Below I have written my insights about All E Technologies Limited

I am invested in the company from lower levels and have decent position in it.

Do share your views on it… So that we can build up a nice conversations around the company and the business All E Technologies Research Report.pdf (4.5 MB)

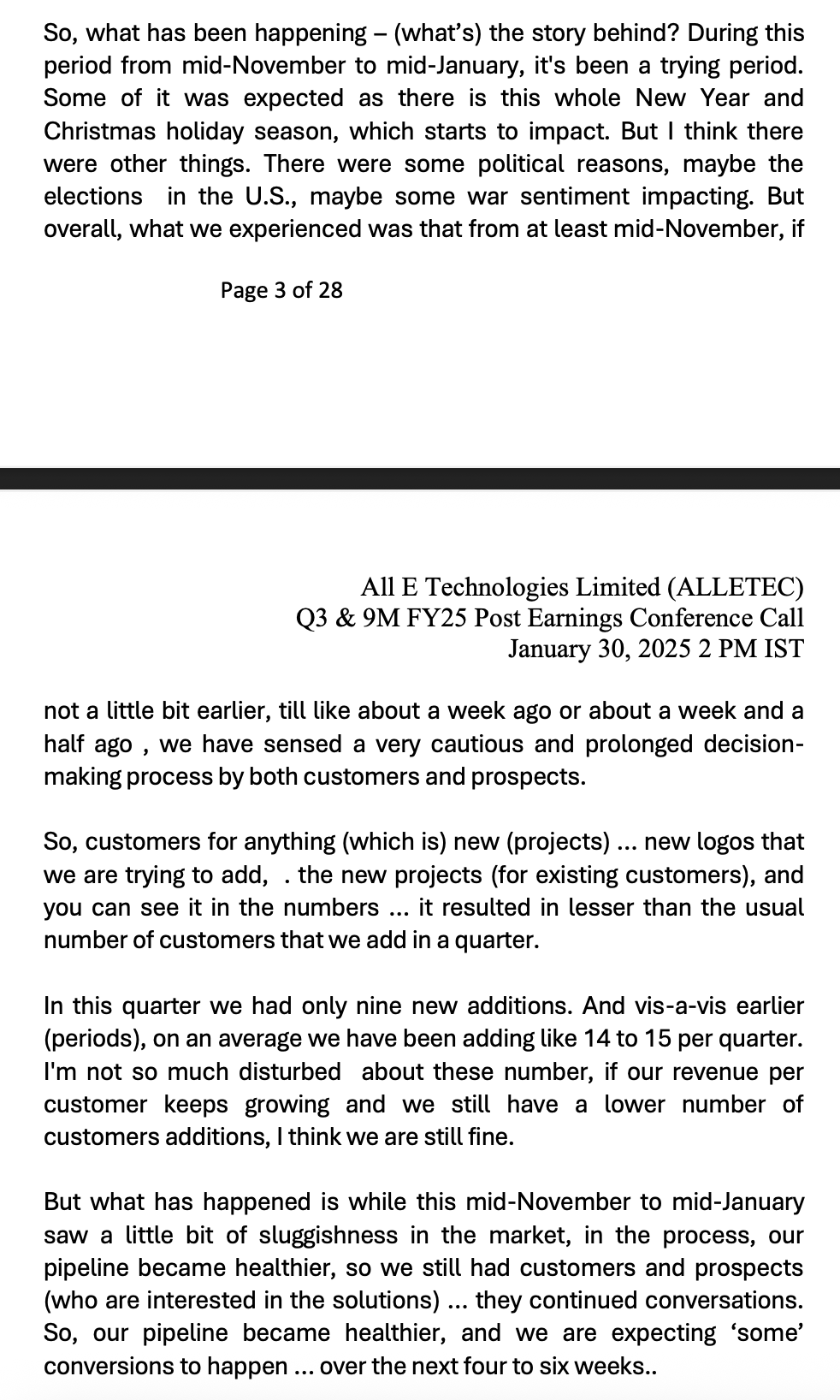

I heard their concall for the 1st time today. Honestly not impressed. Few observations:

Touch of arrogance

Indirect response to few direct questions (such as what are the sales channel for international mkts, blended billing rate, products vs svcs revenue mix).

With ~1000 clients for a approx annual svcs revenue base of ~75 cr gives a sense that they are one among crowd serving their customers (& not really niche/ strategic), hence easily replaceable.

On a like-to like-basis, avg annual svcs realization per employee is ~20 lakhs, which again looks low (hence does not give a sense of any niche kind of work).

They have grown from 0-100 cr in 24 yrs. For growing 10x in next 10 yrs, could not get a sense of any strategy/ plan to achieve it. what is new that will help them deliver such a performance in future.

Video on HR that CEO showed is basic chatbot that any IT company would have even without Gen AI. What’s so unique about All-e-tech here was missing.

Product margin seems to be 16-19%. usually industry operates at ~10% margin. Hence as they will grow, this component may deflate the overall margins.

May be reading too much for a microcap but not convinced about the company somehow…

Their work is not niche (Most IT services is commodity anyway). RPA and chat bot that they showed on the call - people have done these things ages ago.

I feel their products are not really products, but solution accelerators. But good to see a company of this size having them and thinking of industry solutions rather than plain staff augmentation.

To one of the questions, CEO said their revenue is not linear with headcount. My view is that the margin expansion is the result of more work from US, rather than a differentiated model.

They are riding on the demand for service opportunities for Microsoft suite implementation. CEO mentioned services/implementation opportunity being 5-7x of license revenue. I worked in a large consulting provider in their Salesforce practice - they used similar number for calculating TAM.

The market for Microsoft suite implementation is huge. Accenture had a dedicated subsidiary for Microsoft implementation called Avanade. If you google you will see that Avanade revenue is $3 Billion +.

The reason I feel All E Tech will grow at reasonable pace till demand for Microsoft suite sustains, is as follows -

The clients they target are small and not serviced by biggies.

Big dampener for large IT services right now are the GCCs (captives) that clients are setting up in India. The kind of clients that All E Tech would be keen to get the work done by third parties rather than setting up their captives.

Since they are 100% Microsoft shop, Microsoft will push some work to them. CEO alluded to this in the call. I am aware this is a practice followed in the industry, based on my experience in Salesforce landscape.

I like that they publish quarterly results (as SME, they don’t need to) and hold con calls. I like the conservative nature of CEO. I also like that their top management has stayed together for nearly 20 years.

Need to closely monitor how they manage employee cost as they grow. After the madness during COVID years, last couple of years have been benign for talent cost escalation. If situation changes, small companies will find it very hard.

In summary, they are riding Microsoft growth and focusing on a segment of clients that are less likely to be served by biggies. We need to watch how they manage growth along with talent cost.

Thank you. I concur with your views. Listening to their concalls somehow gave me a lot of confidence about the sincerity of the management (subjective opinion - I could be wrong).

Theoretically there should be a huge scope to service MSMEs, digitalise their business processes, implement ERPs, etc. What Mr Mian mentioned on the calls was that their ‘consultants’ do consulting and BPR work and not just implement products from the MS suite. Now what kind of value added consulting, BPR kind of work they are able to do would depend on the calibre of their personnel. I imagine it would be a challenge for a tiny company in this space to get high calibre consultants, so that would be a key constraint for them to go up the value chain. But yes, he kept emphasising that a larger share of US client mix would be the key driver for margin expansion.

I feel where All E Tech comes in is that they services small firms which are shifting from proprietary softwares like Tally ERP, Genius etc… to Microsoft business central/ dynamic this is a clientele they focus on.

They don’t target big giants but serves mid to upper mid level market and that too with a fragmented customer base rather than having concentrated client base. The thing which makes all e tech position better off is the hand holding that they provide to there clients because small firm or mid size firm don’t have that strong technological background but with size & coming up of second generation in the business which are technologically mature they understand the relevance of such software for MSME in india the view of seeing technology as an expense/cost has changed they have started seeing technology has an enabler of better efficiency/ reach/ growth and scalability so they are willing to spend money on technology but since they are not so mature they want solution accelerator rather than pure licensed seller or box seller.

They want a firm that helps them adopt to technology, customise it a bit according to there need, understand there long term goals rather than just selling ERP. That’s where All E Tech is in position.

On product they are not very unique provider and all as they picture because any company can provide that but the solution and advice is were they have an edge because to convince a small business to adopt to this system while ensuring smooth implementation needs much more hand holding than what requires at a large firm.

In addition to the above points, I think the main driver of this company (if it becomes a success story) is going to be the plugins they provide apart from the usual microsoft suite of products. The advantage with these plugins is higher margins and most of the time they provide this under the official portal of Microsoft which makes it more genuine and accessible to broader clients.

In addition to all of the technical competencies, is also the question of succession. The second generation takeover and increased competency can also drive the company to new heights.

This is my personal view. Fellow members, please feel free to correct.

Regarding the Succession,

Son of Ajay Ji also works at Microsoft, but I don’t think that he would join also given the age of the founder and the efforts he has given in building this organization. he would need an exit but how he has planned that is somewhat a grey area.

As per me he can plan that in following way:

Selling his stake to the rest of the promoters

His son takes over the business

All E Tech gets acquired by a company who has it presence in SAP, Oracle or any other business application platform but is looking to increase it’s offering by even providing Microsoft business solution.

This are the few ways that I am able to think but it is something of future and is uncertain so I am not weighing on that too much…

My notes on the company based on concalls, AR, credit rating, VP thread:

Business

It helps business to digitize their operations and modernize their technology using Microsoft products. Works with companies in $100K - $1 million project budget.

The company does a high percentage of repeat and recurring revenue (88%) this includes cloud subscription, annual maintenance contract, licensing fees to the IP products.

They are focusing on expanding in Africa and US and enhancing it’s brand image.

Revenue streams include:

Services including consulting, implementations and support/maintenance which generates the service based revenue

Product offering built on top of Microsoft offerings like EdTech 365, Travel365, GreenPower which are IP to the company and vanilla Microsoft products like Dynamic 365, Microsoft 365, Azure cloud service which overall contributes about 40-45% of the total revenue.

Around 5-10% of it is coming from their own IP.

Verticals

Higher Education: Developed EdTech365 which is built on the Microsoft Dynamics 365 suite and is designed to manage all aspects of a university or college’s operations from admissions to alumni relations. Clients like: O.P. Jindal University, Manipal Group Universities.

BAFINS-CX: IP led solution for BFSI built on top of MS Dynamic 365 and Cx platform, with National Bank of Kenya and National Bank of Kigali are clients in Africa.

Green Energy IP and EPC: offering in the renewable sector where they manage the setup of renewable power plants.

Travel365: Caters to both B2B and B2C travel companies, handles operational and financial process for these companies.

Notes

Company does 15-30% margin by offering the Microsoft products directly.

Gross margins in international business is 50-55% while Indian business is 22-23%.

Aiming for annual revenue growth of 20-25% or more by doing more international projects.

The company is actively looking at inorganic growth for expansion and getting more into data and AI and with complementary Microsoft expertise.

A long term goal is to reach 1K crores of revenue in the next 6-10 years and becoming a dominant player in the Microsoft ecosystem.

North America is the key focus and increase the contribution from 61% to 65% in the coming couple of quarters.

There is a chance of margin expansion by shifting to higher margin services and leveraging off shore delivery model.

Competitors in Indian space are PwC, EY, Deloitte, and sometimes Accenture while in US are MCA Connect, HSO, Velosio.

For international projects, they primarily price its services in USD. This reduces the impact of exchange rate volatility on project profitability.

SWOT Analysis

Strengths

Strong partnership with Microsoft and deep expertise in their products, along with new IP offerings

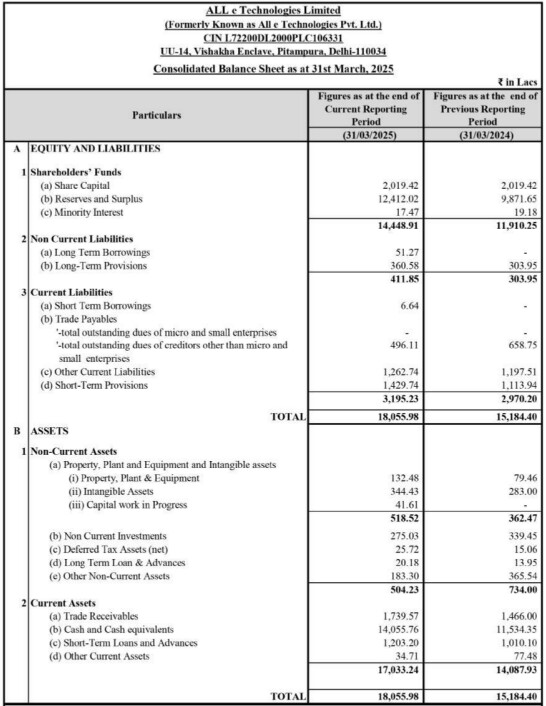

Experienced management with strong financials and a dividend distribution policy and net zero debt company

Weakness

Limited brand recognition and a heavy dependance on Microsoft ecosystem

Lack of marketing and sales expertise and conservative approach to growth

Opportunities

Growing demand for digital transformation, cloud, data and AI

Expanding into new geographies and acquisitions

Threats

High competition along with talent acquisition and attrition

Execution risk in acquisition and any economic slowdown

Let me know if something is wrong or needs to be improved. I used AI as an assistant for my research

Note: Edited out GreenPower as not a lot of information is available in the AR.

Disclaimer: Studying. Not invested

as it was mentioned, it was generated by AI, some times LLM agents hallucinate, in this case, I guess, it pulled this info from waalle renewables. Wa(alle)

This is mentioned in Annual Report of 23-24 page 21 of the pdf. It’s actually referenced twice and I thought probably it’s the same about the renewable business IP they talked about.

Industry Solutions & IP

Industry solutions like EdTech365, Travel365, GreenPower, and the cross-industry solutions of

ProActivate, Cyborg, P2P365 and CEKonnect have

enabled Alletec to stay at the forefront of

competition. The company continues to enrich these

solutions and assess market needs to conceptualize

other possible IP development

Q: Okay. We’ve got a question from Gopi Chand. Since the energy sector is seeing good

growth, do we have product IP to solve problems in this area?

A: So we already have a solution which is for companies who are in the renewable energy

business. We have several customers. Our solution … is built on the base of an ERP and

has got some other components. We help these companies set up their renewable

energy plants.

I myself thought the same initially but I did proofread all the points from the source. So the chance of getting hallucinations should be less unless I have added my own opinions.

Note: I’ll edit it and make it Renewable Power IP to make it less confusing.

QoQ is flattish, and maybe we will get more colour on that in the concall. Their concalls are very heartening to attend. The transparency and the willingness to patiently explain the business is very reassuring. And they are just an SME!

Superb Explanation of the business by @aadhar.aggarwal. I have a small position in this business and the call is on the promoter. My view on steady growth vs Exponential, pretty much aligns with the management. Steady growth invariably will lead to a steady increase in stock price although it may take some extra time. One bad quarter is all it takes to make a villain out of the super Hero. We have seen enough examples of the fastest running horses biting the dust in this bear market.

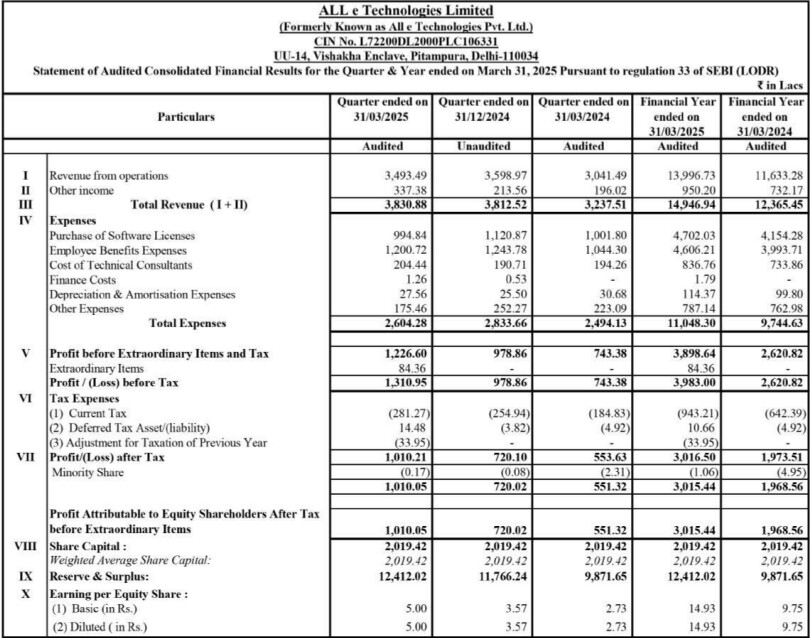

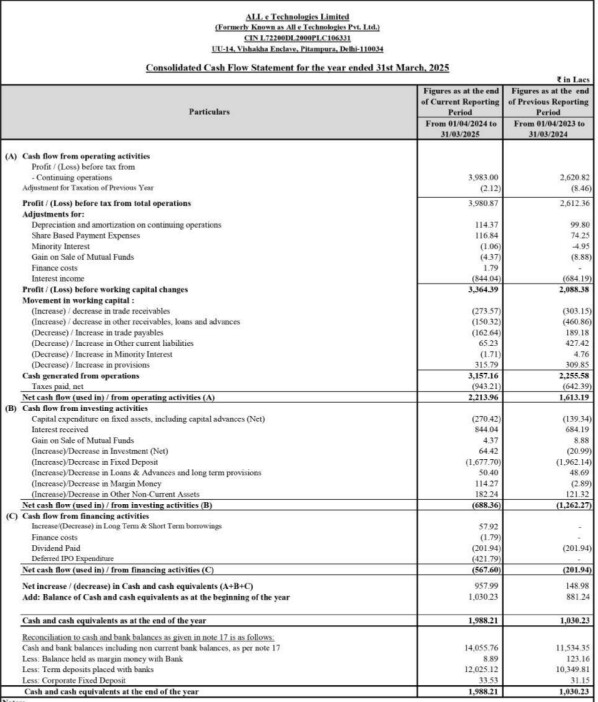

The numbers look very good. Slight dip from the last quarter but good from a QoQ and YoY perspective. Profitability is much better as compared to last quarter and that looks to be from lower cost on software licenses so need to understand how that is possible (similar revenue but lower cost on licenses). Cash from Ops went up this year from Rs 22.5 cr to Rs 31.4 cr.

I eagerly look forward to hearing from Mr Mian and his senior management team on their concall to get more colour on the business.

I think revenues being steady QoQ is a good news when management had highlighted a slowdown in the previous concall. I am pleasantly surprised with the numbers.

However, I would like to understand the reason of employee benefit expense going down QoQ. I would appreciate if someone from this thread asks this during concall. Thanks.

Geographic expansion into the Middle East (Dubai office) has already started paying dividends. Two new clients from that region, if I remember correctly.

Won a tender from a Canadian regulatory body, over others in the fray, such as Deloitte

I didn’t get to ask the question on QoQ decline of the two cost line items - Software license and employee benefits. I have emailed them and shall share any updates.