Thanks very much for the AGM notes Mihir. Appreciate your effort.

1 Like

Thanks a lot Mihir, appreciate details from AGM.

1 Like

From recent India Nivesh note on Ajanta Pharma

We recently interacted with management of Ajanta Pharma (AJP) to get better insight on future outlook on both, domestic formulation as well as exports.

ANDA approval remains key for increased business from US market

AJP has filed 25 ANDAs from its Paithan facility. Out of these 25 ANDAs, 2 are approved and one is launched. AJP had sales of Rs40mn with market share of ~12.5% from one ANDA in FY15. AJP has 23 ANDAs pending for approval, which has potential market size of US$1.5bn post genericisation. It has mix of para II, para III and para IV ANDAs. There has been delay in getting the ANDA approvals. There has been similar delay for other companies as well due to GDUFA implementation process. We expect sales from US market to improve strongly, once the pace of ANDA approval picks up. In addition to existing facility at Paithan for US market, AJP has completed construction of new facility at Dahej with capex of Rs2.2bn. AJP is expected to start exhibit batches soon from this facility.

AJP is expected to maintain momentum in building infrastructure with capex of Rs4bn for next two years. The capex is mainly for new manufacturing facility (location is to be decided soon), expanding R&D facility and maintenance capex.

The new manufacturing facility would enable higher growth in business over next 2‐3 years. The capex would be funded by internal accruals.

New products and higher share in existing products led better‐than‐industry growth in DF segment

AJP’s domestic formulation business has grown at CAGR of 29% over past five years. Such superior growth in DF has been mainly due to new product launches and increased productivity. AJP had launched 26 new products in FY15, out of which 12 were new to market. The MR strength stands at 3,000. Therapy‐wise, Ophthalmalogy, Dermatology and Cardiology have been the key drivers for robust growth in DF sales. We expect AJP to deliver 27% CAGR over FY15‐17 on the back of new product launches and increased traction in existing products.

Branded generics and Anti‐malaria remains key growth driver in Emerging markets

Exports to emerging market grew at CAGR of 31% in past five years. Branded generics and anti‐malaria segment has been the key driver in Africa segment, while branded generics has been the key drivers in Asia segment. AJP had launched 30 and 18 new products in Africa and Asia segment, respectively in FY15. The pipeline for registration of products remains strong giving enough confidence for strong growth over next 2‐3 years.

R&D spend as % of sales has been 5% for FY15. It is expected to increase to 6% for FY16. R&D effort is going to be for developing new products in regulated as well as emerging markets.

3 Likes

Disclosure: Invested from lower levels

Official minutes of meeting also available

http://www.bseindia.com/corporates/ann.aspx?scrip=532331&dur=A&expandable=0

1 Like

New here and seek advise. Is this okay to enter at this level 1600?

Welcome Mr. Sudipsand…here in valuepickr you shouldn’t expect that someone will tell you buy or sell except administrator through VP PUBLIC PORTFOLIO. But that’s also now stopped since last one year, no updation on that portfolio due to RBI clauses. But Ajanta is great company, it’s expected to do well in future too. However, I will suggest you to buy after the july qtr result. If the result is not as expected then there would be fall and you may get it at low value. And if it goes high then also you can buy if your investment horizon is long.

Ajanta management interview in Forbes under Super 50 companies

Key highlight is

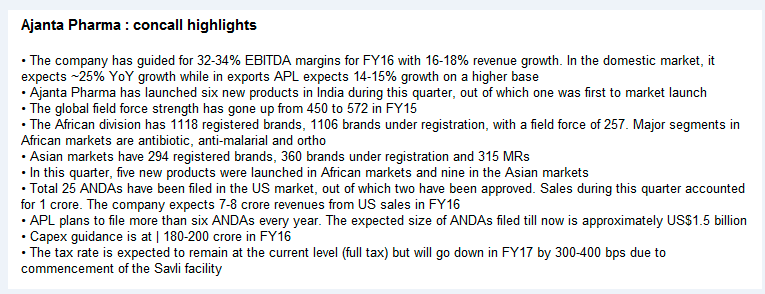

In a conference call with analysts, Ajanta’s management has indicated that its EBITDA margin should sustain at 32-34 percent in FY16 with a 16-18 percent revenue growth.

2 Likes

@idikasony

This is what I got sometime back from a friend.

Regards,

Raj

2 Likes

Excellent article on Ajanta in Forbes India Super 50 companies.

2 Likes

An excellent article by Mckinsey on Africa being the last major growth market.There is a lot of importance being given to local manufacturing.As such is Ajanta going to suffer? Seems its not present in major African countries and is focused on smaller Franco African nations.

Views Invited.

1 Like

Ajanta Pharma gets approvals for 3 ANDA’s

- Montelukast Tablets, Chewable Tablets and Oral Granules

- For the 12 months ending June 15, the above three had sales of $237m, $87m and $31m respectively (per IMS Health)

- Ajanta now has 5 approved ANDAs and another 20 ANDAs under approval with FDA

One more in the crowded space - http://www.accessdata.fda.gov/scripts/cder/drugsatfda/index.cfm?fuseaction=Search.Overview&DrugName=MONTELUKAST%20SODIUM

5 Likes

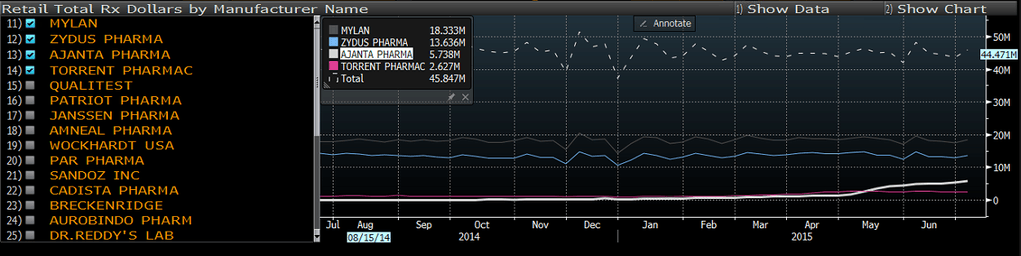

It’s heartening to see Ajanta gaining market share in Risperidone in the US market.

Source: https://pbs.twimg.com/media/CJm1APEUAAEA4fZ.png:large

Risperidone is a crowded place too; 12-13% market share is quite an achievement. Not clear to me if it is through Breckenridge Pharmaceuticals or through its own front-end sales and marketing team in the US.

13 Likes

@lustkills

Ajanta markets its own products whatever the market india africa or USA. Even with single product respirodone in US they have set up its own front end marketing and doing well as seen in market share of respirodone.

Montetlukast looks to be crowded. But many times what happens is that margins will be lower with multiple players and many biggies will move out and then again it becomes attractive.

4 Likes

@ananth - glad to read own front-end marketing confirmation - thanks; will happily disregard the following Oct 2012 announcement now.

Cheers!

If one reads the AGM notes of Ajanta (its on BSE) - they mention that co’s strategy is to have own front end team in US. Believe this was communicated by company earlier as well and I believe is one of the great advantages of Ajanta (having own team helps in getting higher margins if the product is limited competition product).

1 Like

Hi Sandeep

Dont know how to read this chart about Risperidone. Does this mean Ajanta has sold $6 M of this drug in June? If yes, then even at these levels, it translates to 35 Crore sales per month for the drug or 400Cr+ annually. That’s huge and will translate to 30% growth in overall sales just because of this molecule!!!

Or is there anything i am reading very incorrectly?? I am sure I am wrong, could someone please explain more about the market size etc for this molecule?

@sinhalgaurav

Don’t know for sure either. Per Ajanta’s maiden product drug launch announcement, Risperidone had total sales of $147M in U.S. for the 12 months ending March 2014. This indicates the chart could be illustrating running total sales of the last 3 months (quarter) reported on per month (Y-axis) - a guesstimate.

Ajanta reported 4cr Risperidone sales in FY15 from regulated market (U.S.). Chart illustrates market share gain from 1-2% to 12-13% in May-June. Means Ajanta could report 25-35cr sales from U.S. in Q1FY16 results. Would love to be proven wrong on the positive side (AP is highiest allocation in my PF) ![]()

{kind=link}

Risperdal’s global peak sales was $4.5B in 2007.

Source:

4 Likes

Few things regarding the graph attached above:

Till March the % share of Ajanta was around c2-3% and before that (during FY15) - it was even lower. Accordingly Ajanta recorded sales of 4cr for full year from Risperidone. Only in May, June the % share jumped - hence somewhat better numbers can be expected in FY16

The $ amount sales which we can see to be around $5-6m in latest week, this can be bit misleading because this sales is at Retail level (mentioned in the chart itself), this is similar to MRP in India. So this $6m will have retailers margin as well. What sales Ajanta record in its books will be significantly lower. There can be timing issues here as well, when the drug actually got sold in the market (which will be captured in the above graph) and when Ajanta sold drug to the distributors, etc. In short, its safe to assume more than 50% haircut to what approximations we get from this graph.

Given the data, believe sales of 15-20cr can be expected from Risperidone during Q1 for Ajanta.

6 Likes

Great Q1FY16 results. Operating Revenue up 22%, PAT up 41%.

1 Like