I bought today around Rs 1255 to the tune of 5% of my PF worth. I’m averaging up from Rs 360 levels. Will keep buying more if there is any “Ajanta Discount Sale.”

Trading at less than 30 times forward PE and looks fair for a 15-20% growth predictable business with US business kicker yet to play out.

Does any one correlate the reason for recent fall from 1450 to 1170. All most 25-30% in 2 months.

I assume that ZAR vs INR fall from 4.7 to 4 might be the reason as most of the revenue around 60% from south Africa and recent correction on USD to INR might highly impact on revenue etc.

I had asked co’s IR last yr about the impact of African currencies when Nigeria currency depreciated by around 30%. He replied that they book revenue in USD and depreciation of african currencies have no impact on Ajanta.

As per my knowledge, all global wire transaction happens on USD currency. So first domestic currency converted against USD and USD transfer to India INR. So is it correct or they are doing some hedging the currency like IT company or ?

Let me know if you have any further info about currency impact.

My sense is that if they book revenues in USD, they essentially quote and receive funds in USD. In that case the only impact a weakening ZAR can have is lower purchasing power of South Africa.

The drop in Ajanta’s stock price does not surprise me much as 45-46 PE was outrageous.

I am more comfortable buying again at 25-30 PE.

The major driver of PAT growth over recent years was margin expansion which seems to have topped out. I am not saying that there may not be a 4-5% variation going forward, but margins look stabilized now compared to other pharma cos.

My thesis of investing in Ajanta is the revenue growth which looks to be compounding at 25%-30% CAGR. This alone is sufficient to make it a good investment bet at 25-30 PE.

Further margin expansion, if it were to happen, will be an icing on the cake.

I think a PE of 30 is quite attractive for Ajanta not only because of the 15-20% growth in profits, but also on account of the exceptionally high RoE of the company.

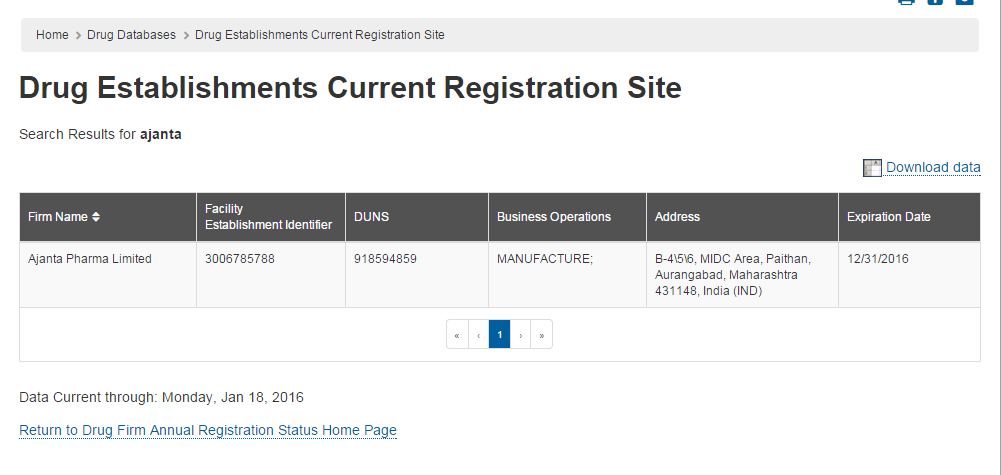

Establishments must be registered within 5 days of beginning operations. (21 CFR 207.21(a) and 207.40 and FD&C Act sections 510(c), (d), & (i)). In addition, establishments must renew registration annually between October 1st and December 31st of each year. (FD&C Act sections 510(b) & (i)).

Firms that send their initial or annual registrations during October 1st to December 31st period are considered registered until the end of following year. If a firm submits its initial, updated or annual registration outside this time frame, it is considered registered until the end of the current year and shall renew before December 31.

Most likely scenario is -

They may have registered between Oct-Dec 2015, due to which they need to renew the registration for 2016.

What we do know is the following:

Unlike Torrent which had FDA Inspection on April 2015, Ajanta has not had that 1st inspection yet.

But since they are sending regulatory filing batches, they would have been allotted a FEI (Facility Establishment Identifier) which would imply they may have been registered.

As for Torrent, since they had started commercial operations in Nov 2015, they would have been expected to register within 5 days as stated above.

I may be wrong with my assessment and others can correct me.

Hi,

I was going through the BS of ajanta pharma and observed that their fixed assets haven’t increased much in last three years . Does that mean their assets are getting old and will need to invest more in coming years

Torrent has only for EQ 20 mg base, but Ajanta got tentative approval for multiple strengths. does it mean Torrent has to apply again for other strengths?

Slowdown in key Derma brand Melacare. Management has trimmed down domestic growth expectation in Q2FY16.

Moving away from low margin Domestic Institutional business (down 75% YoY to 7cr) to continue focus on Domestic Branded formulations (up 17% YoY to 128cr).

Ajanta’s USP has been knack of launching maximum number of first time launches. Of 188 actively marketed brands, 129 brands were first in India. Just need to continue this trend to get back to ~25% domestic growth.

“… Our target is to file more than 10 ANDAs every year and we are looking to file the products where there is a limited competition kind of scenario which are more complex and extended release, delayed release, controlled release, those kind of formulations. We are very poised to do those filings next year, particularly with the Generic Drug User Fee Amendments (GDUFA), the commitment from the FDA, to approve the ANDAs as per the predefined timeline. So, the approvals should come fast and we should be able to make those ANDA approvals, convert them into the numbers faster than before…”

Yogesh Agrawal (on the sidelines of the Antique Investor Conference)