This article does not talk about any split / bonus plan. Nor have I read about the same anywhere else.

Can you reference where you’ve come across this?

Holding from much lower levels.

This article does not talk about any split / bonus plan. Nor have I read about the same anywhere else.

Can you reference where you’ve come across this?

Holding from much lower levels.

Haven’t heard either but have been wondering if the management is looking into that and maybe I am not aware, so asked if anybody did.

Don’t you think it should be on their cards? considering the price apar is currently trading at.

PS: It has nothing to do with the article, VP doesn’t allow to post more than 3 times in a row and suggests editing.

Apar management is solid. The family runs the business well. They will make necessary decisions in time. One cannot rule anything out.

APAR will grow exponentially - everything is in their favour right now.

The business looks like that its time has come.

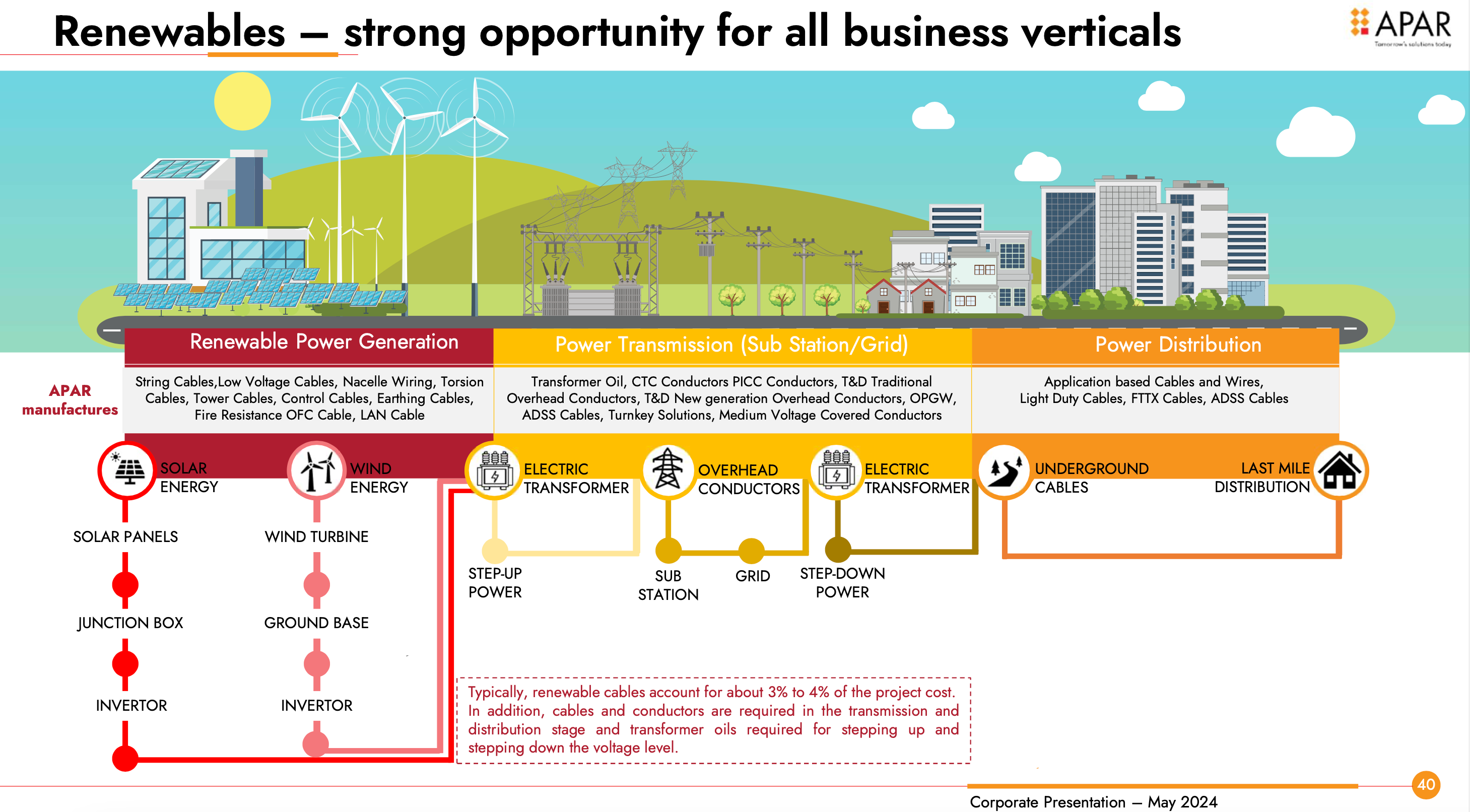

They are present across the renewable value chain.

I have one question which I couldn’t find answer to…are they exposed to undersea power cables which will be required for offshore wind and in a decade or so for regional grid connections?

Thank you all for this insightful thread. Studying this company for sometime now. Need to understand the logic of raising funds to the tune of Rs 1000 crores by diluting equity when :

In my opinion if the sole reason was to meet working capital then it could have been met through debt and it would have been better for the shareholders and if it was to get good set of investors such as mutual funds to boost the confidence of other shareholders then they could have done the same by selling some portion of promoter shareholding to these funds just like Sharda Motors did recently.

Please enlighten.

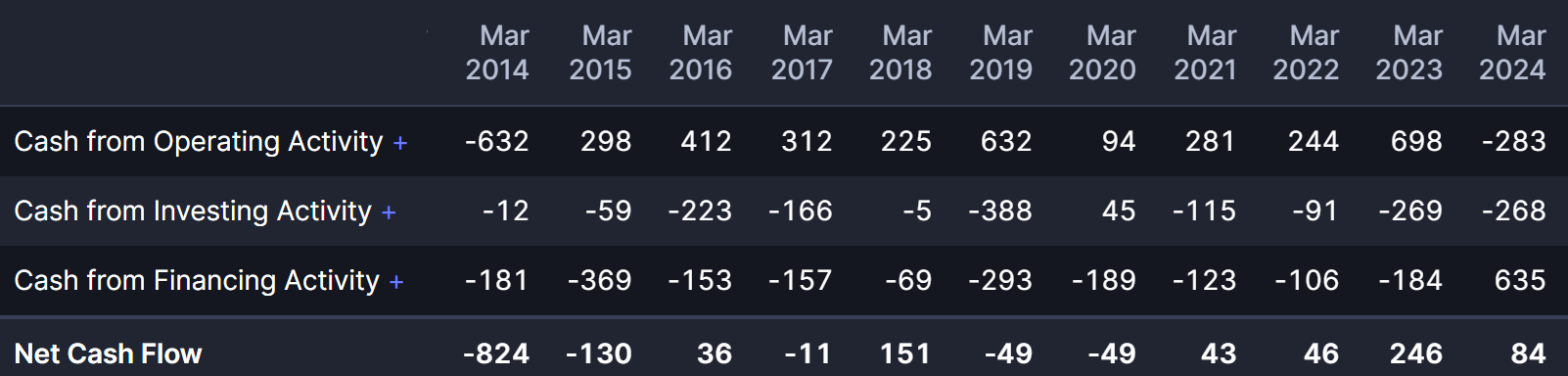

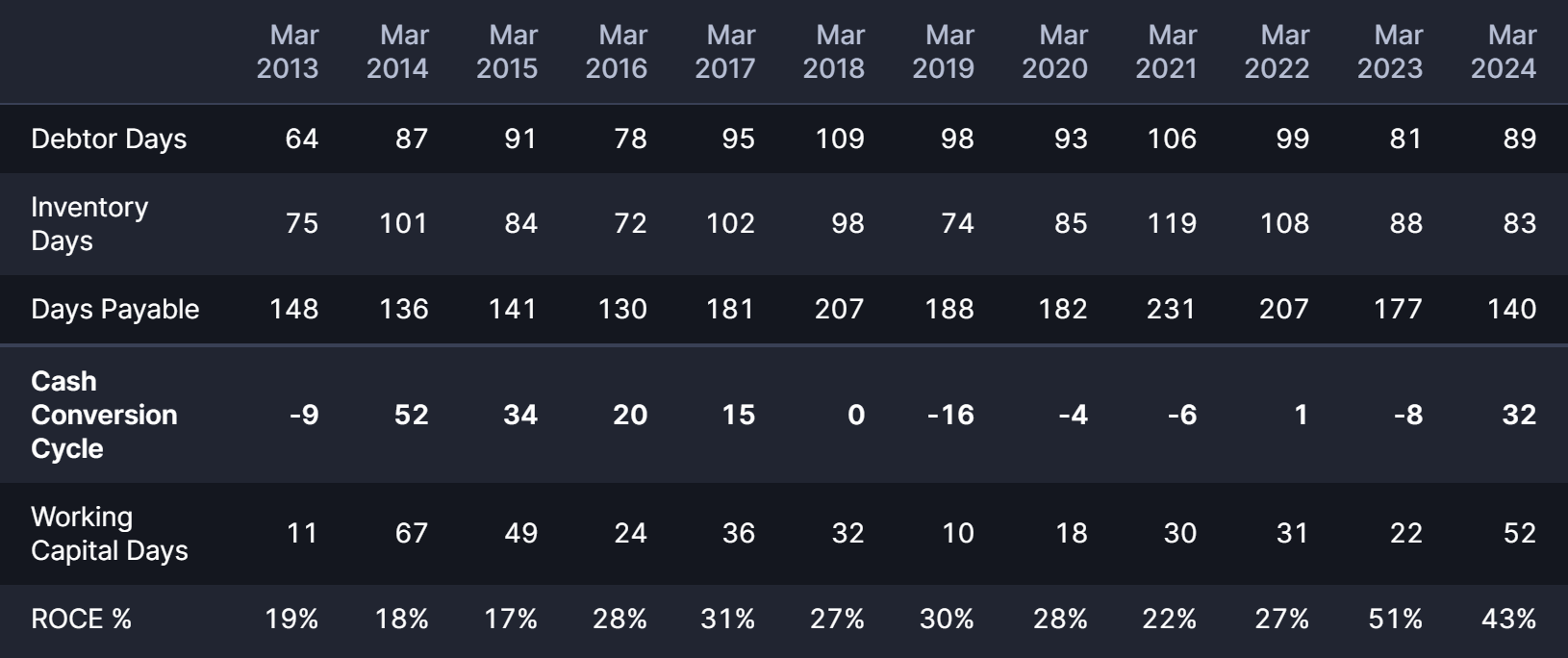

I can see day payables=140 whereas receivables at 89. However, FY24 still shows a negative operating cash flow of -283 cr at operating profit of 1556 cr. Any specific reason for this or am I misreading it?

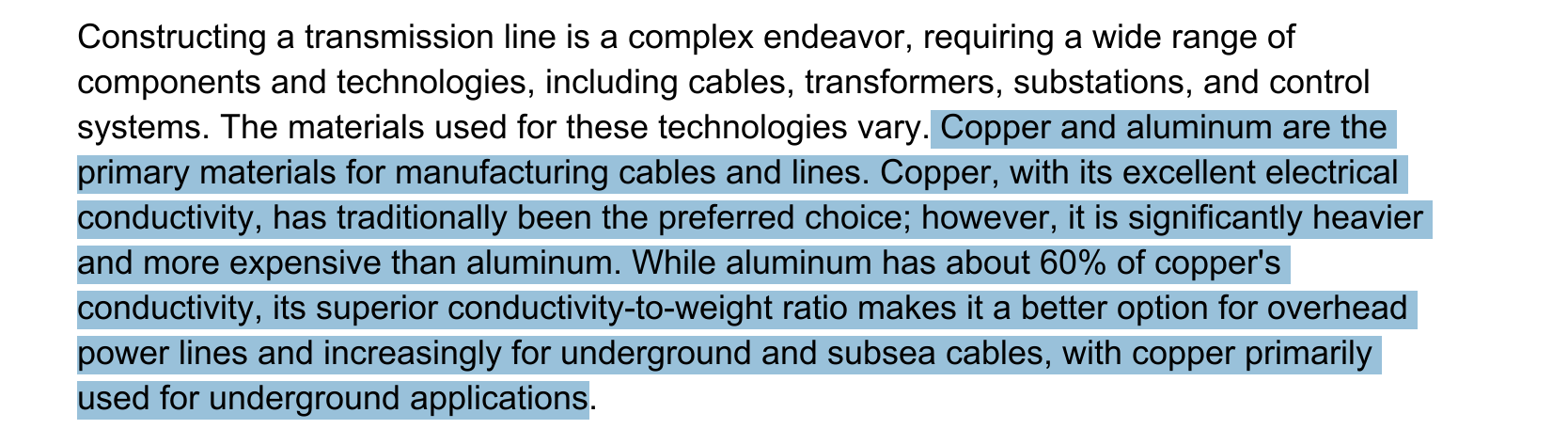

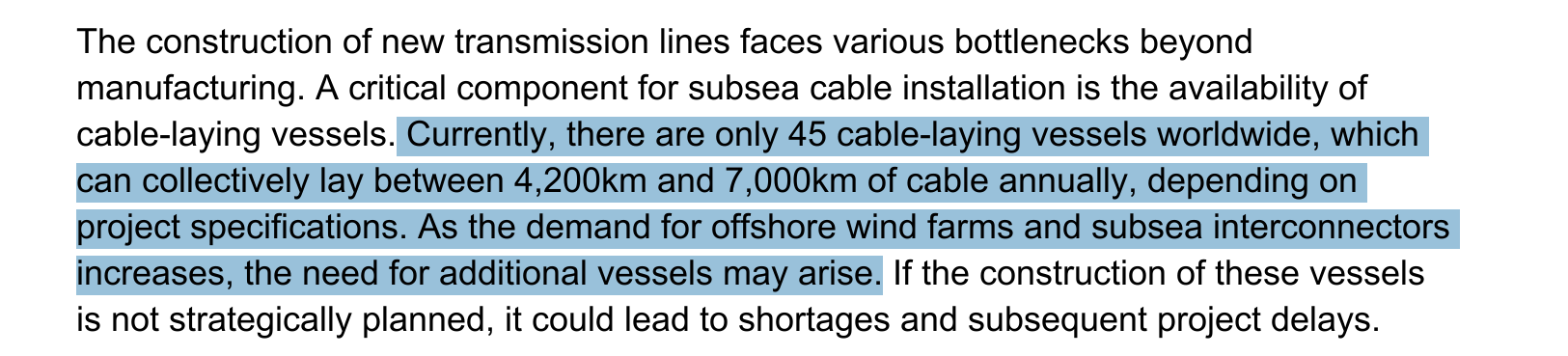

Sharing some key insights I gained related to Apar from Nomura T&D report:

Copper vs aluminium:

Shortage of cable-laying vessels:

Insulation materials:

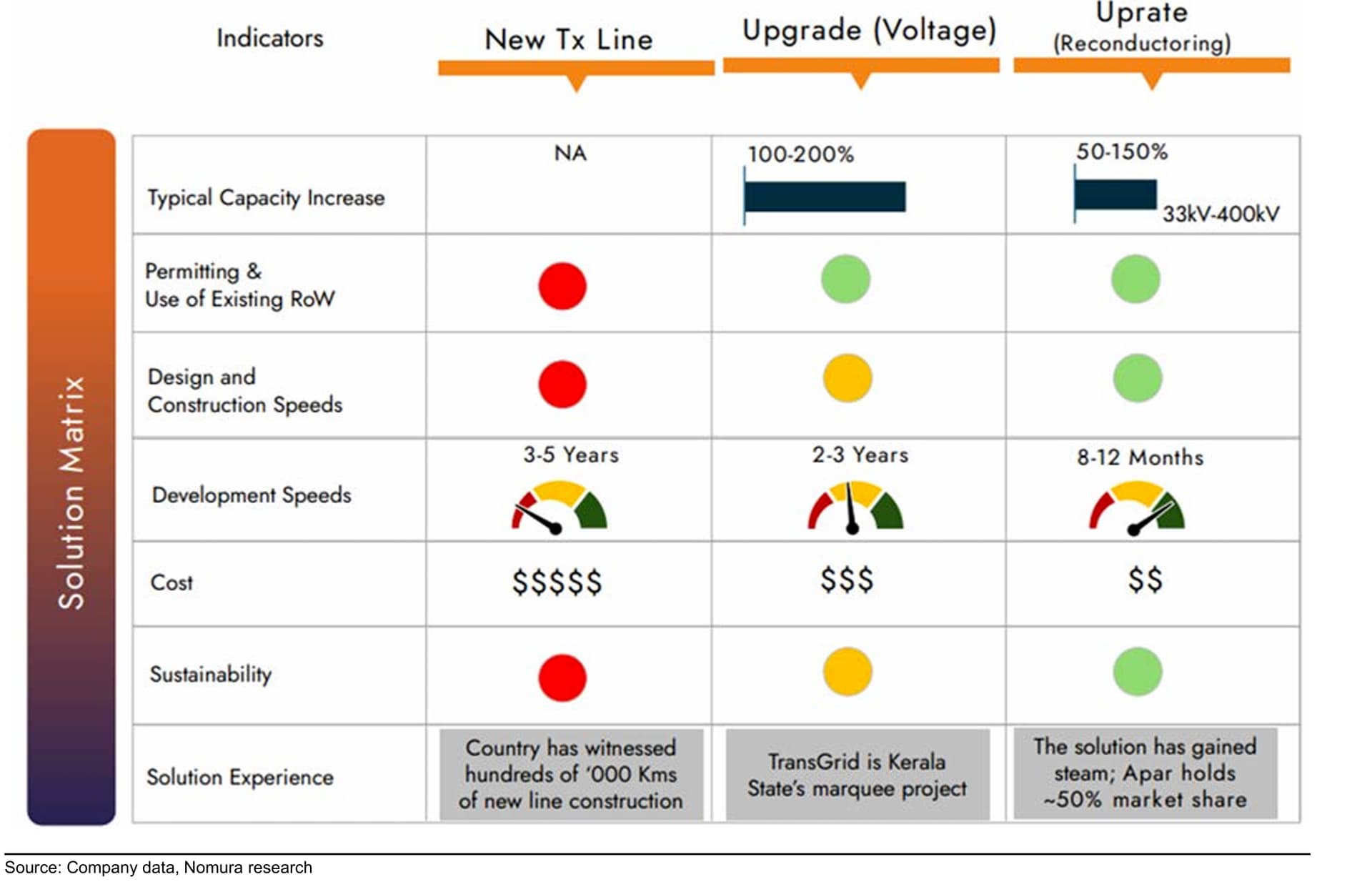

Reconductoring a significant opportunity:

Apar plans capacity expansion of CTC business

Sources:

Advanced conductors on existing transmission towers - Apar EBITDA/MT has increased from 10k in FY20 to 42k in FY24

Source: Nuvama Research Report

Apar Industries | Management Interview

Management Says "We delivered strong revenue growth this quarter, driven by innovation and customer focus.

Domestic growth remains steady with infrastructure capex support, while export headwinds are easing.

Margins dipped due to Chinese competition and lower export demand, but softening freight costs offer relief.

With a strong energy infrastructure presence, we remain committed to long-term value creation for stakeholders."

What we do in apar?

what’s is future growth ?

Apart from the poor results due to decrement in margins, the whole narrative of much less power being required by the datacentres for Deepseek compared to conventional LLM models has impacted the whole power T & D theme and hence the reaction in Stock prices… More than anything I would be tracking the margins which the management said that would improve in Q4 and FY26…Regarding this deepsake thing there is much more clarity that has to emerge and also there are chances of this not being authorized in many countries due to the China connection.

It’s not just Deepseek alone. See, the thing is, this has sent a message to the world that building LLMs isn’t as hard & expensive as everyone was thinking it was. Plus they made everything open source so that everyone can follow. That’s the interesting part.

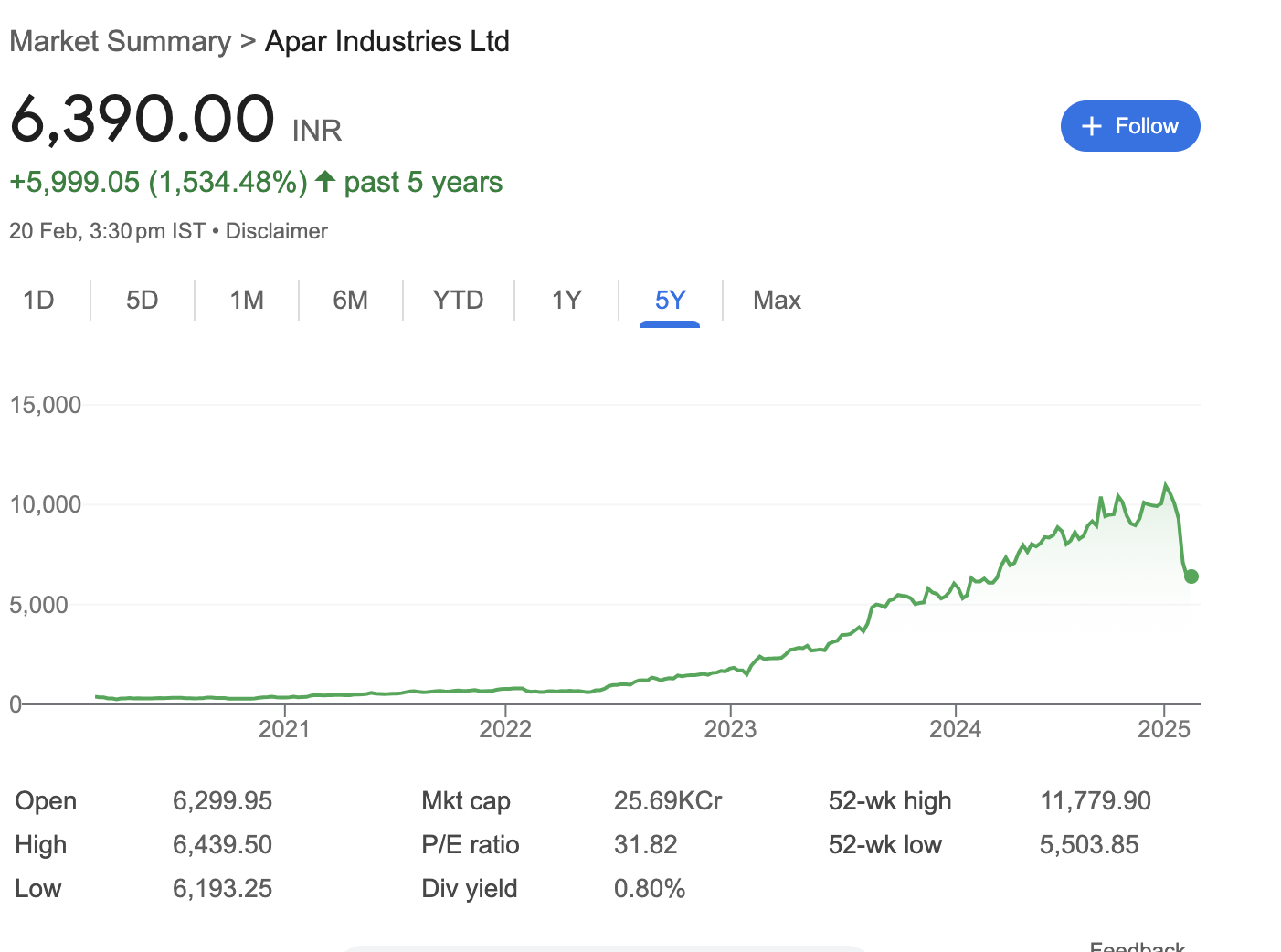

First full break in trendline, with the recent broader market correction. Still a beautiful business, with lots going for it.

Is the journey over, or can it reclaim its’ 5 digit status?

No any major issue except china competition , if they tackle Chinese competition in coming quarter you will see 5 digit shortly.

China has always been around.

This is a structural breakdown on charts. Hasn’t happened before.

Why do they have huge receivables and payables(both over 4,000 crore) as per last year balance sheet(FY24)? Is the government a big client?