This company leaves me flummoxed. All seems good, but the market doesn’t seem impressed.

If there is anyone who can shed some light on this dis-connect i would appreciate it.

Sanjay

This company leaves me flummoxed. All seems good, but the market doesn’t seem impressed.

If there is anyone who can shed some light on this dis-connect i would appreciate it.

Sanjay

Operating cash flow is very less as compared to net profits. There seems to be some operational problem within.

| Year End Mar31 (Rsmn) |

FY10 |

FY11 |

FY12 |

FY13 |

FY14 |

| Recurring PAT | 126 | 152 | 128 | 125 | 176 |

| DTL | (0) | (1) | (1) | 4 | (0) |

| Depreciation | 12 | 11 | 13 | 17 | 17 |

| WC Change | (70) | (72) | (22) | (103) | (9) |

| CFO | 67 | 90 | 118 | 42 | 184 |

Please see last 5 years cash flows from operations. PAT last 5 years 71crs and CFO = Rs50crs. Working capital did expand in FY13 but that was more of a one off which got corrected in FY14

Some statistical productwise data for members' ref....Growth sems to be led majorly by Corticosteroids and secondly by Pyrazinamide....Pyrazinamide growth must be because of WHO approval received in 2012 and it seems to have tapered off....Enthromycin, Higher Macrolides and Chloramphenicol are anti-biotic products and seem to be facing tough competition and therefore lower margins.....

Key things we need to ponder are :

(1) Sales/GB already very high at ~11 times....saturation in current capacityseems to havealready reached and expansionmightbe needed rather than debottlenecking....

(2) Imported RM proportion is at ~87 %....Even Foreign currency Expense/Earning ratio is at 1.76....

(3) If I see the product profile and business model, it seems to be closer to Calyx (not strictly since from the beginning Calyx has focussed more on pyrazinamide) which has traditionally operated at 19 % + EBITDA margins so why is the company operating at such low margins or can we assume that there is lot of scope of improvement in margins....

|

(fig. in ` cr. ) |

1HFY15 |

2HFY14 |

1HFY14 |

FY14 |

FY13 |

FY12 |

FY11 |

|

Enthromycin |

48.4 |

50.9 |

47.9 |

98.8 |

100.3 |

98.5 |

83.6 |

|

Higher Macrolides |

32.7 |

36.7 |

33.6 |

70.3 |

62.3 |

81.0 |

58.1 |

|

Chloramphenicol |

7.3 |

2.9 |

5.6 |

8.5 |

11.8 |

9.1 |

5.6 |

|

Pyrazinamide |

14.8 |

15.8 |

13.3 |

29.1 |

27.2 |

13.6 |

7.4 |

|

Corticosteroid |

33.3 |

30.85 |

17.25 |

48.1 |

28.2 |

17.1 |

16.7 |

|

Others |

9.2 |

4.35 |

5.25 |

9.6 |

11.9 |

5.4 |

4.1 |

|

145.7 |

141.5 |

122.9 |

264.4 |

241.6 |

224.6 |

175.5 |

Discl. - Invested

Hi Mahesh,

Have a strong feeling that this guys are trading in higher macrolides and steriods (that isi why higher sales/GB ratio and low margin) For higher macrolides like clarithromycin and azithromycin, no body can beat China in cost. Even basic steriods range, China is cheaper.

Anuh has the advantage of no debt/cash reserve which they are putting into best use by bargaining best price while buying and this is reflected in better margin.

Disc: Not invested

No Ramesh…they are not a trading company as is evident from their accounts as also till the actual data of production was available…Macrolides is a very crowded place and therefore low margin is understandable…however, since the contribution from low margin antibiotic space has declined over FY11-FY14 from 80 % to 66 % whereas contribution from high margin products likes coticosteroids has increased from9 %to18 % – at the same time if I look at pure EBITDA margin (w/o exchange gain/loss and w/o OI) then it has gone up from only 9.09 % to 10.04 % over the same period…part of this could be because of majority of its sale being to unregulated markets where competition is intense while margins are low…Also, if I look at its clientle then its comforting with the likes of Cipla, Alembic, Ipca, Lupin, etc…so its a contradicting situation but nil debt and Cash&CE of 42 cr. is soothing…I think there aresome questions we need to ponder — will co’s focus on R&D since 2012 do any good — will it be able to increase its sales from regulated markets ---- if it can do both then will it translate into higher margins…Q3 results will be interesting to watch…

Rgds.

Discl. - Invested

This post is in no waya buy/sell/hold recommendation but is part of a general discussion on presented statistical data and facts.

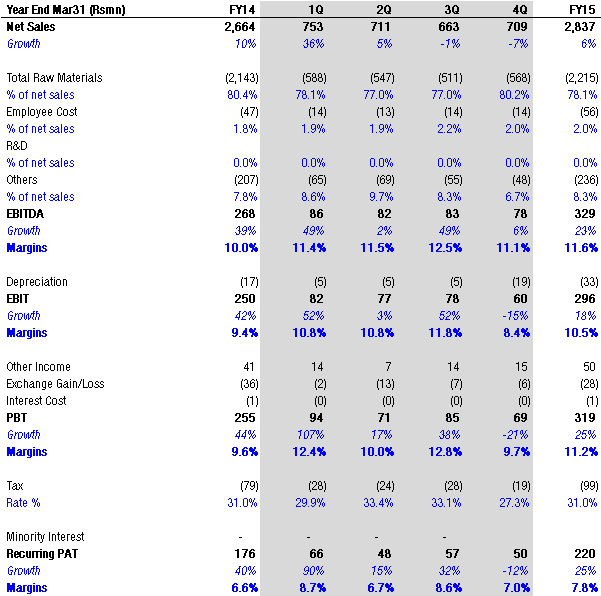

Anuh Pharma delivers a decent quarter. Despite 1% YoY decline in sales EBITDA up 49% YoY and PAT up 32% YoY. 9MFY15 PAT at Rs170mn up 43% YoY. All set to deliver Rs27+ of EPS in FY15E and trading at 15.2x FY15E with 20%+ RoE 35%+ pre tax RoCE, zero debt and dividend payout of 35-40%.

Still a pocket of value in this expensive market

Disclosure: Invested

Anuh Pharma management interview on money control. Talks about future growth potential and launch of new products.

Yes company management has guided for 25% sales growth in FY16E. But stock is not cheap anymore so one needs to be careful.

Disclosure: Invested from lower levels and continue to hold on.

Weak 4QFY15 on Friday has led to a stock correction today by 7%. Any views on this. Does management still stick by 25% growth guidance for FY16E?

I made my first buy today, making use of the correction. Only time will tell whether I am catching a falling knife. What caught my eye was - there is 35% spare capacity available in existing plant, no USFDA exposure (I like this - small/midcap pharma cos can’t put up with the vagaries of FDA specific requirements and can hardly invest in the kind of process, stringent enough to satisfy FDA. That said, there is a move towards making the new Tarapore plant for the regulated markets. That will happen in FY17. In the immediate future, I am looking forward a standard 20% growth (although, last 2 years have been flat), based on upcoming launches in API. I have my expectations grounded and this is certainly not cheap - for the kind of co, this is. I have modest expectations and I may have to down average a bit (although not a preferred method). There is no need for capex and there is a decent amount of cash with the firm and that will also add to the x factor

PS - This is not a recommendation and please do your due diligence before acting. Standard disclosure clauses apply

What just happened here today. 20 percent upper circuit??? Yes they are having a board meeting to issue bonus shares. But that means nothing. Does anyone know something

yes tomorrow board meeting for bonus issue in Anuh Pharma, management has given an estimate of 800cr + topline and 100cr+ bottomline over the next 5 years in their recent interview. Management has good expansion plans. I have taken a small position today for the long term.

disc: invested and may add on dips

I liked the fact that they are debt free , also are planning to enter US markets FY16, they have presence in 57 countries,also expansion is without ipo/debt…pl note: not a recommendation

This stock is on steroids. Another great pick identified early by Hitbhai. Almost a 10 bagger if someone had invested in it at that time

Looks like a reclassification of some of the individuals to promoter category has resulted in the increase in promoters shareholding.

Hey guys,

These are my notes from the Anuh Pharma AGM:-

*There are 20 products in the pipeline. The pipeline will keep developing.

*Corticosteroids are high margin and company will grow from it.

*Will also look into formulations in the future.

*May give 1:1 bonus in the future.

*Company entering regulated markets this year via off patent products.

*Margins are north of 20% in regulated markets.

*Risk to regulated markets is that volume is lower than non regulated market. Hence, company will maintain healthy balance between the two markets and keep itself diversified.

*Reiterate guidance for 90-110cr PAT within 5 years.

*Expansion work is underway.

*Company will grow from internal accruals only. There will be no reliance on debt or equity issuance.

*Company is poised for strong growth in all segments and products.

My takeaways:- Mr.Bipin Shah is extremely clever and shrewd. He had all the answers at the tip of his tongue. He was precise. Inspired confidence. Not flashy at all, very down to earth. The kind of promoter I like to back.

Disclosure- These are just my notes. Although I do not think there are any mistakes in these, please do your own research before making investment decisions. I am invested in Anuh Pharma.

Warm regards

Neil

Anuh Pharma is predominantly an API player, which have usually lower margins than Finished Dosages, or Branded Generics. Hence API players are usually available at a discount to Generics player. Even if one accept wholeheartedly 25% guidance, and 100cr odd PAT in 5yrs, still Anuh Pharma looks extremely expensive at 36 odd trailing pe.

I see no reason why shouldn’t one prefer Granules, which is available at a cheaper valuation, is expected grow faster in next 2 year, and is undergoing API to FD transition nicely. At 40 odd pe, why shouldn’t one prefer Shilpa, which is into high value onco-API (whose growth will be muted in fy16e, but should start firing from fy17e due to multiple triggers).

So far I havent been successful in understanding why should anuh quote at such crazy valuation. Seems to me bull market euphoria to me.