@rupeshtatiya @desaidhwanil https://www.bseindia.com/xml-data/corpfiling/AttachLive/cedcf7ec-c9a1-4a0e-8f7a-fa20e4000e5c.pdf

1 Like

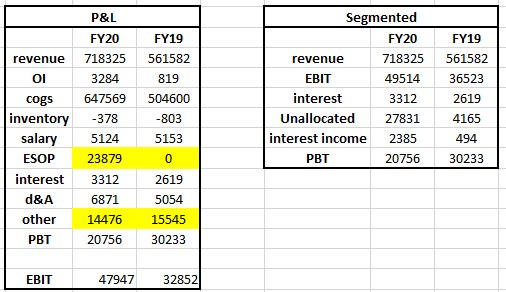

Can anyone throw light on this item

it has increased to Rs. 278.31 cr vs 41.67 cr from last year?

Disc: Not Invested

Hi where is this from? Could not find it in the quarterly result or presentation. At a preliminary glance it looks like they have clubbed ESOP charges.

P&L table is from pg. 14 and segmented is from pg. 15.

EBIT in P&L is my calculation. Have excluded only ESOP and Interest from EBIT calculation. Still it doesn’t fully match the EBIT in Segmented table. I am assuming the Segment Results on Pg. 15 represent EBIT.

As for unallocated expenses, it has increased by 237 cr over the FY, which is the approximate value of ESOPs charge in P&L. The rest of the unallocated expenses in both years must be coming from Other expenses.

You can always contact the management for further clarifications on any financial statements.

Announcement by Co

Conference call takeaways

Volume update: LPG throughput volume in gas segment was down 4%yoy to 722,514

tonnes; LPG distribution volume declined by 21%yoy to 32876 tonnes. Management

expect recovery in high margin retail volumes in 2HFY21. Sourcing volume declined

significantly by 74%yoy to 142,911 tonnes due to lower volume by oil PSU companies.

Liquid capacity expansion projects at Mangalore, Kochi and Haldia are expected to

complete in 4QFY21 providing growth in FY22.

Uran-Chakan LPG pipeline commissioned in June 2020 and rail gantry project for LPG

movement at Pipavav is expected to be commissioned from 3QFY21 with additional

volume potential of 0.5mn tonnes each.

New LPG project at Kandla with capital expenditure of Rs 3.5bn is expected to complete

in 4QFY21 and management expect c. 1mn tonne volume in FY22.

For automobile gas retailing, it has a network of 120 retail stations in ten states under

the Aegis Auto Gas brand, for which it plans to have a national footprint – with 200

stations in 20 states.

The National Green Tribunal (NGT) Delhi has demanded Rs 1.42bn for alleged air

pollution in Mumbai. The Supreme court has directed a stay on NGT order and company

is hopeful of no material liability arising from same and no provision is made.

2 Likes

Will PNG replace LPG in long term? I was thinking that this might be one of the risks. But it seems like goverment will keep on pushing for LPG in rural areas as mentioned in below article. Sharing this informative article which gives more details on India’s cooking energy needs.

Results Dec 20

2 Likes

Transcripts are usually available on Trendlyne or research bytes and Tikr, so far none there (none on company website yet)

Here is the investor presentation

MOSL Coverage AGIS-20210129-MOSL-RU-PG010.pdf (525.1 KB)

Is there any immediate impact on the operating expenses due to Suez canal blockade ?

Note : This blockade is cleared earlier in the day and traffic is going to resume shortly

5 Likes

Q4FY21 result.

Below are my notes from the concall. Also attaching the company presentation with some annotated notes

-

Revenues fell due to lower LPG prices, 1101cr vs 3000cr, Q4 EBITDA 145.4cr same as Q3, YOY drop of 8%

-

Q3 and Q4 recovered. H1 had national lockdown effect.

-

Liquid revenues up 23%, EBITDA up 48% yoy. Excellent performance. Shows resilience of business model despite covid, customers kept business. Record EBITDA for full year. All terminals drove good figures

-

Margin 82% vs 60-65% normally. Change in mix - handled higher margin products. Some saving on expenses but all additional revenue has flown into EBITDA.

-

Sustainability of high margins- We think its sustainable and we are bullish on it as a result of India’s requirement of chemicals, petrochemicals and petroleum for many years to come.

-

Pipavav occupancy only 20-25%. Rest all at high levels

-

-

Gas division- Q4 EBITDA drop of 25% yoy. Weakness in gas sales volumes. Every LPG segment affect by COVID, even before latest surge. Expect it to change

-

LPG througput volumes in Haldia, Mumbai, Pipavav dropped 2%. Earlier guidance was ramp up in Q4 but didnt happen because Pipavav BPCL didnt start and Haldia loss of BPCL.

-

Industrial sales down 30%.

-

AutoGas down 14%.

-

LPG cylinders down 15%

-

-

Outlook FY22.

-

Very good expectation for liquid as result of capacity increase. Mangalore (50,000KL) will start in Q1 and all tanks are sold out. Haldia (54,500kL) also in Q1, already booked. Normally new capacity starts with lower margins and then picks but these are already high value from day 1. This is a good sign for our liquid business. Kochi 20,000KL expected in H2.

-

Gas- Despite recent surge in COVID in April may. Retail will continue to be affect but we expect improvement in LPG throughput because

-

Kandla LPG project (Big project) delayed from plan of Q1 to end of Q2. So numbers will flow from H2

-

More rail movement in Pipavav will boost throughput. Rail gantry started in Jan with IOC and just now signed BPCL for significant volume, to start from June. One customer left HPCL and will start discussions now. Expect good recovery from Q2 and gradual pick up of vols. One thing that could further boost Pipavav is if we could bring Very Large Gas Carriers (VLGCs) into Pipavav, but that requires some jetty modifications by the port. That work is delayed. Today only mid sized gas carriers can come in. That can be possible by H2.

-

Chakan pipeline is operating at full capacity since December. Full year of throughput in FY22. Mumbai can operate 1.2-1.4MT per year and can increase a bit more to max 1.5MnT depending on demand.

-

Some bounce back in Haldia after loss of BPCL volume in December as they moved to own terminal. Loss =15-20,000 per quarter. FY21 utilization was 50% and BPCL was 30% of that. This impacted Q4 and it will take few months to recover. But forecast of increased volumes in FY22 from HPCL and others. It will not fully offset but HPCL volumes can make up for 60-65%. Already seeing improvement in May. HPCL Panegarh is the largest bottling plant of Asia and operating at 50% capacity, 0.25 MT. More LPG will go there. Full utilization 2.5MT will happen in coming years.

-

Question from Enam: “In LPG business, We are building 9.6 to even further with one more terminal in South. We are at 3mn today and generating so much EBITDA so when can we utilize and go to 12mn? In next 5 years I will be shocked if you dont make 2000cr EBITDA. Liquid is already doing 200cr EBITDA/year and with expansion it will go to 300-350cr. In 5 years Liquid can hit 500cr EBITDA and gas can hit 1500-2000cr. When will you hit 150cr in gas division which is long overdue? There is no other company thats more beautifully placed to capitalize on the opportunity than Aegis but last 2 years have been surprising that things haven’t picked up. We are excited about gas stations AutoGas, commercial LPG, domestic LPG, Chota Sikandar. We are not aggressive here. You are talking of only 200 stations and not 500.”. Yes its overdue and life is not perfect. Some of it is due to COVID related delays. We are on the right path and more specific details in June updates on how we plan to ramp up the sales and utilizations. FY21 throughput was 2.91mn vs 3mn in last year. You call it conservative, we call it realistic. There are realities of how to ramp up retail distribution on the ground. It can take 3 years to build gas station because of permissions. You are right and we want to put up more efforts in retail- not only auto gas stations but also on dealers and bottling plants.

-

-

-

Major growth Strategy update for next 5 year incl capex plans will be announced in June. It will be one of the most significant announcement of our growth strategy for many years. This will be a transformational announcement to accelerate Aegis into the big league.

- Part of this will be a major push in the Liquids business. People will be surprised with the scale we have in mind.

-

WC gone down dramatically, is that one off that will normalize? Some of it is because of LPG price falling dramatically. Sourcing volumes have also come down.

Aegis FY21.pdf (2.2 MB)

9 Likes

June got over, wont hold the mgmt to that timeline, but mgmt seemed very confident to share the upcoming plans in June. Anyone has info, what could be the reason for the delay? I know they are conservative, but is something happening that could be concerning?

May be this is the news he was hinting at the Q4Fy21 concall.

Aegis Logistics and Royal Vopak of the Netherlands to form a major joint venture for LPG and chemical terminals in India

1 Like

Some info from Vopak website

Financial details

The enterprise value for Vopak’s shareholding in the joint ventures will amount to EUR 185 million plus EUR 15 million, depending on the fulfilment of certain CP’s. The project and Vopak equity IRR are expected to be double digits. Vopak and Aegis have arranged financing of EUR 153 million in the joint ventures. Taking into account this financing and the contribution of CRL, Vopak’s net consideration amounts to EUR 100 million plus EUR 15 million depending on the fulfilment of certain conditions.

In addition to the net consideration at closing of a total EUR 115 million (EUR 100 million plus EUR 15 million), Vopak and Aegis have agreed the payment of a minimum EUR 18 million and up to a maximum of EUR 40 million payable to Aegis via a financial instrument.

Revenues of the both joint ventures are forecasted to grow with a CAGR of around 6% in the first 5 years. LPG revenues will be about 75% of the total revenues of the joint venture. On the back of the forecasted revenue growth, the joint venture is expected to increase EBITDA in line with revenue growth towards 2026 driven by growth of LPG demand and imports of liquids chemicals in India. In addition, the joint venture has a pipeline of growth projects, both brownfield and greenfield.

Based on these EBITDA contributions, the implied EBITDA multiple of Vopak’s investment decreases from 11x in 2022 to 8x in 2026.

The ROCE, on the Royal Vopak level, is projected to come within the 10%-15% target range after 6 years, subject to growth developments.

This transaction will be marginally accretive to Vopak EPS in the first years.

Normal Purchase Price Allocation (PPA) accounting will apply, including recognition of goodwill as part of the carrying amount of the joint ventures. The consideration is to be measured at fair value at closing date. Any subsequent changes for the part of the consideration not yet settled, will be remeasured at fair value through profit or loss as an exceptional item until settled.

I guess the strategy update investor meet will happen in next few days now

8 Likes

The presentation on merger

1 Like

The con-call on the merger & what is on the table for Aegis

")

3 Likes

The link to the full report available on the internet, if anyone wants to read the full report, Aegis Logistics Ltd - Company Update (edelweiss.in)

3 Likes