Mostly outdated articles around EVs future. Flex fuel - different sources of powering the vehicle should exist. CNG came into being but has not been able to impact a lot. So tech is ever changing.

Hydrogen fuel is upcoming and should find a lot of space. Given the underlying elements or starting elements are mostly commodities and are more or less unevenly spread. So may be europe and its stakeholders find oppurtunities in Hydrogen but Amara seems confident that they can pivot and are not looking to be the first one to get slaughtered. Being the 2nd one is also fine as TAM would be good for every one.

The sense one gets from listening to Amara Raja Management is that they are well aware of the margin, ROE and changing tech landscape challenges in the Li-ion cells segment. However, they have made a modular plan for venturing into the business because lead acid will get replaced incrementally by newer batteries in one form or the other over the next few decades and if they don’t act now, the terminal value of the business will keep declining. However, they are quite cautious about their approach, first setting up a customer qualification plant, then a 2GwH line for 2Ws and then expanding to 7-8 GwH once this stabilizes. They face a difficult, uncertain situation wrt the future of Li-ion technology and viability but I like the way this management is going about it. They aren’t going all in but at the same time they are not failing to act.

Having said that, the economics of Li-ion business are definitely nowhere close to their existing business. But hopefully what they will lose in valuations due to lower ROEs, a part of it will get made up via higher terminal valuations. Also, with the 2 sons involved heavily and the promoter apparently giving up politics to focus on the business, investors can hope they will try will try their best to steer the ship as best as it can be steered in such choppy waters. Over the medium and long term, I would trust Amara Raja to execute better than its Indian peers in this area. I may be biased.

Hyundai Motor Company and group firm Kia Corporation have signed a Memorandum of Understanding (MOU) with Exide Energy Solutions Ltd, as part of their electric vehicle (EV) expansion plans, Hyundai Motor Group said in a statement.

Hyundai Motor and Kia aim to localise their EV battery production, specifically focusing on lithium-iron-phosphate (LFP) cells in line with the expansion of their EV plans for the Indian market, it added.

Its surprising how wide the PE re rating between Exide and Amara Raja now. Almost 2X!

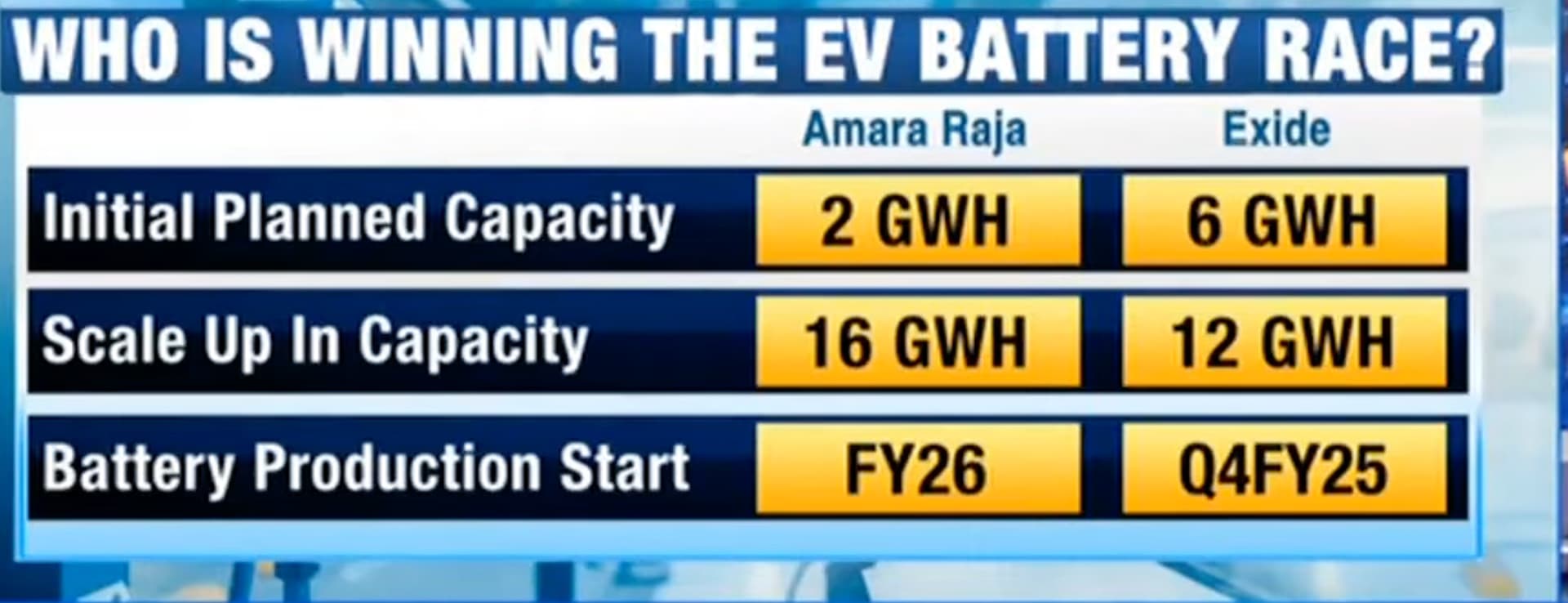

Its becoming hard to really understand whether these companies expect a high revenue jump from FY26 when LI facility starts? I see Tata Motors and major OEMs implement a tighter control over their Battery production since simply that will be pne of thier biggest spends in EV production.

How do you all see the LI Battery production and would it really bring in a game changing revenues, like 30-40-50% jump when thise giga factories starts in FY26?

Proof will come when EV targets by countries or states are met. And that should act as a POC (proof of concept) for other battery makers or other OEMs or even standalone Battery makers (who don’t garner eye balls coz of their legacy Lead Acid Battery journey)

Imo tesla coming to india is a proof of concept, battery infrastructure is on the rise and policy do hint at a up trend vs a down trend. Tesla is a EV car maker, so focus increases on developing and providing a infra for Tesla and in general car makers to flourish. Battery players are likely to benefit on several front and not just EV. Lead acid still remains a part of the ICE car and may be they still remain a preferred stakeholder for telecom operators. Not counting Data centers as that is a given. Amara raja has a good share in telecom domain which helps the legacy business for sure when they shift to li ion.

Negatives are less in number and +ves can come in which could re rate and clear out the arbitrage b/w exide and amara raja.

Plus the overhang of Amara raja promoter and their political alignment seems to be fizzling out. Double +ve imo in a country like india.

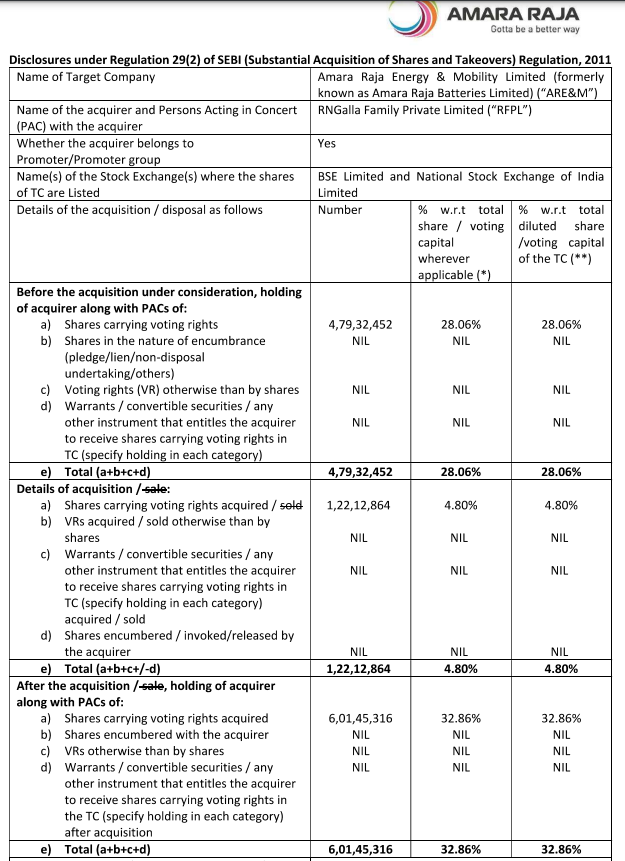

Personally for me, low promoter holding of Amara Raja is the deal breaker. With promoter holding only 28.06% stake, I really need to have huge confidence in the promoter integrity and honesty before putting my money on the block, which is not the case here. Also history shows that any new technological change may bring in new market leaders in that sector. So betting on old war horse to adopt and adapt in dynamic changing environment also needs to huge leap of faith on management and promoters.

Low promoter holding shouldn’t be as much concern as promoter selling the stakes. Amara promoter family hasn’t reduced their stake over the years and has maintained it at 28% which again is not small by any means.

Some of the blue chip names like Infy, L&T, Axis, Mahindra & Mahindra also have low promoter holding (under 20%) which doesn’t mean their management is inept or questionable. And there are other quality names (e.g. ICICI bank) where there really are no promoters.

Conversely most of the PSUs and inferior small caps companies can have very high promoter holdings which doesn’t make them particularly well-run or high quality investment.

It’s testimony to promoters’ vision and execution excellence that Amara was able to break Exide’s monopoly and gain significant market share. Quality of their product is world class (from my own experience), it’s a zero debt company and promoters are very smart in allocating capital.

The increase is not because they bought it from open market but because they merged one of their companies with AREM and that increased their shares in AREM.

It’s an interesting point considering that both Exide and Amara have traded at the same multiples historically. Amara has just closed gap with its 10 years average multiple.

Considering duopoly structure of the market and not much difference on the other parameters between the two companies (quality and ambition of management, technology, execution ability, capital access etc), Amara should also trade at similar multiple to Exide. That means stock could hit 1500 in the near term.

I don’t think Political play has much do in this case, unlike Heritage Foods. Exide and Amara Raja are both in rally because of their play in EVs. Also they’ve both broken consolidation of many years.

")