Ok so a lot has happened since my last post! I’ve been actively building portfolio during Covid crash and was able to add / average many positions with decent buy price. Of course, in hindisght, should have invested more during March-June. ![]()

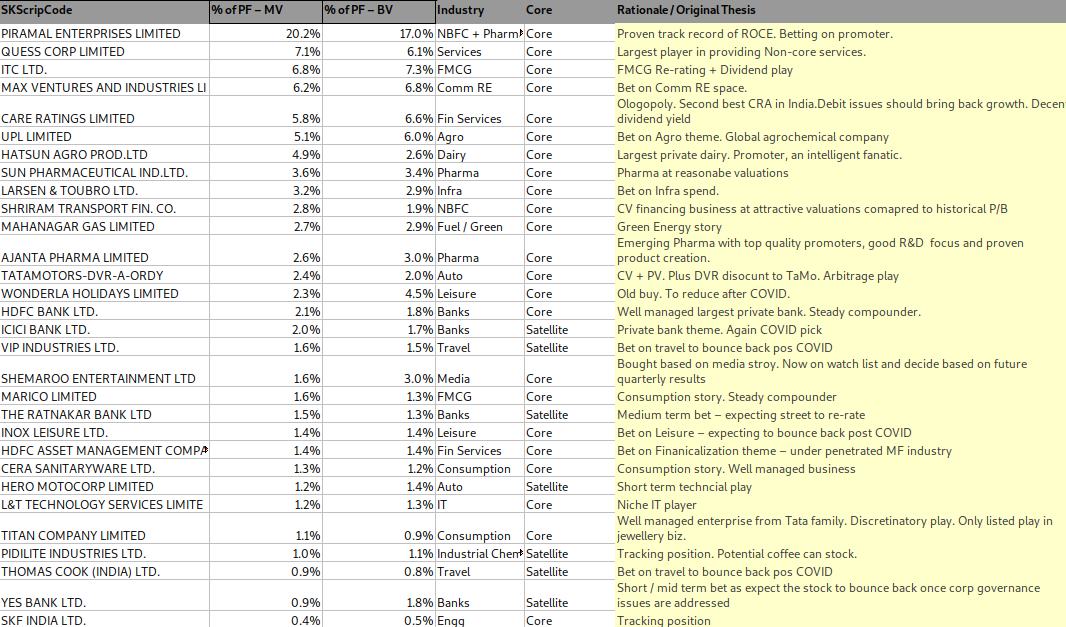

Please find below the latest portfolio, broadly categorised into Core and Satellite.

I’m aware that it is perhaps too many per liing of most investors but I do have lot of time to track (kill)! ![]() Plus, some of the companies have been holding for past few yeears / big names that perhaps needs lesser attention.

Plus, some of the companies have been holding for past few yeears / big names that perhaps needs lesser attention.

Feedback most welcome ![]()