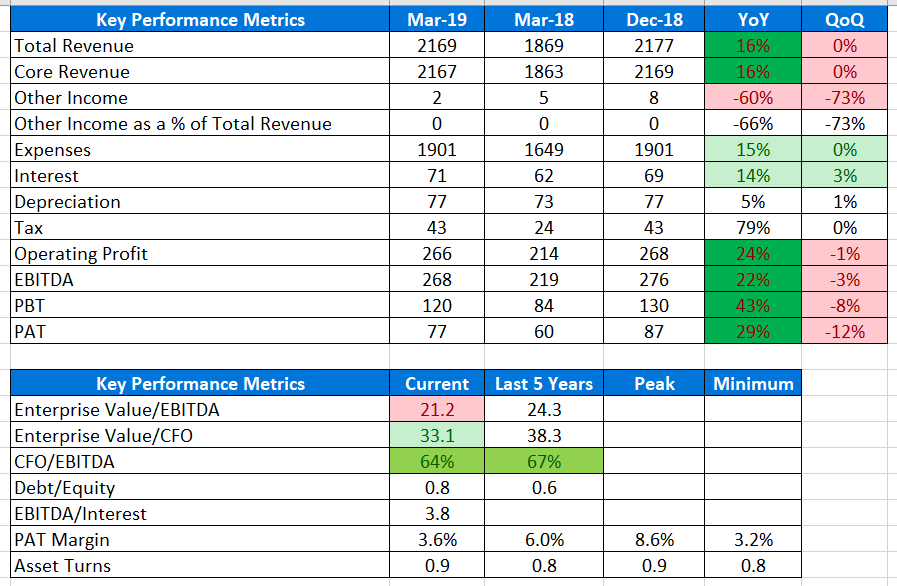

Good results due to operating leverage story, expansion growth drivers in hospital, store expansion and store operating leverage based pharmacy and reduction in losses of AHLL continues. Company posts high double digit topline and bottomline growth.

Key Takeaways from call:

- High single digit growth in matured hospital and double digit growth in new hospitals

- Navi Mumbai hospital worked at 150 bed and is EBITDA positive . Plan to take it to 200 bed this year

- Good improvement in store level profit like revenue per store, inhouse brand sales leading to overall improvement in pharmacy margins. Margin growth + 400 new stores led to ribust growth

- Fixing issues in some AHLL hospitals along with revenue growth led to better margins and reduction of losses. Trend to stop for Q1 FY20 due some annualizing expenses and then management further expects same trend to continue from Q2

- Debt has peaked out. 200 cr of promoton capx pending. Also, annually, there would be 200 cr of maintenance capex and 250 cr of working capital needs.

- Management expects to bring down debt from 3200 cr to 2500 leveraging cash generated from pharmacy sales, cash flows and some deals which they are expecting to finalize in a month

- Management also plans to bring a strategic investor for proton therapy and create a separate SPV to separate P&L and balance sheet items

- improvement in ARPOB due to improvement in case mix driven by CoEs

- Pledge has reduced by 10% from 78% to 68% and management expects to get rid of pledge in a year post loan reduction due by methods mentioned

- No major capex planned further and expect operating leverage story to continue

- Waiting for more regulatory clarity on digital pharmacy

Q4-FY19-Earnings-Update.pdf (1.3 MB)