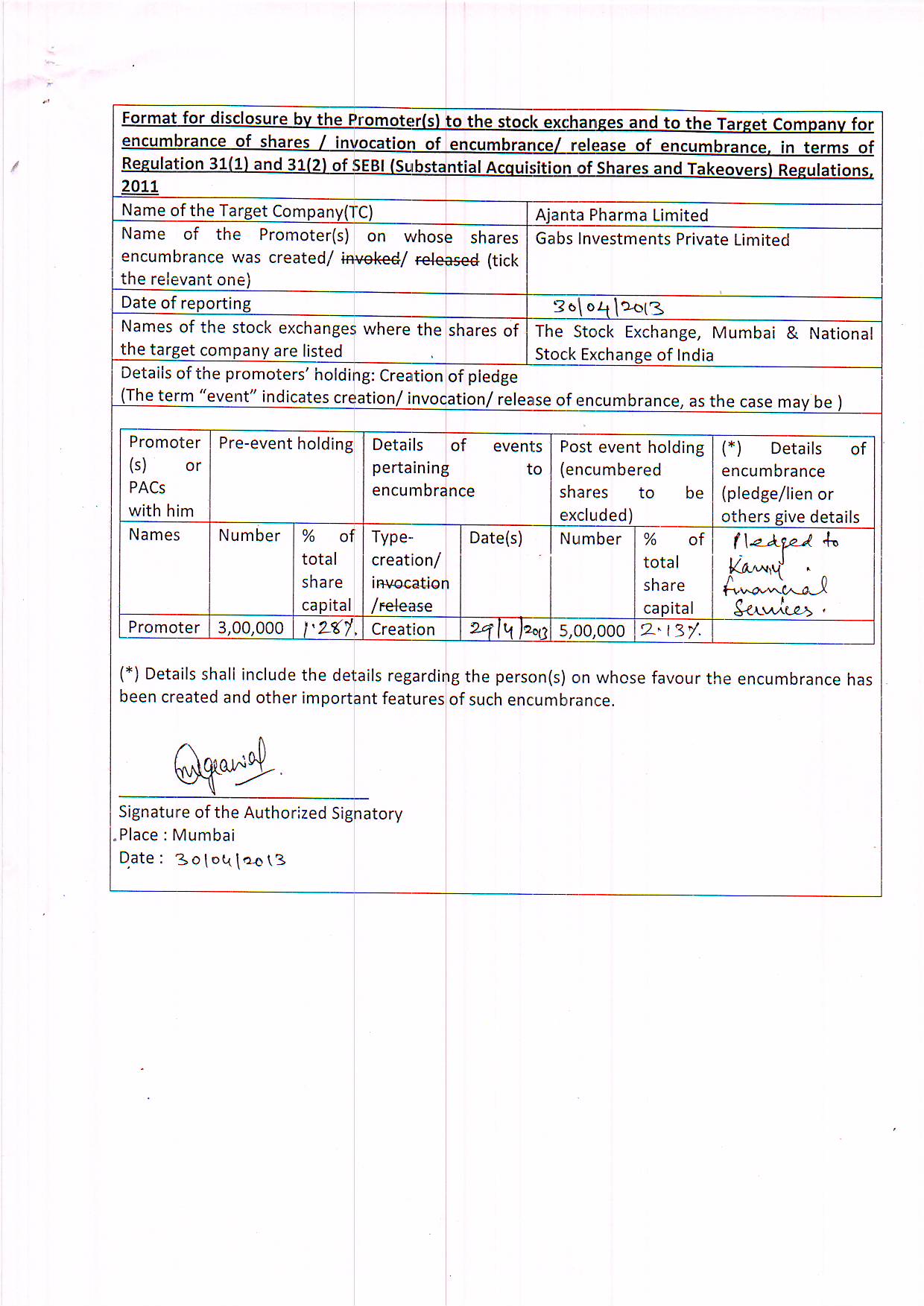

@subhash - I haven’t seen anyannouncementover last few months wherein they have pledged their shares. Or that they are buying and pledging. I think the pledging of some shares - about 6% of total, was there since quite sometime and now the same is getting highlighted to show concern.

On the taxation - co has written that 15.75 Cr is towards earlier tax. What I think about this is - earlier there was a news item that objections were raised by the IT department over the tax benefits the co was claiming due to huge R&D (earlier tax was 20-22%). It seems Ajanta has stopped claiming the tax benefit of the same and is now paying full tax of 33%. We should consider this as the tax rate going forward.

Usually the mutual funds are fairly active in the Pharma space and you will find most stocks picked up by some funds or other. Despite this dream run, Ajanta never features in the buy list or holding of any mutual funds. Any inputs in this regard from anyone ?

Ajanta was a 200 cr. market cap company just 2 years back. Most of the MFs avoid stocks with less than 500 cr. market cap. By the time the stock moved to 500 cr + category ( almost a year back), it has already moved too fast for their comfort. Typically, they would want a cool down period to buy their big chunk slowly. That has never happened in this counter. There was a period, when the stock was at 400 for quite some time, but then there was a taxation issue, so they were away from this stock. And in last 6 months stock is again up 2.5 times.

Basically, you will rarely find a stock that becomes 10 bagger in a matter of 2 years. There are very few examples in the market(I think TTK and Mayur belong to this category), and most of the big players miss these companies.

P.s. - My opinion is biased as Ajanta is my largest holding and I am holding it from much lower levels.

Not debating on Growth prospects, re-rating , promoter buying etc.

Just want to understand one simple thing. If all the above things are true then despite such high volumes why is the delivery percentage in the scrip less than 20% (it has always been so).

Want to understand ow is this happening and what are the implications of the same

Why bother about daily indicator like delivery percentage, share price for such awesomely growing secular stock. One should have a long term view for such stock, and check for quarterly numbers (few information once in 3 months). At least you can save your time and energy, will have less mental stress, and enjoy life much better way.

The max one can check is PE ratio, for finding if the stock has moved to irrational over-valuation zone, but it also happens once/twice a year.

The next issue is timing the market. After reading few books, I am convinced that no one has any special capability of market timing, and it is just plain luck. SIP type buying is the way to go for suitably taking advantage of different price levels at different time.

The beast approach is to go for SIP way for good ROE/ROCE, low DE stocks at a cheaper valuation. I track my portfolio (not individual stock, mind you) and I find it an excellent approach for generating wealth consistently. One can beat sensex hands down via this approach.

I agree Subhash…Respect your views, and started by saying that Im not debating on valuation/growth.

Just wanted to understand, that if Delivery Percentage is so low, doesnt that mean there is circular trading going on. There must be some science behind this number.

Hold Ajanta. Its 7% of my portfolio. Almost free shares.

based on your estimates (3.5x), one year forward PE is 15, which would be reasonable price for the stock if the company just reaches 150 Cr as this would be a moderate growth. So the stock wont have much upside from here.

But a better results (170 cr), lead by better perfomance and a PE of ~17 which would lead to possibility of around 30% upside.

The risk is of retrospective taxation stays with the company, which maybe a dampener.

The contribution from subsidiaries of Ajanta Pharma,

Sales

Net Profit

NPM(%)

FY10

26.05

5.46

20.96

FY11

47.72

4.26

8.93

FY12

73.13

10.78

14.74

FY13

91.64

10.99

11.99

As the subsidiaries of Ajanta are not at all insignificant, they deserve a look.

They contribute around 9~10% to its bottomline.

The sales have been going up at CAGR of 36%, if they maintain the same pace at NPM of aroud 11~12 %, they can contribute significantly to the business from long term perspective.

Are the revenue mainly from Malaysian subsidiary only? As the management had suggested 47.8 crore revenue in FY11 from Malaysian subsidiary and subsidiary sales were 47.8 crore in that year.

Does anyone have sense of outlook for the subsidiaries, as they can contribute more to the business going forward.?

R&D expenses was around 56.25% of NP in FY12, so materially a huge amount of Profit is invested back in launching new products. So what are the success rates(R&D) in the segments it operate? Does more spending in the segment it operates materially leads to higher revenues going forward with more products, or is there any chance of research products going obsolete and hence R&D expenses going down the drain. On an average for each rupee invested, how much of revenue can company expect moving forward?

Management in the Q&A said marketing spends are at similar levels to R&D expenses. So the spends on finding the gaps in demand supply side for individual countries will continue. But can’t the company reduce the expense on other aspects of Marketing, once there is sufficient demand of its products. Does this require continuous effort from sales team to pass through its products and create demand? As the marketing expenses are at similar level to R&D expenses and hence I assume around 50% NP, isnt reducing this expense going to lead to better OPM/NPM for the company.

API division is only for in-house usage or commercial production has started?

For a company with only 100 crore in profits, does preventing outsourcing and increasing operational efficiency along with in-house capabilities justify 400 cr in expansion?USFDA plant, if it cant get revenue of 200 cr, isn’t it imprudent investment of capital?

Love it when company like Ajanta falls without any change in fundamentals. Give me chance for accumulating at a lower price point.

A slightly pessimistic 0-growth model of 42cr EPS each qarter gives me next 12 month eps 168-170cr. At a pe of 17.5 Mcap after 1yr is 2940 crore which is cool 55% up from cmp.

If I take a pe of 16.5 (a more conservative pe) I get 47% gain. Seems to me solid buy at 800-820 range.

Disc: Ajanta is my top holding (23% of my portfolio). Aggressively converting my minor holdings to Ajanta at 800-820 range

for company having net profit of 165 crores at npm of 11% u need sales of 1500 crores. In fy 13 they did sales of 920 cr. Effectively we are hoping for a sales growth of more than 50% for fy 14 which seems difficult on a higher base of fy 13.

Other option is company could increase npm to more than 11% – now this will have to be done after overcoming full tax rates, higher interest expenses due to planned capex and higher depreciation due to expansion.

And coming to valuations, at 165 cr net profits (say somehow company does manage to pull it off) then also , applying a 15 PE would amount to a target market cap of somewhere areound 2400-2500 crores. Thats a 20-25% upside. (current market cap is 2000 cr)

Now for this to happen company has either to do 50% sales growth or improve net profit margin inspite of the factors listed… This to me seems like a tall order.

First quarter should set the tone for what to expect for fy 14.

Ajanta has been doing 45-50% np growth in last 3 year. If I assume a 40% growth rate in NP this year (assuming last quarter tax has taken care for the tax outgo for entire year, so I need to do nothing special), I get np of 157cr next year. The type of growth ajanta is having, I guess we can have a pe of 17 for ajanta (typical lower end pe for good pharma companies). I get 2669cr of NP (30% upside from current price, and 45%+ upside if bought at 800 price point).

I agree that I have over-calculated it to 165cr as I missed subtracting other income of 6cr from last quarter figure.

{kind=link}