As per this local news article:

”The project envisages dismantling ageing infrastructure and carrying out a comprehensive redevelopment of Berth No. 9 to facilitate handling of liquid bulk cargo such as crude oil, petroleum products (POL), and liquefied petroleum gas (LPG). As part of the modernisation initiative, the berth draft will be enhanced from the existing 10.5 metres to 14 metres, with a future-ready design provision extending up to 19.8 metres. This upgrade will enable the port to accommodate vessels up to 2,00,000 deadweight tonnage (DWT), including very large gas carriers (VLGCs)…………….The construction period is pegged at two years, while the overall concession period will extend to 30 years, including the construction phase.”

So long term infra is being setup for VLGCs, not sure when work will start, but with a 2 year construction period, this should be sometime after FY29. Berth 9 current capacity is 2.2MTPA, which will be upgraded to 10.90 MTPA.

The article is concerning, since it might indicate LPG imports might struggle due to the affects of the Iran war. How this impacts LPG sourcing and throughput through the Aegis terminals, will have a huge impact on revenues of Aegis. Hope in the FY26 Q4 conf call (mostly May end), the management can throw light on the impact on volumes.

The picture is very unclear as of April 2026,although the LPG shortage has brought in focus the strategic importance of a company like Aegis. Had it been the 70s the government sensing the sysytemic importance of Aegis assets would have promptly nationalized it !!

The times are different and the government currently has a growth mindset. Hence the following announcement.:

This bodes further well for Aegis as the government focus is on building pipeline infrastructure and not port infrastructure.

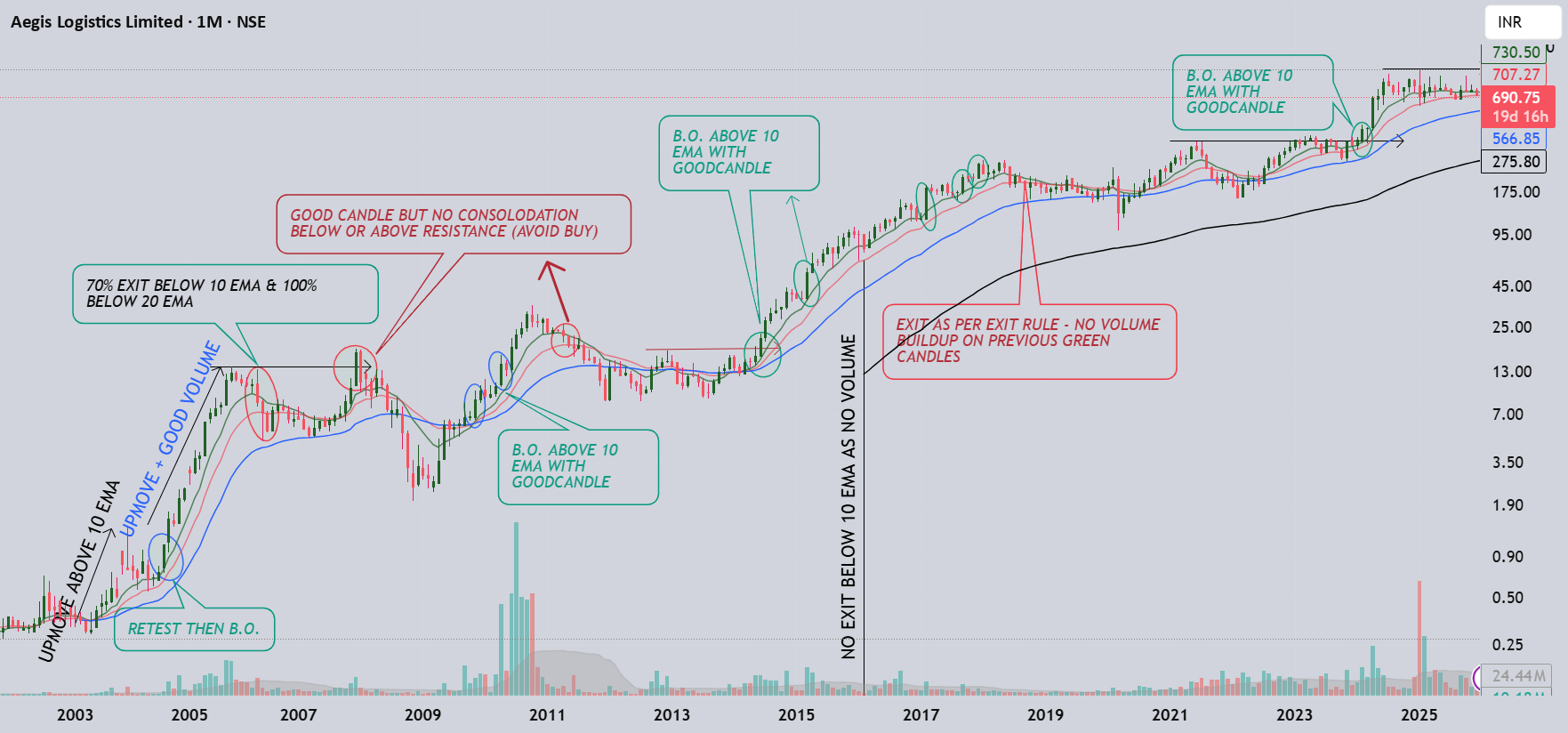

Disc: added in the fall around 600/- ( the window of oppurtunity was quite small, I was thinking of adding further around 500/-)

Sorry for asking very basic question. In view of recent LPG disruption across the whole country, does it is reasonable to say that upcoming quarter results will be bad for Aegis logistics? How we are arriving at the margin of safety in 600 rupees share price? I know it is very hard to value or assign quantum of margin of safety at any share price, but in rough senses what is prompting us to buy Aegis when we know that it profits depend on volume of LPG it handled rather than price of LPG.

As I have viewed Aegis over last few years is that it is more of an infrastructure play ( return on fixed asssets) rather than a P/E multiple play. When i first bought in 2023 ,I expected the stock to double in next 3 years which it did as the management was able to successfully ramp up gross Block from 4148 Crs in March 2023 to 5875 Crs in March 2025.( There is CWIP of about 1308 crs as per the last results) Now the margin of safety lies in the time horizon for which I am investing..now I have tapered my expectation and when viewed with a fresh lense I am ok with Aegis doubling in a 5 year time period i.e by 2030 (15 % return).I am making very simplistic assumption of 10,000 crs gross block,2500 crs profits and 50k crs market cap by 2030. Instead of calculating to the last decimal I like to be comfortable with my assumptions. Also, Since I have not sold my earlier holdings the returns for that would also get baked into the final outcome if all goes well. One must always keep in mind that nothing in stock market goes as planned,there can be pitfalls but currently there is low debt,clear ownership, clear management vision and focus. I like these filters and would pay up if these get satisfied. There is a brilliant chart posted by someone on tradingview showing periods of consoldation when work-in-progress is there and stock price bump-up once the project gets completed. The very long term holders have been very suitably rewarded.

Aegis will be beneficiary due to the below news item, since in Nov’25 they announced the signing of a nonbinding memorandum of understanding with Larsen & Toubro to develop an ammonia terminal for their upcoming green ammonia project at Kandla.

Commenting on the development, Subramanian Sarma, Deputy Managing Director & President - L&T, said: “The agreement with ITOCHU is a significant step in translating L&T’s clean energy ambitions into large-scale, bankable projects. By securing long-term demand through a reputed global partner like ITOCHU, we are strengthening the commercial foundation of our green ammonia platform, while contributing meaningfully to global decarbonisation”.

Hiroyuki Tsubai, Executive Vice President, Member of the Board, and President - Machinery Company, ITOCHU Corporation, said: “Establishing a reliable and scalable supply of green ammonia is critical to accelerating its adoption as marine fuel. Our partnership with LTEGL provides a strong and credible supply base, enabling us to expand our bunkering business and support the shipping industry’s transition towards low-carbon operations”.

When everyone was thinking that aegis would suffer a huge setback due to the ongoing middle east war,they have hit it out of the park. New LPG capacity at Mangalore & Pipavav came online, tripling throughput potential. The Management has been unfazed by the global upheaval and have followed the path chalked out by them earlier over last 3-4 years. The underlying growth trajectory is real and multi-year in nature although there was a one-off gain of about 111 crs.on sale of subsidiary to AVTL.