Thanks for the kind words. Few observations from my end:

As you have rightly pointed out, how much of the shipment translates into revenues is something none of us know. We have been hearing that it is possible that all the yearly shipment have already been done in bulk for the whole year or for 180 day exclusivity period. However, it is to be noted that more than Rs.500 crore of shipment data was for the month of June and July (up to July 6), though much less than the data for April and May. Also, how much of the shipment data is captured by Zauba is also a question mark. It can be more or even less.

Revenue sharing agreement with the partner is also something we dont know and Alembic doesnt share with the investors. However, I think as you have calculated, 40% is something we can work on conservatively (if I remember correctly in one of their concalls they had mentioned it to be in the range of 20 - 40%).

Margin expansion is definitely possible and I have seen that in few of the companies we track that launched products during 180 day exclusivity. However, I think it will be difficult to sustain that post 180 day exclusivity (post Q1 and Q2) as there are already six players including Indian companies like Zydus and Sun which have tentative approval for the drug. It will get very competitive post the expiration of 180 day exclusivity period.

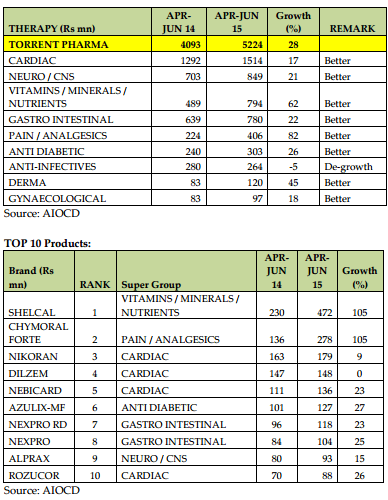

These are some of the blind spots we will come to know post its Q1 results. We can get an indication of that from Torrent’s results which will be declared on July 27th. The surprising thing to note here is that Alembic is not forward integrated into marketing its own product but is backward integrated into manufacturing of APIs while Torrent is forward integrated with its own marketing set up for the US markets but isn’t backward integrated into manufacturing of APIs.

However, as seniors have pointed out we do not factor event based triggers in our valuations. But we should note that Alembic has a great pipeline for the next two years with around 15 - 16 products lined up. In addition, it has good complex R&D skills as we have seen with 20 months exclusivity for gPristiq (NDA - desvenlafaxine).

Great eyeopening write up on alembic pharma.WE needto work hard n forget price anchoring.what cud be the expected EPS for next 2 years?

were u able to raise these queries at ajanta AGM.If so what was the response.

I dont know what the EPS would look like for next 2 years. We can estimate that only after the Q1 results. It becomes pretty difficult to factor the sales and profitability from a product with 180 day exclusivity. Also, key thing is the approval for other products post expiration of exclusivity for Abilify.

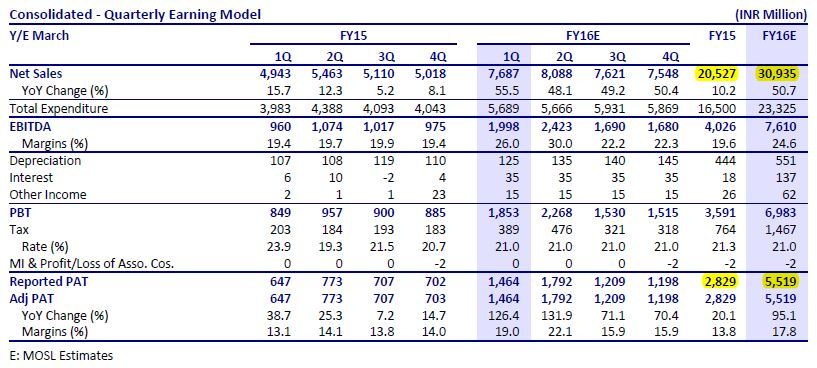

Lower US base and gAbilify launch in the US is expected to increase Alembic Pharma’s sales growth 55% YoY (1.55x) to 770cr, with 14.6% growth in domestic and 187% in international generics.

EBITDA is likely to grow by 108% YoY (2.08x), aided by favorable business mix (margin expansion of 700bps).

Overall PAT is expected to grow 130% YoY (2.3x) to ~150cr.

USD35m sales (on a conservative basis) expected from gAbilify in 1Q.

The difference between standalone and consolidated sales in torrent in 1Q16 is just 80 crore while consolidate profit is around 380 cr less than standalone profit. any reasons for the same ?

As per Sandeep’s post few days back, Alembic, Hetero and Torrent together shipped 1700c of Aripiprazole. Torrent sales outside India have gone up by 565cr from 722cr to 1287cr. Assuming a growth of 10% on other products, we are left with a guess of 565-72=493cr of Aripiprazole by Torrent. This is very close to Sandeep’s estimate of 461cr ( will be even closer if we assume a higher than 10% growth on non-aripiprazole products).

So we are on track for Alembic estimates.

However, Torrent is trading at 25x trailing EPS. It may give a sharp run up from here on.

Torrent sales outside india incude brazil and europe and others. So, you have to consider that.

As per Q1Fy15 call they did 269cr to US and today press release they said US did 231% growth. So around 890cr would be US sales. Q1FY15 of torrent had similar one time sales of cymbalta around 110cr.

Q4FY15 had US sales of 225cr.

Even if you take 225cr of Q4FY15 as a base it would be around 665cr.

Note that this quarter has only two months of sales of abilify

We should look at consolidated financials rather than standalone. I think the management would clear the doubts regarding the same in their concall tomorrow. US sales during Q1FY16 was Rs.890 crore (231% growth over Rs.269 crore US sales recorded during Q1FY15). I think Abilify sales would be more than 100 USD million.

expenses related to elder and zyg ,with these two yet to generate significantly to cash flow may be reason behind standalone and consolidated.mgmnt should clear this tomorrow.

Guys, this is Alembic thread and too much of discussion of torrent in this thread is not appropriate. Yes since Aripiprazole is sold by Alembic & Torrent in US, that much discussion was OK. But for further discussion on Torrent, please create a different thread.

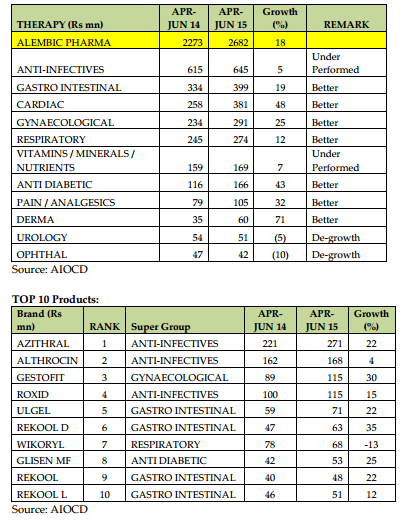

Why are Alembic results so poor? Weren’t profits supposed to more than double in the quarter? International generic sales up only 47% and this has been neutralized by 63% decline in international branded. Does anyone know why impact of gAbilify is so weak?

Revenues up 19%

PAT up 8%

International generics up 47% to 168Cr. Torrent had sold approx 600cr worth of Abilify. Alembic claims a successful launch of Abilify on day 1. To me, it looks a bit disappointing to say the least. Looks like they lost to others.