Completely agree with you @omsingla!

We need to understand that the company is into retail business which primarily works on “brand” and it’s proposition.

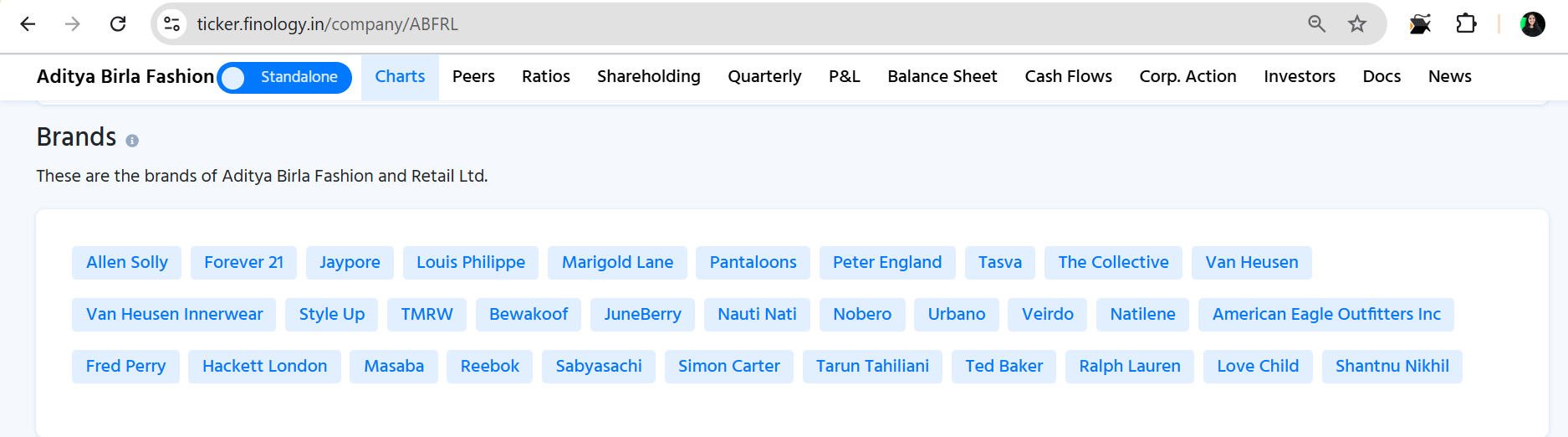

Abfrl acquired Madura (Vh, Pe, As etc.) in 2000 with the brands already clocking 325 crores with decently established brands as per those standards.

That portfolio has gone on to become ~ Rs.8k cr (including some additional segments like Reebok & VH innerwear) giving ~15% revenue CAGR.

Entering India’s fashion retail with owned brands at such an early stage, this growth is at best an abt average.

Also, the brands which at once point of time had a strong image, positioning also has also got diluted massively with brands crossing each other here & there in terms of positioning.

In retail, the brands & its positioning pulls crowd towards it, other things comes to consideration much later. (Case in point: Zudio, Westside, Ethnyx & even Abfrl’s very own Tasva).

This brands’ unique identity isn’t there. You dont know what to expect from which brand & the collection varies widely store to store. (Different for factory owned, SIS, FOCO, COCO, Multi brands)

Basically, the entire retail game in opposite direction.

This has been shown by AB group with other brands also.

(Pantaloon, ABCL - not a strong enough for such a long history group)

The same highlighted by the ken: Kumar Birla takes yet another shot at fixing his spotty record in retail - Trade Tricks by The Ken

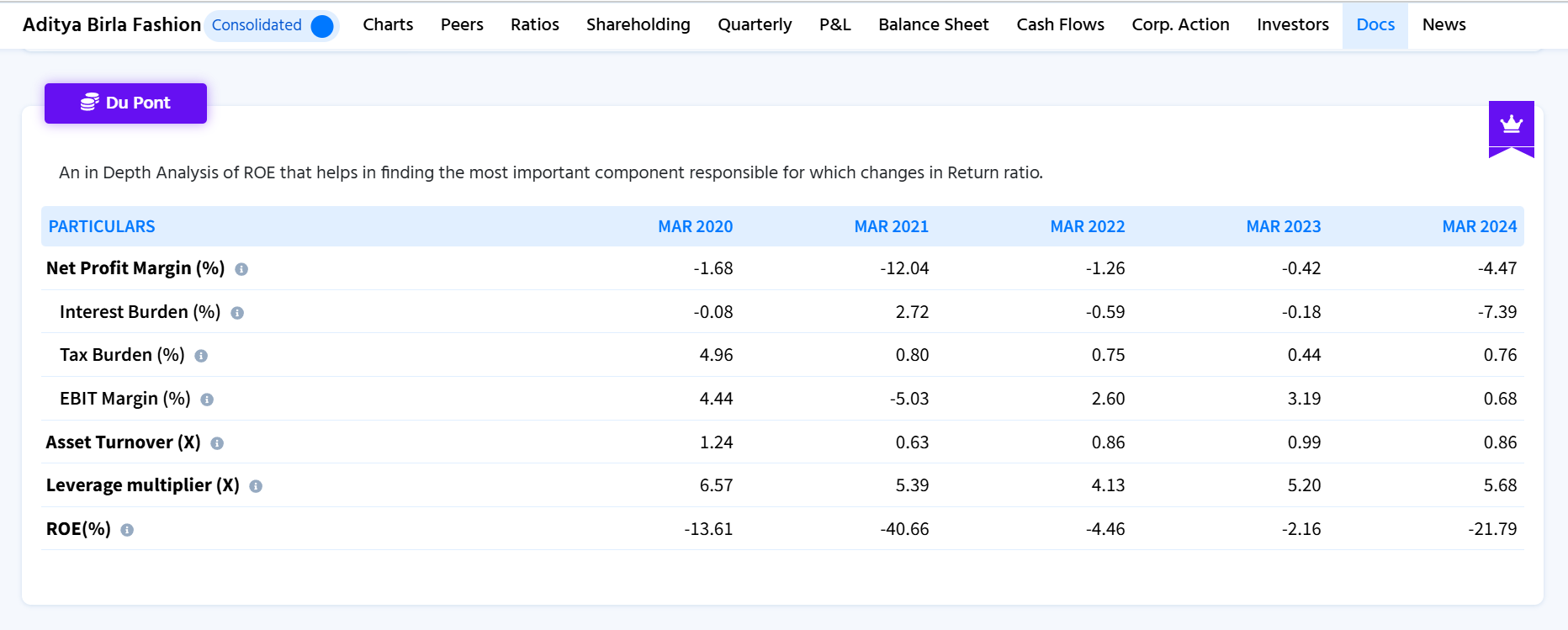

Add to this is relentless buying/starting of brands without focus on creating strong brands, the company needs to focus more on profitability than growing it. Rs. 16k cr is not a small number.

With new blood of Ananya & Aryaman on board, hopefully we see that change, finally.

Disclaimer: Invested at Rs.210