WestBridge is continously selling and now its holding is below 15%. Next round of selling can reduce this overhang from the stock. Looks undervalued when compared to its past multiples. Can the final exit of PE take it back to its past valuation??

1 Like

This is not an undervalued opportunity.

The price-to-book ratio is a sound valuation metric when the book value is used to its full capacity. Aptus has an inflated book value with a very high capital adequacy ratio.

Price to book will only go up -

- when they gradually give more loans and get their capital to work.

- Even if they give dividend to lower book value (Very unlikely). Suddenly price to book will automatically increase…

There is another trade off -

Growth Vs RoA

- If they want industry leading growth, difficult to manage NIMS and RoA

-If they want RoA, very fast growth is not possible without riskiness

But this doesnt look like a cheap valuation to me..

2 Likes

Should they give back the extra cash to shareholders and reduce book value?

And dilute later on when the demand arises at a higher valuation. I feel the cash is sitting idle right now.

This is making the company inefficient. At 7.5% RoA, nbfc should at least do 30% RoE. They are doing 18%, only 2.5x leveraged.

I feel they should at least give back higher fraction of profit every year. At this high RoA and conservative dividend, they will never need to dilute like other nbfc.

2 Likes

What is the reason for a decline in the stock price even after good results?

People are assuming Real estate will get affected due to all this tariff drama.

Tarriff shall disrupt IT/Pharma/etc. and hence maybe, maybe it would lead to defaults in housing sector.

Aptus is a core housing finance company, so it can get affected the most. Just my analysis of why real estate is in pressure since last week.

Yet,

I think we are heading for overall economic recovery, in terms of long term economic cycle. Just my 2 cents.

1 Like

II think the market is reacting to concerns about asset quality. Gross NPAs have gone up by 30 basis points quarter-on-quarter. In general, many lenders—including big banks—are seeing stress among sub-prime borrowers, especially in microfinance, where borrowers often don’t have formal jobs or strong financial backing. So, the market might be assuming that Aptus could also face similar issues going forward, which is a real possibility.

However, unlike credit cards or microfinance loans, Aptus mostly gives out secured loans, and their loan-to-value (LTV) ratios are much lower than what’s common in the industry. So even if there are defaults, the impact might be cushioned since the company can recover money by selling the collateral.

I don’t think this is the reason. Aptus focuses on providing affordable housing finance and small business loans to underserved, low- and middle-income, self-employed individuals primarily in Tier 2 to Tier 4 towns. IT and Pharma employees are not the target clientele of Aptus.

7 Likes

I partially agree with @pramaan. I have independently analyzed this company and holding it since last 1.5y so I know the dips are happening due to:

- impact of tariffs is slightly complex. labour intensive sectors such as textiles, gems & jewellery, furniture, carpets, etc may struggle. labour + white collar employee layoffs may happen in tier 2/3 cities where these industries are located. These people could be customers of Aptus. In fact, all small lenders including HFCs and SFBs will be impacted. To what extent impact will happen? tbh nobody can quantify it, not even management.

- recent surge in competition which the all companies’ management have recognised. Just read latest concalls of Aptus and Aavas. So many players have listed + new players have entered via PE funding since I bought the stock. It’s not easy to find promising home buyers now. The market might be huge but the profitable market of customers who won’t default is small. So many players would mean slowdown in growth.

- Westbridge might sell their stake further. It’s a normal thing. Every PE fund sells their stake within a few years after listing. Just see what happened with Aavas last year and what’s happening in Nuvama currently. I personally don’t find it a problem. Maybe temporarily stock will remain underpressure but long term it will deliver.

As far as micro finance defaults are concerned, RBI warned about this and advised unsecured lenders to cut back. Aptus already being cautious in its SME loans. Housing loans aren’t affected by this reason (largely). A small increase in stage 3 GNPA is acceptable.

Disclosure: Invested and continue to hold it unless the tariffs become a major structural problem for tier 2/3 folks. By Q3 concall we should get a concrete clarity on this.

6 Likes

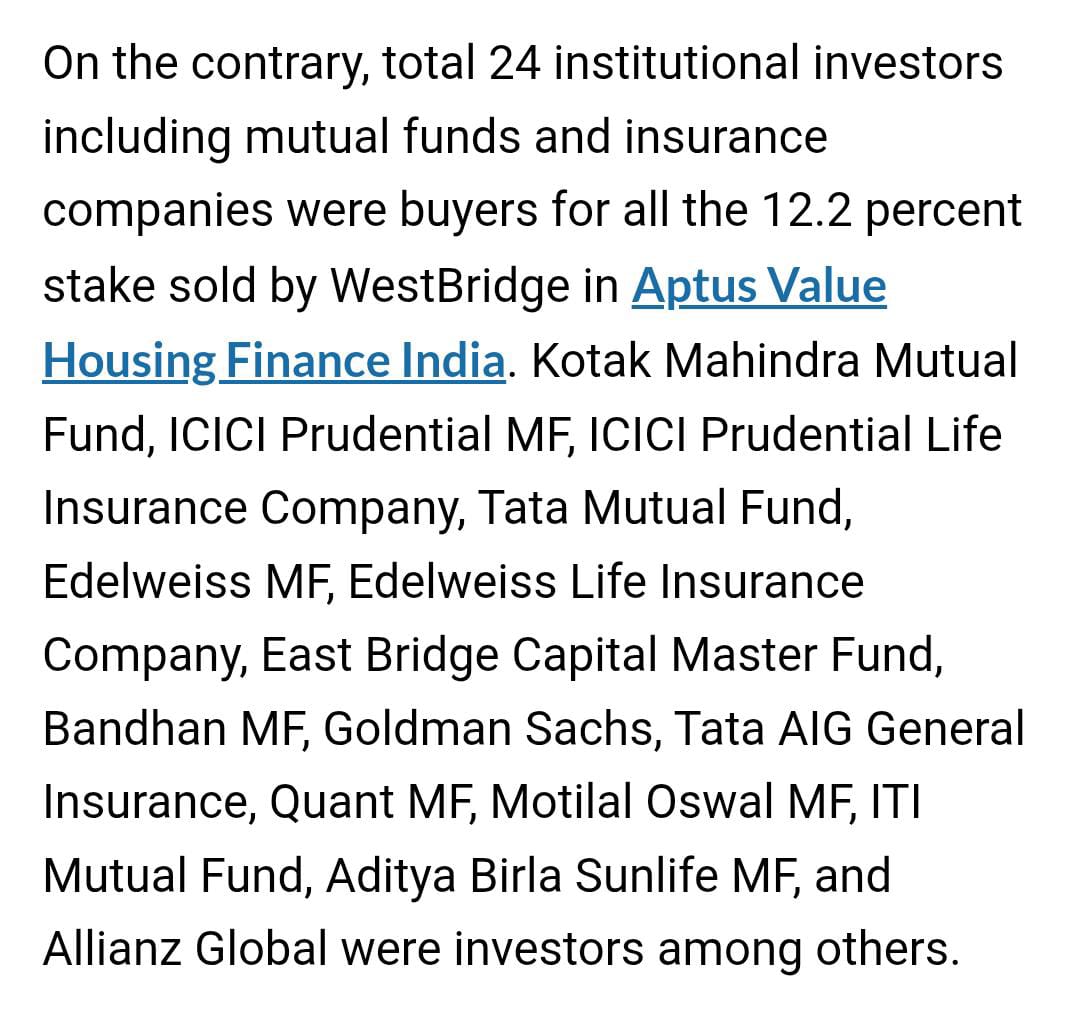

Aptus Housing Finance – Supply Overhang Cleared

Over the past 4 months, WestBridge Capital has exited nearly its entire position in Aptus Housing Finance, offloading ~28–29% stake. The key positive is that this large supply of shares was fully absorbed by Indian institutions, reflecting confidence in the company’s fundamentals and future outlook.

With this overhang now behind, the stock may have more room to reflect business performance without the pressure of large block sales.

Disclaimer :invested, not a buy sell recommendation;

4 Likes

Can someone please explain Pledged percentage 47.6 % ?

this is against 40.4% of promotor holding, not the overall company. Could be required for raising the capital from Investors. I am not sure about the reason not closely tracking the company. But this is quite normal.

Why is the stock so weak? The Q3 numbers were quite good, except for growth - which the management clarified that they slowed down growth considering the stress in rural areas. They have guided for 22% to 24% growth going forward. Anythiing else that is worrying the markets about this stock?

1 Like

I think succession worries. And global uncertainty in general

AUM in 2021 was at 4068 crs and it is now at 12,330 crs- a very healthy CAGR growth of around 24%

NIM that was at 11% in 2021 has increased now to 13.10% and

NPA that was at 0.49% is now at 1.18%- not a very high number considering the very high NIM.

The small business and non-home loans as a %age of the total AUM was at 23% in 2023 and has now increased to 29%.

Even though the management has been trying its level best to explain that everything is under control, market participants are not convinced that this performance is sustainable in future considering the high NIMs in the risky segment that it operates and the steep growth seen over the last 4/5 years

1 Like

as long as NIM is in control, growing quarter on quarter should work well, It’s bit surprising the stock is not performing, although PE exit has turned to trusted DII entries, still the stock is not performing. Only reason I could think of is management is not trying to plaything anything gamble here, otherwise the price shall reflect and push forward to 500. Sometimes old school management to good to be true

Aptus Value had approved a proposal to amend the Articles of Association (AOA), subject to shareholders’ approval.

The key proposed amendments were:

-

Promoters will have the right to nominate directors to the Board

-

Promoters will have affirmative voting rights on certain reserved matters

-

Promoters will have rights related to quorum requirements at Board meetings

Today, Voting results of Postal Ballot was released.

And, you may find that Votes against (50.93%) exceeded votes in favour (49.07%) and there was 75% requirement for a Special Resolution.

Upon checking, category-wise. You’ll find the below breakdown:

Promoters: 100% in favour

Public-Institutional: 74% voted against (main reason the resolution failed)

Public-Non Institutional: 99.97% voted in favour (but their influence is relatively less)

So, you can say that, institutional investors deliberately and effectively blocked the resolution.

There could be several reasons, however, I feel that the prime reason could be to not let the promoter hold significant control over them and weaken their own control/influence.

7 Likes

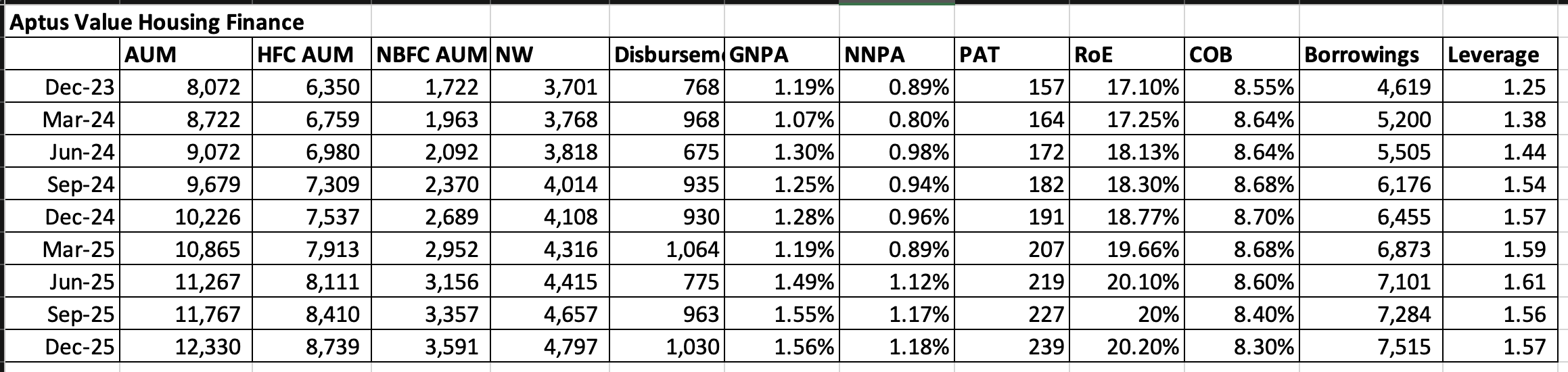

The stock of Aptus Value Housing Finance has been in a sustained downtrend over the last six months. On September 4, 2025, Westbridge Crossover Fund (investor-promoter) sold remaining stake.

Logically, one would expect the removal of this persistent “supply overhang” to stabilize the stock. Instead, the price has nosedived since mid-August 2025 . Looking at the data of a Bank or NBFC/HFC is inherently limiting as these firms can simply not recognise their NPAs, and as such, continue to post very good results. Investors have very little insight in the actual health of the loan book, specially, where loan book is very granular as is the case with Aptus. One can just look at how Yes Bank unravelled, where the bank continued to hide asset quality issues for years despite their having lent to leveraged corporate groups was public knowledge. With that in mind, and assuming that the asset quality issues, if any, are correctly reported by Aptus, I decided to look at key financial parameters to understand the reasons for the price action.

Key Financial Data (Dec 2023 – Dec 2025) from quarterly investor presentation

Looking at the table, no clear conclusions could be drawn. However, the market seems to be pricing in three specific risks:

-

Product Mix Shift: The NBFC loan book (often higher risk) has grown from 21% to 29% of the total AUM. Management’s admission of stress in this segment would have market bracing for further deterioration in asset quality.

-

Deteriorating Asset Quality: While still low in absolute terms, GNPA has crept up from 1.07% to 1.56% over the last 21 months.

-

Growth Moderation: The management has walked back its ambitious AUM target of ₹25,000 crore by FY29.

Looking at the key financials in the table above, the sharp fall in the stock price seems a bit overdone compared to how the business has actually performed. RoE has improved from 17% to 20%, and that too with very conservative leverage of just 1.57x.

Even if disbursements stay muted—especially after the recent decision to stop sanctioning loans below ₹7 lakh—AUM growth of more than 13% would still imply a PEG ratio of under 1, which looks reasonable from a growth-versus-valuation perspective.

What I find most comforting is the low leverage. The balance sheet is quite strong. Even in a stress scenario with meaningful write-offs (say 25%), the company would likely remain solvent. Not many lending businesses can say that.

Disc- Invested and Biased. I am novice and not a registered Investment advisor. Please do your own due diligence.

7 Likes

I think the narrative around this being a major promoter power grab is a bit exaggerated.

There weren’t any new economic rights being introduced. The earlier structure was linked to Westbridge as an investor promoter, with certain thresholds attached. With Westbridge no longer involved, that clause had effectively become redundant. The amendment was largely an alignment exercise rather than a dramatic shift in control.

Promoter-nominated directors would still go through NRC review, board evaluation, fit-and-proper criteria, and shareholder approval. Those governance checks remain unchanged.

Yes, the promoters would have had the right to nominate a majority of the board and certain affirmative/quorum rights. But this has always been a promoter-led company. The structure of the business hasn’t suddenly changed.

At the same time, operational performance remains strong — 20%+ growth, around 20% RoE, and 16 years of operating history in a regulated lending environment, with meaningful promoter skin in the game. That combination is not very common in today’s market.

The recent issues seen in parts of the low ticket-size lending space also remind us that disciplined growth and underwriting matter more than headline expansion.

To me, this vote seems more about differing views on governance philosophy — particularly around balance of control — rather than about the company’s fundamentals or credibility.

The business metrics remain intact. The debate is more structural than operational.

3 Likes

Why I Continue to Hold Aptus (Despite the Noise)

Been reading multiple threads on Aptus — growth concerns, promoter selling chatter, peer comparisons. Sharing my view in simple terms.

- Promoter Skin in the Game

Deep promoter ownership is not talked about enough.

M. Anandan (Chairman & Promoter) continues to hold a meaningful stake. This is not a widely dispersed, institution-driven NBFC.

MD P. Balaji has been running operations with continuity for years.

In lending, alignment and stability matter more than presentations and quarterly commentary. - Why Not 25–30% Growth?

Yes, some peers are growing at 25–30%.

But growth doesn’t come free.

Many fast-growing lenders operate under:

PE timelines

AUM acceleration pressure

Market expectation of constant scale-up

Aptus doesn’t seem to chase growth at the cost of underwriting. After seeing what over-expansion did in affordable LAP and MFI cycles, 20% disciplined compounding doesn’t look bad at all.

20% steady > 30% with future credit shocks. - “Risky Customer Segment”?

The perception is that it lends to small-ticket South-based LAP borrowers.

If that risk was structurally flawed, how has the company managed:

Stable asset quality

Strong spreads

Consistent performance

for ~16 years?

Either underwriting is more robust than assumed, or the narrative is overstated.

Track record across cycles deserves some weight. - Return Ratios

This is where the debate usually becomes quiet.

Who else:

Does LAP + small-ticket HL

At comparable yields

Maintains high spreads

Delivers strong ROA/ROE

And still compounds ~20%?

If they cut rates aggressively to chase growth:

Margins compress

Niche weakens

Market says moat gone

They’re choosing profitability over optics. - The Rumour Cycle (led by Glorified Journalists or some of the sell side analysts as you call them)

Every few months:

Promoter selling

Too much promoter control

Chola acquisition

NBFC licence cancellation

At some point, we have to separate noise from numbers.

Stability in management is underrated in financial businesses. Sudden transitions haven’t ended well for many lenders. - Dividend Discipline

Not many growing HFCs consistently return capital.

That reflects:

Capital comfort

Earnings visibility

No desperation for aggressive balance sheet stretching

My View

Aptus isn’t a narrative stock. It’s a discipline-driven lender.

Promoter skin in the game

Controlled growth

Strong return ratios

Long underwriting track record

For me, that fits the definition of a value pick.

If quarterly noise bothers you, it may not be ideal.

But if you can look past chatter,

Aptus Value Housing Finance India Ltd

still looks like a steady compounder in the making.

5 Likes