i don’t think so that any actual cash movement happened, its probably just accounting stuff or maybe maturity of advances which now qualifies as loans

1 Like

7efc9638-c5cd-4ea0-ab18-809db365eede.pdf (233.0 KB)

Any thoughts on this ? Ideally they should give atleast a new dumping area?

1 Like

well the bmc do have proposed a waste to energy ground at deonar,lets see how that goes plus mumbai already has multiple dumping grounds, optimizing them to the whole would be a challenge as they do have to work on increasing their efficiency.

4 Likes

so this is my imp takeaways in a very rough format and mota mota updates about the company Q4 FY25, please forgive for mistakes and just take it as a rough note, i have not added any quantitative (i.e growth yoy and stuff) snippets as you can find them easily in invetsor presentation

Q4 FY25 CONCALL

1) Demonstrated scalibility of the oprations

2) Favorable settle ment and the fund has been credited to our account

3) Remeaining amts in ongoing arbritation would be resolved in our favour this is what we believe

4) Md says solid growth of 14% lol for q4 fy25

5) Healthy 10% up from fy24

6) Heigher volumes and increase in operation

7) 48% yoy growth processing entity.

8) In q4 fy25 we started an new contractin navi mumbai C&T CONTRACT,

9) PBT was down a bit on yoy basis ,they stated ths primirarly because of depriciation and interest cost,following the commisioning of wte and c&t projects.

10) Escalation which are part of the buisnesss has been slightly sticky in the last few periods

11) They feel it can be made up with approvals in time

12) They expect healthy grwoth next fiscal year with an order book of 8300crore

13) QUES 1

We have already submitted 2 in south and 1 in western part of coutnry and 2 are in line when it comes to bidding for new projects

The buisness carriews great license risk as it depends upon govt top give contracts

Waste to steel project in talk in talk with a big corporation, we wanted to buy land for project and identified a piece of land for car scrappping and rubber scraps would be updated next quarter

- QUES2

How many long due cases are pending ? 2, one with supreme court around 19 cr and one from clients collectively around again 19 cr

Both are pre 2016 after that contracts are more efficient

15) QUES3

Breakup of 8300cr= close to 58% of it having a long tail which is expiring by 2040

The balance would be executed over 12 years

Cannot show a linear growth of 15-20% due to nature of business they may havea revenue jump up due to bagging of a cntrqact as this industry does not work like other wheer small company mens aggresve growth

Tough industry

Constructionand developemnt contract revenue 5

Do they see company making topline of around 2k cr in 5years?= it would be very ambitious so that as of today

16) QUES4

Any plans to reduce debt to decrese interest cost?

The debt is mostly collateral and stuff they are trying to pay back debt

What would be the amount that they would receive if court cancelled contract?

They have no alternate site for waste and the comp has approached big 4 for valuation of collateral they should get

Vehivcle scrapping?

Timeline is expected to close deasl and stuff and commence from fy27

17) QUES5

We have to look on cagr basis mota mota nt on yoy basis

18) Why are we not winning more C&T projects?

They are doing okok in terms of securing contracts and they are going after good cities where they have ability to pay and good track record of paying the companies

19) Adjusted the numbers that we had a runoff so they have adjusted the numbers from existing projects and stuff

We normally see a volume growth of 3-5% C&T,escelation and volume growth at max 8-11%.

Bulk of capex has been done post monsoon maybe additional 2 quarters of capex do not expect more capex in ourr existing contracts

The core ebitda margin will move to 20-23%.

Please do cross verify as i can be wrong and do correct me,thank you

4 Likes

Hi all! just had a few questions regarding Antony waste - still learning about the business and would appreaciate any help!

- do we know what the total revenue exposure to the facility in Mumbai is?

- would it be safe to assume the margins on this businesss are above group average?

- has the company spoken about what is their maintainence capex level (ex- any expansionary needs)?

thanks !

3 Likes

yo, so let me tell you the company is heavily concentrated when it comes to that,and mumbai metropolitan region conbtributes to approx 45% of their revenue,but exact numbers can change a bit here and there due to project time line ,but they are concentrated.

secondly yes a bit but not much high margin if you look closely at bio minning and processing part

so about that maintance capex part, it will be under 3% of revenues most of the time,until the timeframe for that asset is over and new has to be brought in for replacemnt, the company has not mentioned this specifically, they have always mentioned about expansion capex only. hope it helped

4 Likes

thank you that is super helpful!

so it remains quite a large chunk of revenues - do I understand right that the risk here is in some way ring fenced by the fact that the contract includes clauses for compensation of revenues in case of the SC ruling not going in their favour? maintainence capex levels look fair I think - though for a 20% cagr to sustainable mid term I doubt we see that level..

thanks again!

3 Likes

yes, as we know we are into a B2G business and in any B2G business most of the time government always has the upper hand, the company has previously seen delayed payments and court hearings just to get their payment. right now if you go through the latest concall they still have some unpaid amount. to solve that company has improved the contract type mostly by putting in good terms and agrements with most prob no loopholes which govt party can exploit. and about cancellation of contract, recently there was a talk of landfill area to be removed as it was stated that the landfill was some conservative site for specific type of tree, but company made sure that if the order to get removed gets passed they will get all the invested amount back, but again its on govt mercy so you have to look at it that way.

about the capex part they invest only when they get contract or get contract confirmation, so any info you get about company doing capex(mostly) it only happens when company already has that order. so mostly any additional capex we see it is most probably due to new contract. so the most important part for them to grow at 20% is to continiously bag new contract and overall budget allocated for this sector for govt should increase so they can focus on this part, as my personal opinion is they should really focus on cleaning the city and managing dumps well because your average indian city really need some good waste managemnt.

the biggest threat in this business is the payement system,even if the industry grows at 30% if cash is not recived and recievables are piling up causing cash munching which can lead to more borrowings and poor valuations.

10 Likes

If possible , study urban enviro waste management and add your insights on its forum , it will be very helpful

6 Likes

Antony waste has got a temporary relief from supreme court which has stayed the decision of high court that would have turned Kanjurmarg landfill into a protected forest again and as we all know that it handles 90% of mumbai’s waste so for now we can say a major disruption is halted.

but if u read the document it also says that the final verdict is still pending if they go on to agree with high court decision then it could be serious problem for the company. either they get compensation or alternate land.

now apart from what the press release i think its stupidity to say in overnight that now this site cannot handle 90% of the city’s waste and it runs 24/7 and they need to already pal an alternative befroe they go on to impose sucha crazy decision for such a big and important city i think supreme court decision is good ,if u want to protect the forest its good do that but at least give people a new place to dump waste before

8 Likes

@Rohan_Selson what is their total order book now?

2 Likes

It should be around 11,500 crore now.

8 Likes

but any idea why the stock has not responded positively?

1 Like

mostly randomness and need actual numbers to reflect into results and cashflow to actually move the stock

It seems that the Kamjurmarg project case is an issue.

Have attached a note which should be treated for purely educational purposes and it does not solicit or recommend any level for investments.

Antony Waste Research (Educational).pdf (691.6 KB)

4 Likes

Decent Q2 results.

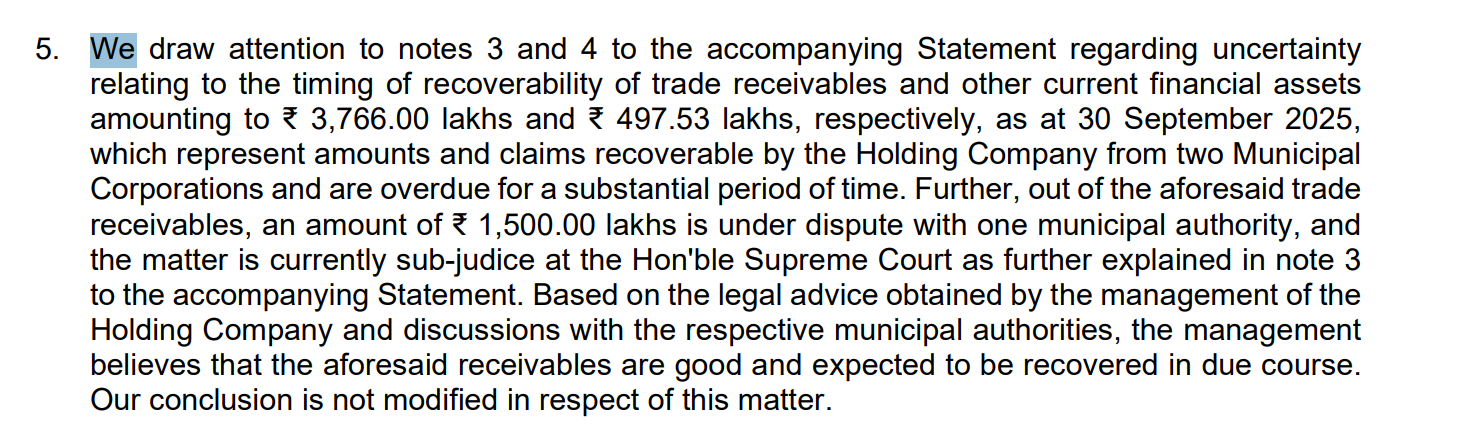

Auditor warning for 42 Cr. worth of past receivables, 15 Cr under dispute in Supreme Court.

Company’s diversification into WTE remains the highlight and receivables remain the pain point. Q2 concall breakdown

7 Likes

https://www.business-standard.com/amp/markets/capital-market-news/awhcl-arm-secures-two-contracts-worth-rs-1-330-cr-from-bmc-125121701074_1.html

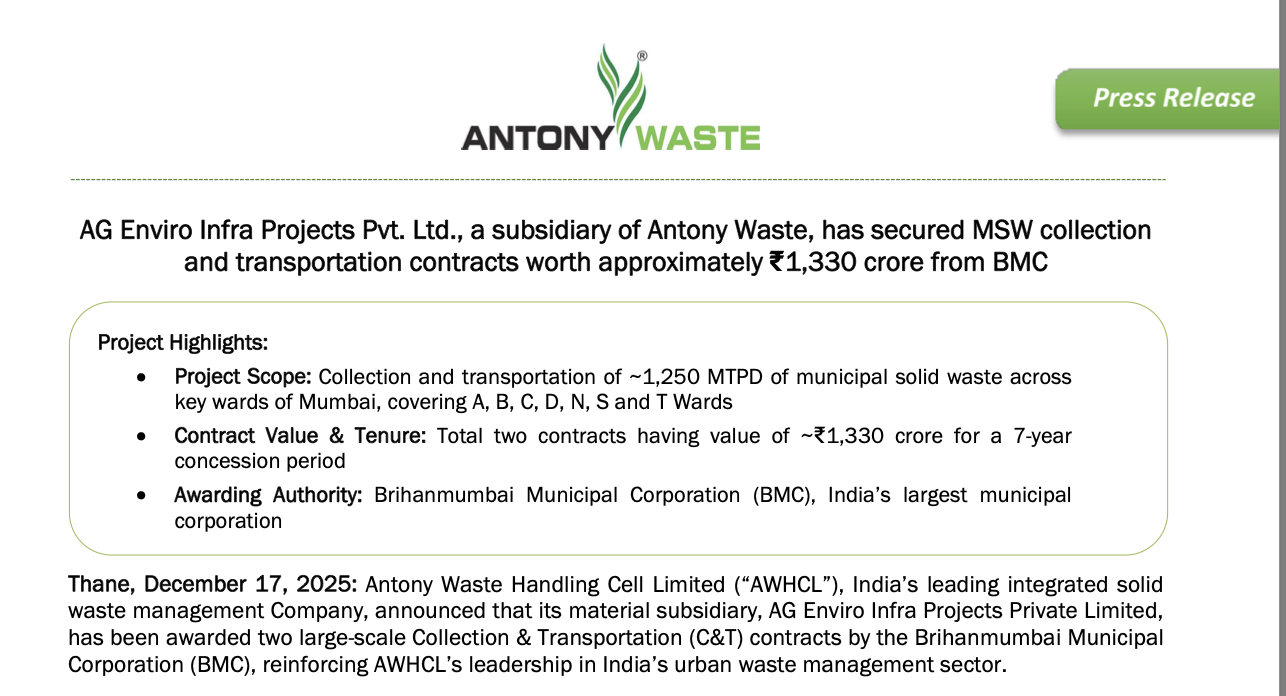

Antony Waste Handling Cell announced that one of its subsidiary, AG Enviro Infra Projects has been awarded two contracts of Collection & Transportation of MSW in the city of Mumbai by Brihanmumbai Municipal Corporation. The contracts were awarded to consortium/Joint Venture of AG Enviro Infra Projects (51%), M/s. Jigar Transport Company (29%) & M/s. M. K. Enterprises (20%).

The first contract valued at Rs 684 crore for a period of 7 years entails, collection & transportation of approximately 650 M.T. Per Day from A, B, C & D Wards of Mumbai City. The second contract valued at Rs 646 crore for a period of 7 years is for collection & transportation of approximately 600 M. T. Per Day from N, S & T Wards of Mumbai City.

1 Like

AWHCL announced that its subsidiary, Antony Lara Enviro Solutions Private Limited, has

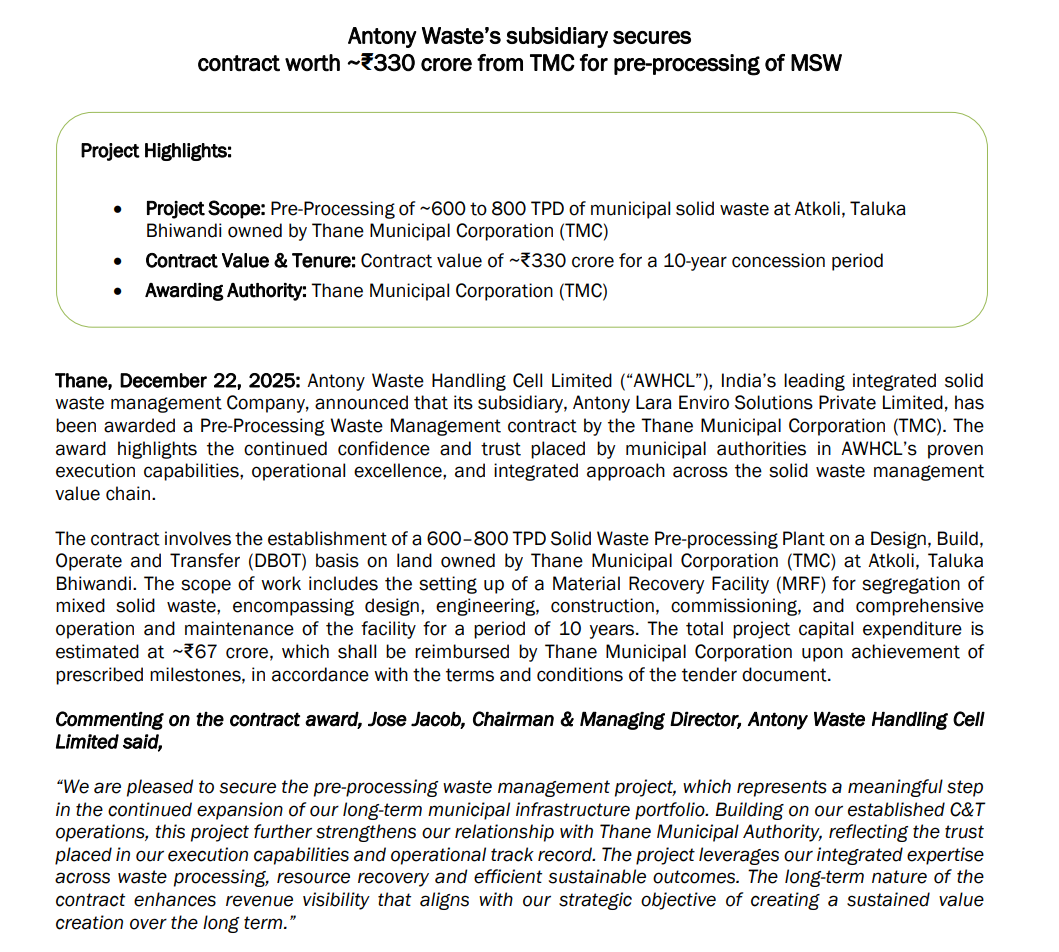

been awarded a Pre-Processing Waste Management contract by the Thane Municipal Corporation (TMC).

The project is on DBOT basis and total project capital expenditure is ~₹67 crore, which shall be reimbursed by TMC.

Project Scope: Pre-Processing of ~600 to 800 TPD of municipal solid waste at Atkoli, Taluka

Bhiwandi owned by Thane Municipal Corporation (TMC)

Contract Value & Tenure: Contract value of ~₹330 crore for a 10-year concession period

2 Likes