4% in FY25 as compared to 8.6% in FY24. Thereafter, the operating margin is expected to improve to 8.5-9.0% over the medium term, with sustenance of gross margin aided by calibrated price hikes, lowering dependance on imports and better operating leverage” – Credit report

UAE Capex to improve margins: The strategic rationale for this capacity addition is twofold: it provides a cost-effective and sustainable supply source for raw materials to India, thereby reducing dependence on imports, and acts as an export hub serving the GCC region and beyond. This lowering of import dependency is specifically projected to contribute to the medium-term improvement of AAL’s operating margins.

• EXPORTS:

Internationally, Aries expanded its footprint with strategic engagements in Australia, Brazil, New Zealand, Nigeria, Nepal, Philippines, Taiwan, and the UAE, and participated in key expos including the CAC Expo (Shanghai), Horti Agri Next (Thailand), and PMFAI (Dubai).

International Sales have shown significant growth, which includes Sales from the Aries Branch in Fujairah, UAE and from our Associate Company, Amarak Chemicals FZC, UAE.

Exports are projected to grow going forward with UAE expansion.

• GST 2.0 TAILWINDS:

Under “GST 2.0”, the Goods and Services Tax (GST) rate on micronutrients and bio-pesticides has been reduced from 12% to 5%, making these inputs more affordable and encouraging the adoption of sustainable and eco-friendly agricultural practices. This change is a component of broader tax reforms aimed at boosting the agricultural sector and supporting farmers and small organic farms.

The rollout of GST 2.0 has brought encouraging changes for micronutrients under the Fertilizer Control Order, especially with the reduction in GST rates that directly benefits the farming community

Reforms in GST 2.0 should further strengthen the demand buoyancy of Aries Agro’s flagship micronutrients portfolio.

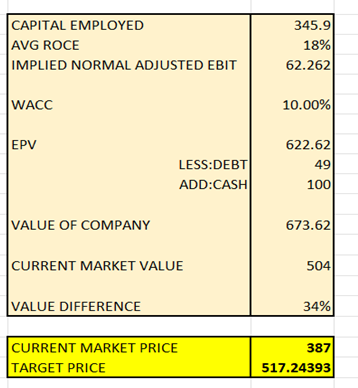

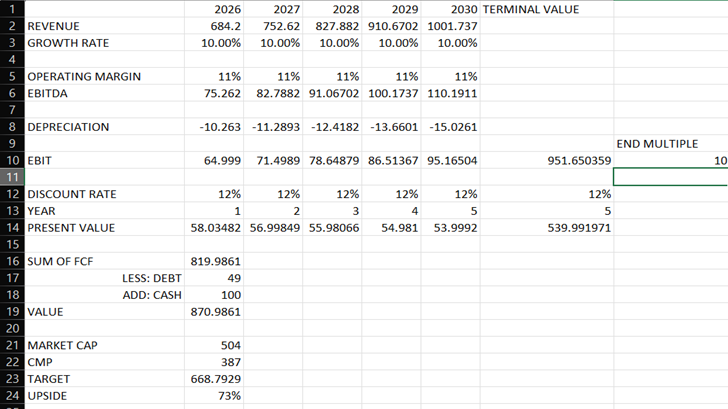

• CHEAP VALUATIONS:

Company is currently trading at very cheap valuations given the turnaround that has happened fundamentally and the presence of growth drivers going ahead.

PE – 14, EV/EBIT – 7.9.

ROCE has touched 18%, ROE at 13%. If ROE and ROCE improve more, there could be a possibility of big re-rating.

OCF was 105cr in FY25. Market cap is 500cr. FCF was 72cr. Trading at 7x market cap/FCF.

(Steady state valuations / DVP)

(Using very conservative estimates)

• STRENGHTS & OTHER POSITIVES

The company will continue to benefit from its wide product portfolio, established brand image and wide reach of over 10000 distributors.

o MARKET LEADER & IMPROVING MARKET SHARE:

The ratings factors in the established position of AAL in the organised micronutrients market, its improving market share, wide product basket, strong distribution and marketing network, and extensive experience of the promoters.

AA is the leader in the micronutrients space

o NO CORPORATE GOVERNANCE ISSUES:

There have been no qualifications by the Statutory Auditors in their report on the Accounts of the Company for the last 15 (Fifteen) years. The Company shall endeavor to continue to have unqualified Financial Statements.

- Promoter salary is fair.

- No suspicious related party transactions.

- No unnecessary investments in shares or land

- No bad debts

o DISTRIBUTION STRENGTH:

Strongest dealership network pan india present.

o MARKETING:

Its advisory approach remains a key marketing catalyst: soil testing and crop-stage guidance funnel farmers towards its products. Advice builds trust, trust drives repeat purchases and repeat business strengthens the network.

It has invested in grass-root level marketing by deploying its marketing staff in villages to educate farmers, convince opinion leaders and demonstrate the effectiveness of its products.

As per my understanding of the business, it has a small but expanding moat. The distribution network has been painstakingly created. The management has, over the years, gone state by state, village by village to create awareness. It now has a very large distribution network, covering almost every state in India. Farmers did not know what they had been missing out on by not using micronutrients. This has been a very tedious job. There is no easy way for even a large established player to replicate this. Farmer education requires time, money and effort and AA clearly has the headstart here.

o INCREASING PRICING POWER? -

In fiscal 2025, gross revenue improved by 19% yoy to Rs 804 primarily driven by realization growth as company passed on the price increases to its customers. While volumes in the micronutrients segment remained marginally flat, agrochemicals segment witnessed volume growth albeit on a low base.

Most of last 5 years sales growth is driven by value growth (newer products, hike in existing products etc). Another positive sign. Is the pricing power of the business increasing?

o WIDE & CUSTOMIZED PRODUCT PORTFOLIO: It has continuously added new nutrient formulations (on an average 5-6 products new products launched every year) to meet changing requirements of farming regions and provides a wide range of related products and services, further strengthening its brand.

Customization: No two crops or soils are the same, and Aries embraces this diversity. It has developed crop-specific formulations that are updated every few years based on extensive soil testing data.

o Increase in FII and DII in June Qtr

RISKS

o COMPETITION RISK – INCREASING DISCOUNTS RISK:

Competition is looming as the specialty aisle is no longer empty. Fertiliser giants are scaling their lines, global brands are localising and nimble regional players remain quick-footed. The battleground is often discounts. Discounts have crept up as firms fight for dealer mindshare. Some of this is rational, firms have to seed new products and defend shelf space, but left unchecked and it risks eroding Aries’ cash flows gained from digitisation.

Exposure to intense competition: The company faces competition from unorganised players, which comprise around 60% of the market. The industry is characterized by low entry barriers owing to low capital investment and limited product differentiation. However, with increasing customer awareness and farmer education, demand for its products should increase. Also, with stricter government regulations with respect to quality of products, unorganized players are getting eliminated, benefitting companies like AAL

“I am not sure how difficult it would be to market micro-nutrients if one day an established player plans to venture into this space. Well awareness is improving, distributors/dealer network is already established for an established player in similar space (for instance pi or excel or some seeds company), much deeper pockets than AA, so why cannot this be replicated?” – Valuepickr forum

Dealer network cannot be called moat. Same dealers are probably dealers of seed companies and other crop chemical companies. – Valuepickr forum

It might be that the pie is too small for larger companies to look at this business vertical at the moment. What if the pie actually increases? – Valuepickr forum

Believe me, I am in distribution business of Agro-chemicals. There are 100 other companies selling micro-nutrients similar to Aries. Sales are all linked to longer credit period and higher margins and retailers/distributors like me shift our purchases every year. There is no brand pull from farmers level for the non-established brands like Aries. Customer is dependent on retail -channel for credit so trade decides which brand to push. – Valuepickr forum

(These valuepickr comments are from 2016-2018, fundamentals have changed since then, yet it’s a good reminder on the fragmented nature of the industry)

o WEATHER RISK:

Vulnerability of the micronutrients sector to rainfall: Micronutrients are used for correcting nutrient imbalance in soil and improving the land/crop productivity. Rainfall and its distribution over time and space is one of the basic determinants of micronutrient consumption. The fortunes of the domestic micronutrient industry are therefore linked to rainfall. Surplus or inadequate rainfall could affect revenue and profit margins of domestic players. Despite increasing awareness among farmers about better irrigation mechanisms, a substantial area under cultivation in the country is still not well irrigated and depends on rainfall to meet water requirements. As the group derives a major portion of its revenue from domestic markets, it will remain susceptible to the vagaries of monsoon.

o POLICY RISKS:

Policy is another uncertainty. Specialty fertilisers may be unsubsidised but they are still regulated. Tighter standards or knee-jerk price caps could squeeze spreads. Here, Aries’ defence is the same one that enabled advance bookings: its brand pull through which farmers ask for its products by name because they see tangible yield gains.

o OTHER RISKS:

-

Low awareness among consumers: One of the other major restraints to growth of the agriculture micronutrients market is the lack of awareness among farmers in developing countries regarding appropriate dosage and proper application of micronutrients, limiting demand. As per international standards, 4 kg of micronutrients are used per 100 kg of fertiliser, while in India, only 870 gm of micronutrients are used per 100 kg of fertilisers. However, with the company taking steps towards farmer education, awareness among farmers has improved, which will also increase the offtake over the medium term.

-

“However, the progress of the 2025 monsoon has been erratic, with rainfall distribution marked by monthly anomalies and regional disparities. While certain geographies received early and excessive showers, large swathes of the country faced extended dry spells followed by late bursts of rain. This uneven pattern has significantly influenced the Kharif 2025 season, leading to delays in sowing in some states, crop stress in others, and a mixed outlook for yields overall. For the Agri-input industry, such fluctuations have impacted the timing and intensity of demand, underlining once again the importance of agile supply chains, farmer engagement, and product positioning that can withstand the unpredictability of climate trends. We are preparing for erratic demand patterns through automation, enhanced warehousing, and better inventory controls. We do hope to close the current financial year not too far from our projections.” – Chairman’s speech 2025

o LACK OF CONCALLS AND QUARTERLY PRESENTATIONS

o For last 5 years, share application money has been paid to Amarak yet shares haven’t been allotted yet.

o M/S. Golden Harvest Middle East FZC is non-operational for years and is loss making in the range of 5 to 6crs each year.

(I think it’s because it’s the holding company of Amarak. Once operations scale even more, this might change)

• MISCELLANEOUS

• (FACEBOOK) (8k subscribers on YT)

• The Ministry of Agriculture and Farmers’ Welfare has reported that the total area sown under Kharif crops in India has reached 1121.46 lakh hectares as on October 3, 2025 — surpassing last year’s coverage of 1114.95 lakh hectares. The overall increase of 6.51 lakh hectares, representing a 0.6% rise over the previous Kharif season, reflects resilience and strong farmer participation despite varying monsoon conditions across regions.

According to the data released by the Department of Agriculture & Farmers’ Welfare, several major crops including rice, pulses, maize, and sugarcane have shown significant area expansion this season, with maize recording the highest increase among cereals. The improvement in sowing figures suggests a positive outlook for Kharif 2025-26, bolstered by supportive government policies, timely rainfall, and enhanced seed and input distribution at the state level.

• INVERTED DUTY STRUCTURE ON SOME PRODUCTS IN GST 2.0: The Central Board of Indirect Taxes and Customs (CBIC) has assured the Indian Micro-Fertilizers Manufacturers Association (IMMA) and the Fertiliser Association of India (FAI) that a speedy refund mechanism will soon be notified to address concerns over the inverted duty structure faced by micronutrient manufacturers.

At a meeting held on Friday at North Block, the CBIC chairman acknowledged industry concerns over the higher goods and services tax (GST) rate of 18 per cent on inputs. He said a notification on refunds would be issued alongside the GST 2.0 notification.

IMMA also pressed for uniform GST treatment for all micronutrients covered under the Fertiliser Control Order (FCO). The CBIC noted the representation and said the matter would be referred to the Ministry of Agriculture for further action.

On dealers’ demand for refunds of GST paid on stock-in-trade, the Board clarified that such refunds are not permissible under law and must instead be adjusted against future liabilities.

The industry bodies further sought a level playing field in GST treatment of notified micronutrients across manufacturers, traders, and importers. The Board reaffirmed that the current inverted duty structure would continue as long as multiple GST rates remain in place.

FINAL WORD:

• Long term growth in speciality nutrient industry+ highly improving business fundamentals (working capital, cash flows, return ratios) + UAE operations gathering pace+ big increase in advance bookings make it a buy

Competition is a risk that must be kept in mind.

• Even though the risk of competition is tugging at me and saying do a slightly smaller position, The fact that overall advance bookings have increased by nearly 20% and advances from customer have increased from 47 to 81 cr

And the fact that they have 115% ocf / Ebitda and such a huge improvement in working capital metrics, tells me that the company is doing something really good. The distributors & farmers WANT their products. That’s why they’re booking big amounts in advance.

And plus, UAE operations tailwind is a hidden driver of turnaround. In valuepickr forum, I didn’t see it mentioned much anywhere…but it was the downturn in uae operations that caused a lot of problems for Aries and now it’s being turned around.

• The only downside risk (That too short term) is erratic rains playing spoilsport yet mbpl has reported best ever numbers (as a fertilizer company), so that risk too seems not much. Monsoons have been bumper which means rabi crop will also be very good.

• India’s specialty fertiliser crunch may be the tailwind Aries Agro needed

Aries’ strategy fits in neatly. It is widening its manufactured portfolio where it has process expertise, not merely adding more products. Investments in automation and logistics ensure that advance bookings convert into timely, cost-efficient deliveries.

Aries Agro today sells more of what it makes, relies less on imports, plans production earlier and turns cash faster. In a market where one exporter’s whim can jolt supply chains, this predictability is a moat. If Aries resists the temptation to erode margins through excessive discounts, there is a large market waiting for it. The chill from China’s supply shock may have paradoxically given the company just the opening it needed.

The wide product basket of the group, its well-established position in the domestic chelated micronutrients market and extensive experience of its promoters will help maintain healthy business risk profile over the medium term.

• The only way I can see this investment thesis going wrong is that competition becomes too much leading to stagnating revenue growth and pressures on margins and cash flows. But with the industry growing at a good speed & import substitution theme being present & also the long gestation required to market, raise awareness & build a brand & the company being the market leader in this space, this risk seems not too much currently. But it needs constant monitoring.

DISCLOSURE - INVESTED. CONVICTION - HIGH

5 Likes