JM_Financial_Initiating_Coverage_on_Ami_Organics_with_29%_UPSIDE.pdf (2.7 MB)

3 Likes

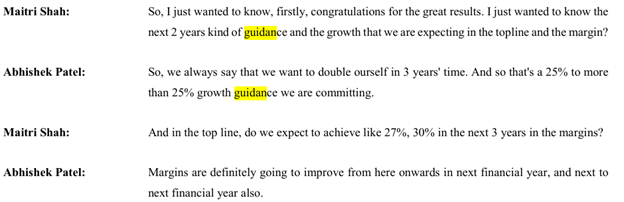

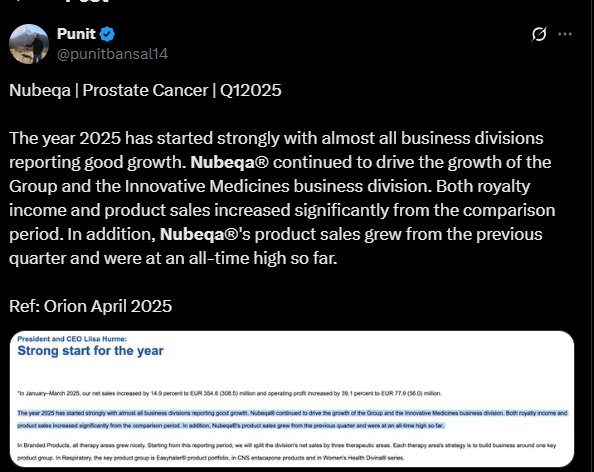

AMI Organics | Management Guidance

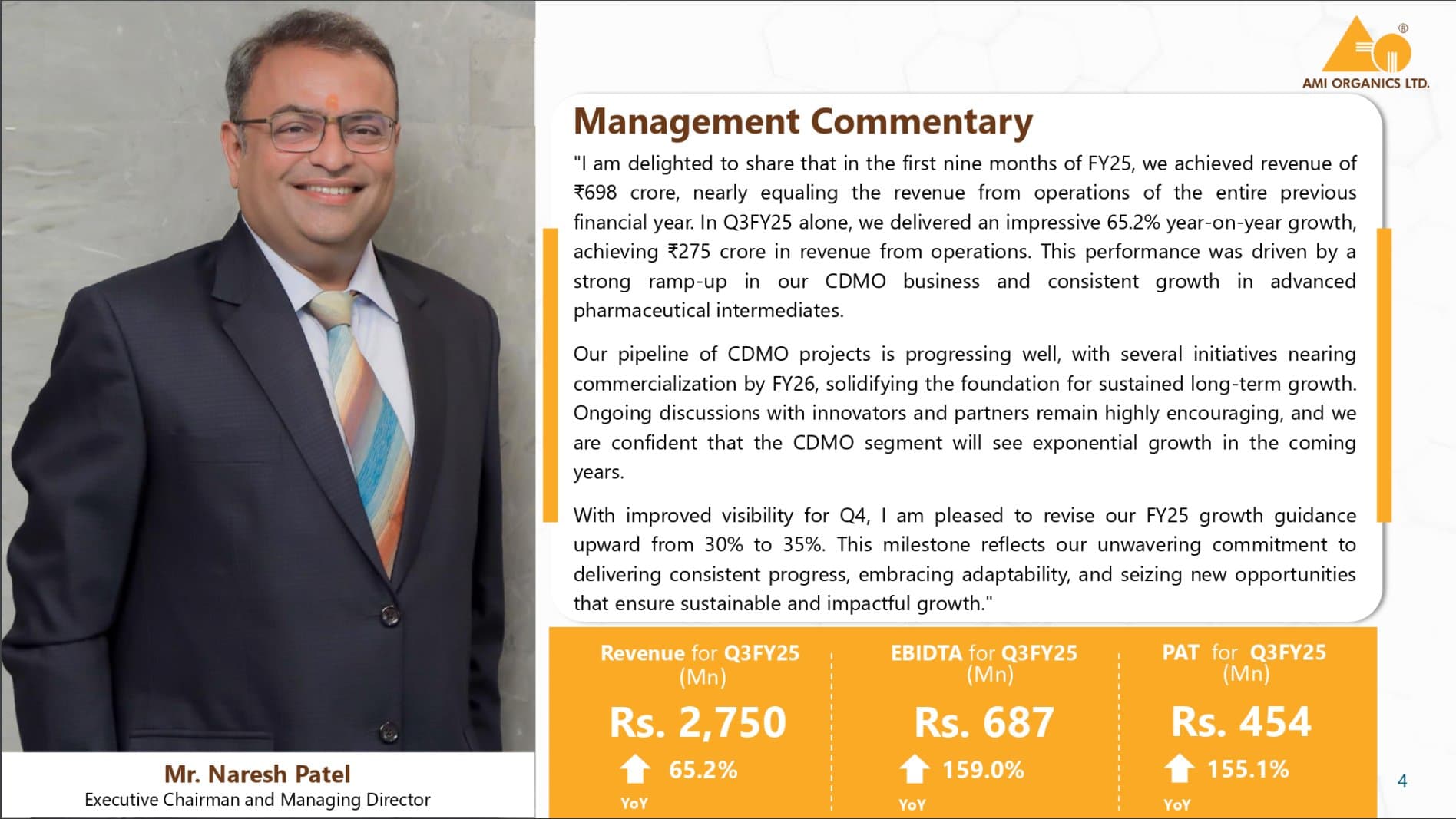

Results Update

Strong Growth in Q3FY25:

Revenue: ₹2,750 Mn (+65.2% YoY)

EBITDA: ₹687 Mn (+159% YoY)

PAT: ₹454 Mn (+155.1% YoY)

CDMO Business Expansion:

a. Significant ramp-up in the Contract Development & Manufacturing (CDMO) segment.

b. Several CDMO projects progressing toward commercialization by FY26.

c. Positive discussions with innovators & partners for future growth.

Revised FY25 Growth Guidance:

Growth guidance revised upward from 30% to 35% due to strong Q3 performance

9 Likes

This telegram channel.

2 Likes

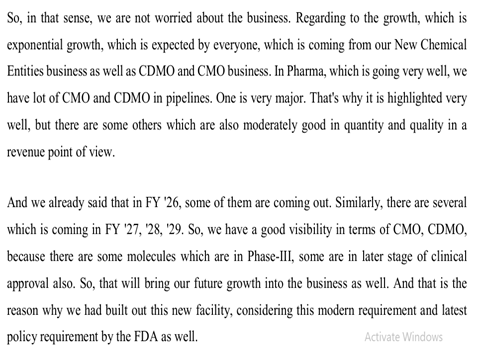

Guidance & Management Insights from Q3 Earnings Concall

- CDMO business to grow from INR 80–90 crore to 1,000 crore by FY28

- Growth guidance was revised upward from 30% to 35% for FY25

- EBITDA margins are expected to reach 27%-30% with operational leverage in upcoming years

- The company aims to double its size in the next three years

- FY26 is expected to have the highest-ever margin for Ami Organics

- Management is confident about business sustainability till 2040

- No plans to enter peptides, staying focused on synthetic chemistry

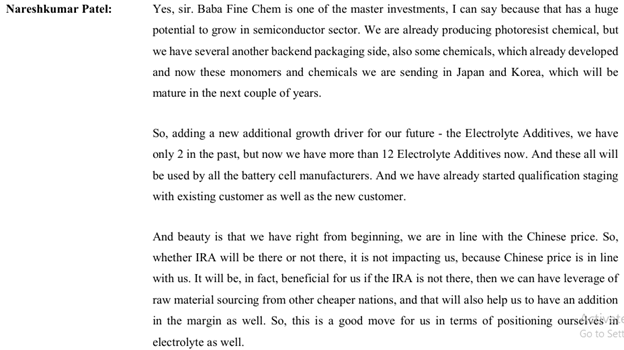

- Battery chemicals: 4,000 metric tons of all additives planned

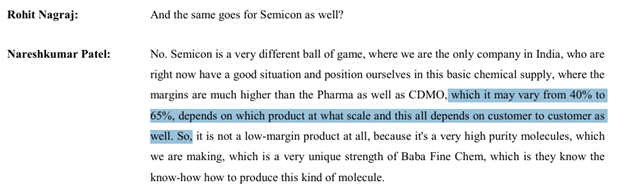

- Semiconductors: Focus on high-purity basic chemicals with margins ranging from 40%-65%

- Balanced growth strategy across Pharma, Agro, Specialty, Polymer, and Petrochemicals to reduce dependency on any single segment

Challenges & Headwinds

- Specialty Chemicals: Highly commoditized, pricing pressures, and raw material fluctuations

- Battery Chemicals: Geopolitical uncertainties affecting ramp-up

- Deferred orders in commodity chemicals (cosmetics and parabens)

5 Likes

I am new to the community and hence in learning mode.

Q3FY25 Con call:

Response wrt long term visibility:

Response wrt Baba Fine, Electrolyte and Chinese Competition:

Another wrt Semi-Conductor:

Wrt Guidance and Margin for next 3 years:

I believe if management shall be able to deliver what they promise then share should give good return here onwards. However valuations have already priced in above factors. Hence any fresh entry will lead to high risk for high reward.

I am invested in the stock and hence may have biased view.

2 Likes

As per Incred Equities research report of March-25, Earnings growth of AMI Organics will taper down and the valuation is too high.

• Ami Organics’ FY25F EPS growth is primarily driven by 100% growth in Nubeqa sales, which, in Bayer’s own admission, will taper to 15-20% in CY25F.

• While there is optimism about Nubeqa’s sales, high treatment costs and limited growth potential in developing markets are areas of concern.

5 Likes

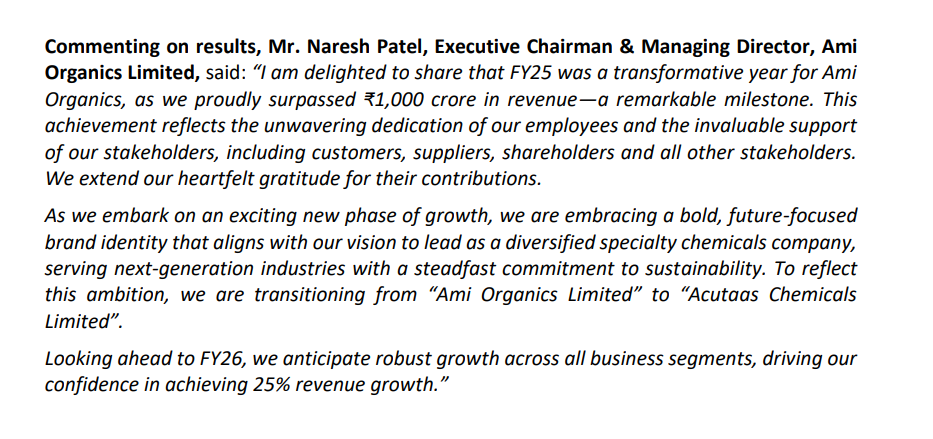

Company going change their name now new name is acutaas chemical ltd

b03ba366-8277-4c92-b1f8-f2c3a2e63fda.pdf (386.9 KB)

2 Likes

Going through Ami’s conference call, the management recently stated this about their CDMO segment: “We anticipate our overall CDMO business to reach approximately 1000 Cr by FY28 compared to 80-90 Cr in the last FY.” This interested me and i wanted to dig deeper.

Broadly, the sales of the company are split between

-

Pharma intermediate - 80% of sales

-

Specialty chemical - 20% of sales

CDMO vertical falls under the Pharma intermediates. AMI organics wants to be only in the intermediates space and not move in to API segment per the mgmt.

They are investing in the Ankaleshwar facility, which currently has a capacity of approximately 450KL and three units. One of the Units (number 2) is dedicated completely to Fermion alone. Fermion is a subsidiary of Orion Pharma (Finland).

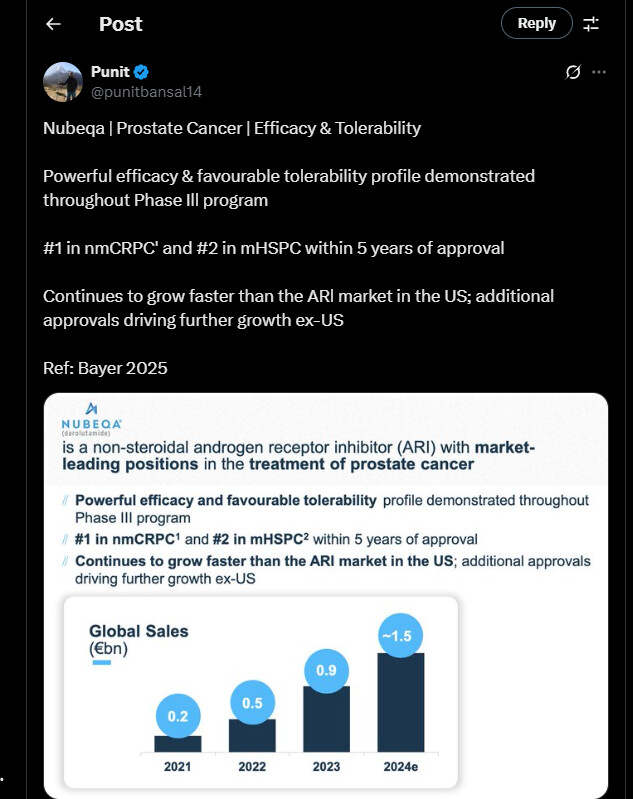

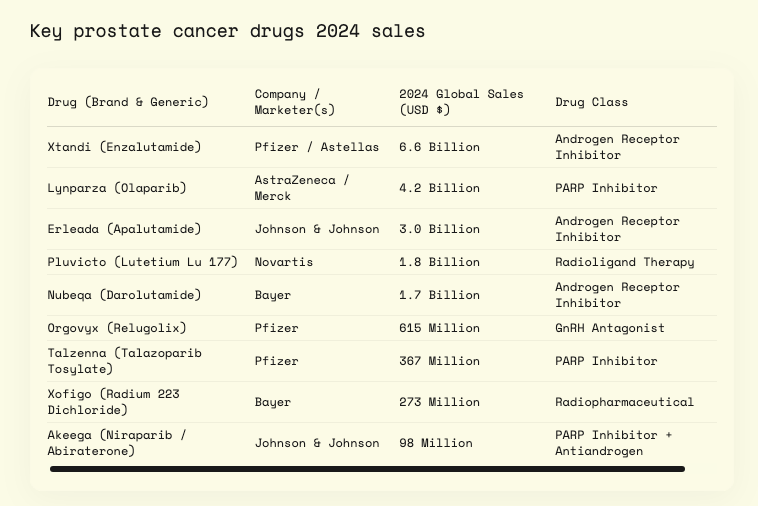

Ami is currently supplying 5 intermediates for the molecule Darolutamide. Bayer is selling NUBEQA as the end product to patients/customers.

This was a collaborative effort by Bharani @phreakv6, Nirvana @nirvana_laha, and me to determine whether the molecule Darolutamide, marketed by Bayer as Nubeqa, will be a meaningful driver for Ami Organics.

From Bayer’s conference call, the co-innovator has tagged the molecule Nubeqa as a blockbuster drug.

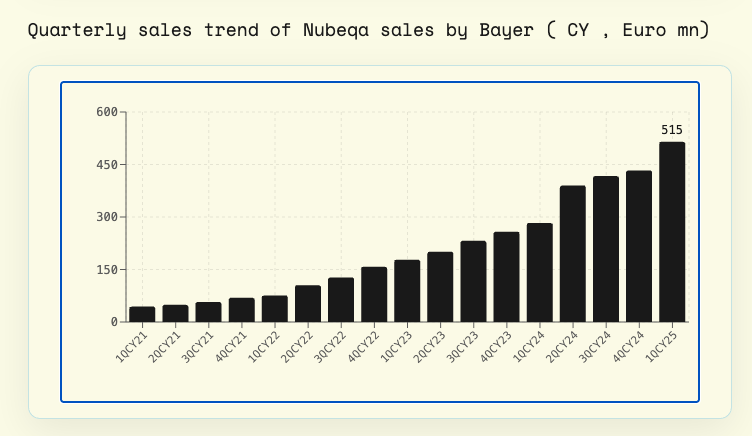

- They had touched €1.1 billion by 9 months of CY24.

- For the entire CY24, their sales was €1,523 billion.

Q2CY24

Q3CY24

Based on the EC filing, lets look at what are the steps involved in leading up to the final API, Darolutamide, is made ( as far as the EC docs go and there is some educated guess up until the final API):

Now let’s look at the intermediate molecules

| Intermediate | Molecule name |

|---|---|

| DARO-II | 5-acetyl-1H-pyrazole-3-carboxylic acid |

| DARO-III | (2-chloro-4-(1H-pyrazole-3yl) benzonitrile (DARO-III) |

| DARO-IV | Tert-Butyl((1S)-2-hydroxy-1- methylethyl)carbamate (DARO-IV) |

| DARO-V | S) - 4(1-(2- AMINOPROPYL) -1H-PYRAZOL-3- YL) -2-CHLOROBENZONITRILE |

Daro II:

There is no explicit callout of Daro I in the filing document; we assume it is Methyl-5-Acetyl—1H-Pyrazole-3-Carboxylate(M5AP3C) which is the key raw material for making Daro II. They did not have the capacity for this before the filing, and they have proposed to make 10MT per month (thus, 120 MT per year)

20 Kgs of M5AP3C gives an output of 78 Kgs of Daro II

Daro III:

The route of synthesis for Daro III is a two stage process as shown below:

Based on these reactions:

70 kgs of raw material [1-(tetrahydro-2H-pyran-2- yl)-5-(4,4,5,5-tetramethyl- 1,3,2-dioxaborolan-2-yl)-1H- pyrazole] for this step produces 95 kgs of Daro III.

Daro IV:

100kgs of 2-Amino Propanol and 272 kgs of Di-BOC which are the raw materials produce 100 kgs of Daro IV

Daro V:

Daro III and IV are both needed to make Daro V. 110 kgs of Daro III and 239 kgs of Daro IV along with a few other raw materials- are need to produce 402 kgs of Daro V.

The capacities they have proposed to add for this process are:

Intermediate Molecule name Capacity (MT/Month) Capacity

(MTPA)

DARO-II 5-acetyl-1H-pyrazole-3-carboxylic acid 10 120

DARO-III (2-chloro-4-(1H-pyrazole-3yl) benzonitrile (DARO-III) 10 120

DARO-IV Tert-Butyl((1S)-2-hydroxy-1- methylethyl)carbamate (DARO-IV) 10 120

DARO-V S) - 4(1-(2- AMINOPROPYL) -1H-PYRAZOL-3- YL) -2-CHLOROBENZONITRILE 10 120

The sales number for Nubeqa, as reported by Bayer is:

Now, moving on to the economics:

The daily dosage is 1200 mg/day (2x300 mg tablets - twice a day)

Link: https://www.accessdata.fda.gov/drugsatfda_docs/label/2022/212099s002lbl.pdf

- So this implies it’s 36,000 mg/month (1200x30)

- As per online sources, Nubeqa’s cost is approximately. $14,890 for 30 days of supplies (4 tablets a day x 30 days in a month = 120 tablets)

- So, cost per patient per year = 12 x 14890 =~ $178,500

- How many patients are eligible for the currently approved labels? ( not considering the in-process, to-be-approved label expansions) = 200k-300k. So, let’s take an average of 250k patients.

- And how many gms/day is each patient consuming in a year?

- 1200 x 365 = 438,000mg/year = 438 gm/yr

- So, 1 MT capacity of API should cater to how many patients?

- 1000,000gms/438 =~ 2250 patients

- Assuming a conversion ratio of 1.5:1 for the Daro V intermediate to the final API = 2250/1.5 = 1500 patients.

- So 1500 patients can be catered to, with 1 MT of Daro V. To cater to 250k patients on average, how many MT Of Daro V are needed? = ~ 160-170 MT.

Ami Organics, as per the EC document, has 100 MT capacity currently. This roughly means Ami’s capacity can cater to 60% of the demand.

Looking at it from the reported sales number of Bayer perspective and reverse engineering a bit, their 4th quarter sales figure was 443 million Euros, which approx to 478 million USD.

- Using the same numbers as above, $14890/month of supply of Nubeqa/patient. Per quarter (3 months), the sales cost is ~$44,500/patient.

- We need to take this number with a pinch of salt as the final price that Bayer gets might differ after rebates, discounts with the PBM (pharmacy benefits managers). Also, the supply chain will have its margins. Assuming the supply chain has 20% margins for simplicity’s sake - Bayer receives 80% of the revenue. $44,500 X 80% = $35,750

- This would approx. give us $478M /$35,750 = 13,400 patients.

- Also, the reported sales number is for global sales, and the US might be all but a portion of this 443 million euros. Assuming the US share is 50%, since the prices are highest in the US relative to the remaining 86 countries for which Nubeqa is approved. So, assuming 50% of sales = $239M/$35,750 ~= 6,700 patients. [Please note that only regulated markets can fetch higher prices; other countries have reduced selling prices.]

As of now per reports - NUBEQA is now the fastest growing androgen receptor inhibitor in the U.S., with nearly 45,000 patients in the U.S. and 100,000 patients globally treated as of the end of 2024.(link & link) This is well on the way to the 250k-300k patients addressable market & beyond. They are in the process of submissions for the 3rd indication in US, EU and China. If they get approval in China, that also would unlock additional patients and a major market.

Few points to note:

- Bayer’s sales numbers might also include inventory stocking and not just filling prescriptions (patient count - inflated)

- There are several assumptions/ approximations I have used in the above calculations. If the Daro V to Daro final API ratio of 1.5:1 is different, say 1.25:1, 1.3:1, or 1.1:1 - the MT needed to manufacture will be lower (~140 MT for 1.25:1, 145 MT for 1.3:1, etc.).

- Real-world efficiency might be very different from theoretical efficiencies used above. As stated above, a lower ratio can reduce the demand estimates.

- The 20% supply chain margins can be very different. Bayer’s net sales per patient can be lower if the margins are higher - 30%, 35%, or 40%.

Disclaimer:

Ganesh - invested (tracking position)

Nirvana - not invested

Bharani - not invested

27 Likes

Excellent result from Ami, Overall 37% growth in Top line yearly qtrly basis and138% growth in profit y-o-y .qtrly .will be waiting for mgmt commtary…my objective will be ignore noise, pharma being a very complex subject and listen only to mgmt comments…now onwards..folllowing the mgmt who spent millions in capex in last 2-3 yrs..

25% Revenue growth guidance now..last year, they gave the same number after Q4 2024, then upgraded it, after Q2 2025…

8 Likes

Further to add, Ami mentioned in concall, Margin in FY 26 will ‘definitely’ improve from here,

in H1 , 40% and H2 60% revenue will come..

7 Likes

Fabulous end to the year.

Some points captured from the Q4 FY25 concall yesterday. Usual disclaimers E & OE apply.

-

Guidance of 25 % revenue growth and margin improvement

-

H1 accounts for 40 % of the topline and H2 60 %. Margin also varies accordingly

-

In Q4, Gross margin improved due to better product mix and EBIDTA margin improved due to expansion in GM and operating leverage

-

Pharma CDMO - Rs.1000 crore revenue by FY28 expected. Have a strong pipeline

-

BFC - Expanding into Taiwan, Korea, Japan. Will ramp up in the next 1 or 2 years. Samples are going to customers, approvals in progress.

-

Ankleshwar facility Block 1 - Marquee CDMO. Block 2 - Fungible multipurpose facility Block 3 – Dedicated to marquee customer

-

Margins for FY25 - Advanced Intermediates - 24.5 % Spec Chem 14.7 %, Average - 23 %

-

Sachin Pilot Plant - Will help scale up R&D products. This expansion required since existing pilot plant is not enough. We are also getting into High Potent molecules (which requires special facilities, I think)

-

New CDMO contracts - On track. Qualification stage going on. Revenue will come in H2 FY26

-

CDMO sales for FY25 - we are not disclosing.

-

FY26 - Rs.200 crores capex - Spillover capex Rs.130 crore for Electrolytes + Maintenance Capex, Pilot Plant capex is Rs.70

-

Savings from solar power plant - when 16MW is completed, we will get Rs.16-18 crore p.a. savings. Currently 11 MW is completed

-

Spec Chem - growth is slow due to BFC. Rest has grown 27 % (I think this is the number mentioned, but need to check)

-

No new debt expected for next 1 year at least

-

CDMO - we have visibility of pricing also since pricing is fixed in the signed contracts

-

Pharma generic business is also growing well; RM prices & output prices are both stable currently

-

We don’t have any direct sales to US

-

We have no idea whether current revenue include any inventory build-up at customer’s end which may impact future sales

-

Capacity Utilization for Spec Chem is 60 %

-

Margins for Spec Chem (electrolytes & semiconductor) business will be at current levels only

-

Rs.300 crore investment in electrolyte salts announced earlier - no change in status. No movement on that issue

-

Electrolyte additives - 2000 MTPA going commercial this year in H2 FY26. Will reach full utilization in 3 years

One additional observation of my own (not discussed in the call):

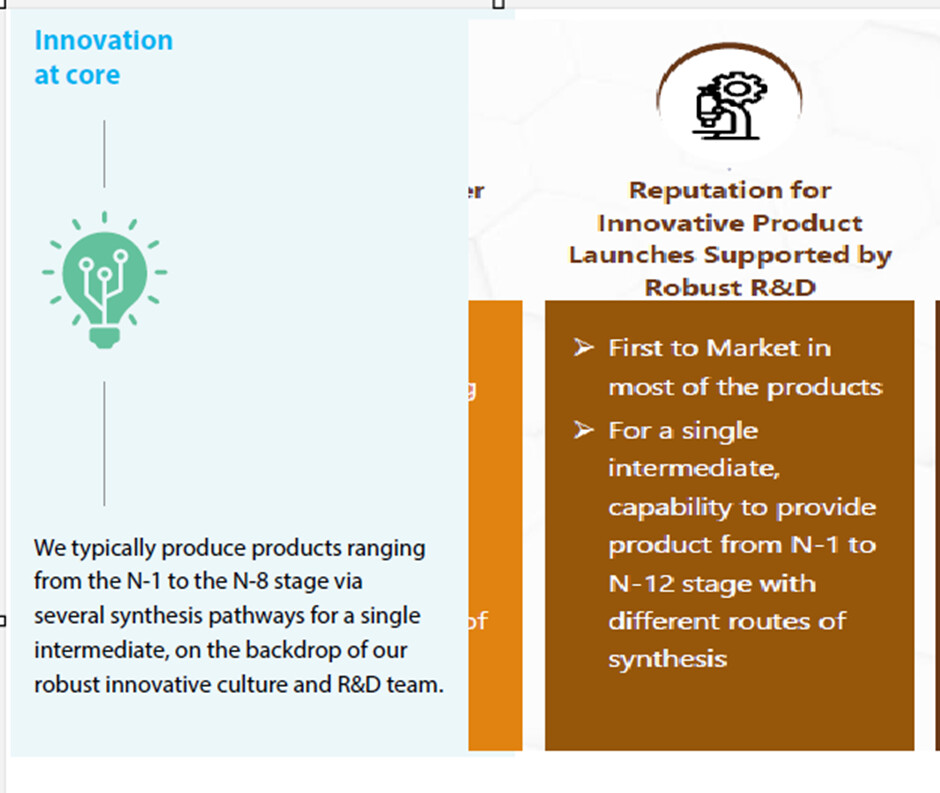

In the past (e.g. FY22 AR), Ami used to mention ‘capabilities to execute products from N-1 to N-8 stage’ but sometime last year, Ami has moved beyond. The presentations now mention ‘N-1 to N-12 stage’ which is a significant enhancement of capabilities from N-8.

(FY22 Annual Report (left) Vs. FY25 presentation (right))

This progression represents a significant advancement in the company’s capability, since each additional step introduces exponentially greater complexity across multiple dimensions, such as reaction expertise, purification techniques, documentation, impurity management etc. It also allows companies to capture a larger share of the product value chain, create their own IP etc. thereby yielding higher margins. This is particularly significant as the industry is moving toward increasingly complex molecules. Research reveals that the average synthesis for drug candidates required 8 steps in 2006, but by 2017 it had increased more than 20 with some complex candidates requiring as many as 92 steps (for the final API)!

I am not a technical person, so I asked AI (after a series of prior questions not given here) what level of sophistication does a N-12 level of capability indicate, and where would it rate it on a scale of 1 to 10 where 1 is the lowest and 10 is the highest level of sophistication achieved by a pharmaceutical / chemical manufacturer. It answered 7 – 8. Here is detailed answer for those who are interested. Those with a technical background are welcome to comment.

N-12 Capability.pdf (312.4 KB)

(Disc.: Invested)

29 Likes

Kotak Mahindra MF acquires 6.6% stake in Ami organics for Rs 301 crore.

Ami Organics promoters Vaghasia Chetankumar Chhaganlal and Nareshkumar Ramjibhai Patel divested the same number of shares at the same price on the NSE.

After the stake sale, the combined holding of promoters and promoter group in Ami Organics has declined to 29.36 per cent from 35.96 per cent.

1 Like

I’ve compiled everything I know about the company into this PDF. It might be helpful for new investors. Please let me know if any corrections are needed. Also took the help of ChatGPT.

Ami Organics.pdf (1.5 MB)

17 Likes

Does Ami Organics deserve to trade at such premium valuation versus other NCE suppliers or Pharma players? Whats the differentiationg factor vs big names like Laurus or Neuland which makes Ami special or is it different from them in comparison?

2 Likes

It seems the company name has been changed to Acutaas Chemicals?

3 Likes

Changed the name of the thread to [Acutaas Chemicals (formerly Ami Organics) - Pharma Intermediates & Specialty Chemicals] from the earlier Ami Organics - Pharma Intermediates & Specialty Chemicals to reflect the current name

2 Likes

Over the past few weeks, i spent time researching various pharma cdmo players, what caught my eye about acutaas was management’s guidance regarding its cdmo business . below are my notes about the company -

disclaimer - no reco / have no position in company either

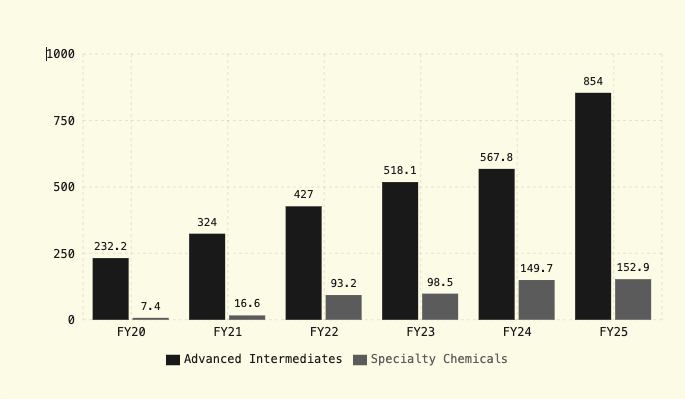

Acutaas Chemicals (formerly Ami Organics) is a fast-growing manufacturer of pharmaceutical intermediates and specialty chemicals. The company is experiencing rapid growth driven primarily by its pharma CDMO business, as well as the ramp up of its specialty chemicals segment, which includes electrolyte additives and semiconductor chemicals.

Acutaas’s business can be categorised into two broad categories: Pharma Intermediates (85% of FY25 revenues) and Specialty Chemicals (15%). Company’s portfolio comprises 610+ products and has a diversified customer base of about 600 customers across 55 countries.

Management aims for 25% annual sales growth and targets revenues of ~₹1000cr by FY28 in its pharma cdmo division. The strongest near term growth trigger for Acutaas will be its pharma CDMO contract with Fermion to supply intermediates for darolutamide - a fast growing, blockbuster patented drug for prostate cancer.

Business Segments

Revenue Mix by Segment (cr)

Advanced pharma intermediates accounted for 85% of company’s overall revenues in FY2025. The Company develops, manufactures and commercialises intermediates used for manufacturing API and NCE in India and overseas markets in therapeutic areas such as anti-retroviral, anti-inflammatory, anti-psychotic, anti-cancer. Since inception, it has created over 550 pharmaceutical intermediates in 17 different therapeutic areas, which are supplied to over 160 customers. Acutaas has positioned itself as a supplier capable of handling multiple chemistries such as nitration, diazotization, oxidation, esterification, ammoxidation, etc and is highly backward integrated as far as possible for most of its intermediates. As a result company has been able to gain a dominant market share in many of its products.

As of FY24 company’s pharma intermediate business consists of 10% from CDMO, 40% from innovator and 50% from generic pharma intermediates. About 95 % of the portfolio targets fast growing chronic therapy (anticancer, antiviral, CNS and cardiovascular segments) and company is usually first to market with different routes of synthesis and capabilties to supply intermediates from n-1 to n-12 stages . Once a intermediate supplier becomes a registered source in customer’s DMF , there is an entry barrier against new entrants. This becomes a source of moat and leads to limited competition and high market share in chosen molecules.

Acutaas has built strong relationships with important customers like Fermion for which it started supplying intermediates since 2010. Company holds 15 process patents to its name and also adopted newer technologies such as flow chemistry and distributed control systems to make its production processes more efficient and competitive.

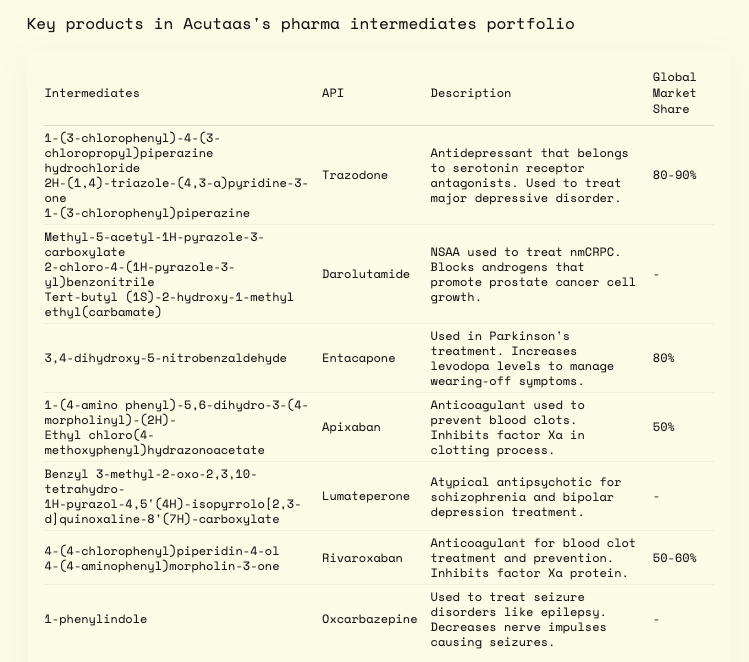

key growth drivers in non CDMO business

Apixaban: Apixaban (innovator brand name Eliquis) is an anticoagulant medication used to treat and prevent blood clots and to prevent stroke in people with non-valvular atrial fibrillation. The global market size of the drug is close to US$20 bn, although this will likely decrease after its patent expires in 2026. There are more than 70 manufacturers of the API. AOL has a sizeable market share for two intermediates used to produce the API: 1(4-aminophenyl)-3-morpholin-4-yl-5,6-dihydropyridine-2(1H)-one and ethylchloro [(4- methoxyphenyl) hydrazono] acetate. AOL has already established a healthy pipeline of 25-30 customers for the post-patent era.

Lumateperone tosylate: Lumateperone (innovator brand name Caplyta) is a medication used to manage and treat schizophrenia and other neuropsychiatric disorders. Its patent expiry is 2029. AOL holds a process patent for one of its intermediates: benzyl, 3-methyl-2-oxo-2,3,9,10-tetrahydro-1H-pyrido[3’,4’:4,5]pyrrolo[1,2,3-de]-quinoxaline-8(7H)-carboxylate.

Rivaroxaban: Rivaroxaban (innovator brand name Xarelto) is an anticoagulant medication used to treat and prevent blood clots. The drug was initially developed by Bayer and marketed by Johnson & Johnson. Its patents are expiring by 2026, and AOL will look to supply four intermediates to generics suppliers.

Trazodone: Trazodone is the largest API in terms of revenues for the company and has been contributing 100cr+ of revenues for the past 2-3 years. AOL offers three intermediates used to make this API and claims to hold a dominant market share (80-90% in FY2021) in these.

CDMO business : key growth driver

In it’s cdmo business Acutaas undertakes contract manufacturing for pharma companies under long term supply contracts. Company has commenced a 10 year contract with Fermion Oy of Finland to supply intermediates for darolutamide ( brand name nubeqa which has become a blockbuster for Bayer). This contract will be a major growth driver for Acutaas in coming years . Acutaas is currently supplying 5 intermediates for the molecule Darolutamide. Bayer is selling NUBEQA as the end product to patients/customers. Acutaas is also working on several new CDMO contracts with other pharma innovators with multiple projects in pipeline to be commercialized by FY26.

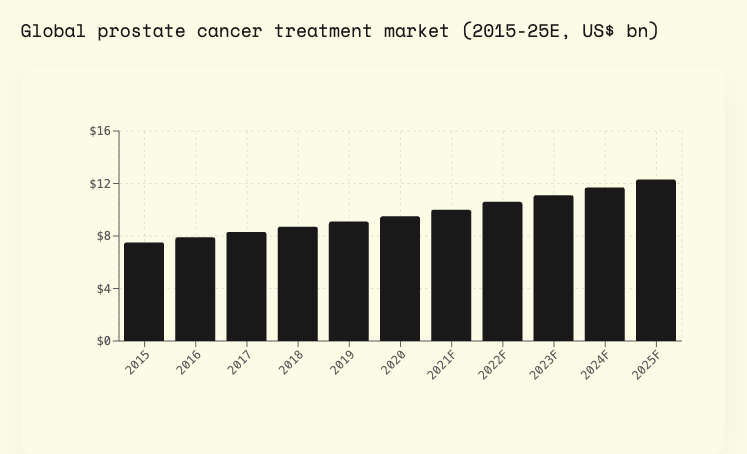

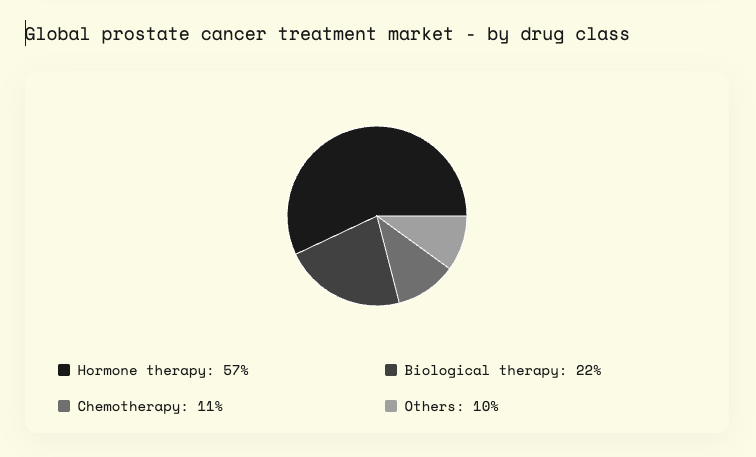

Prostate Cancer Treatment Market

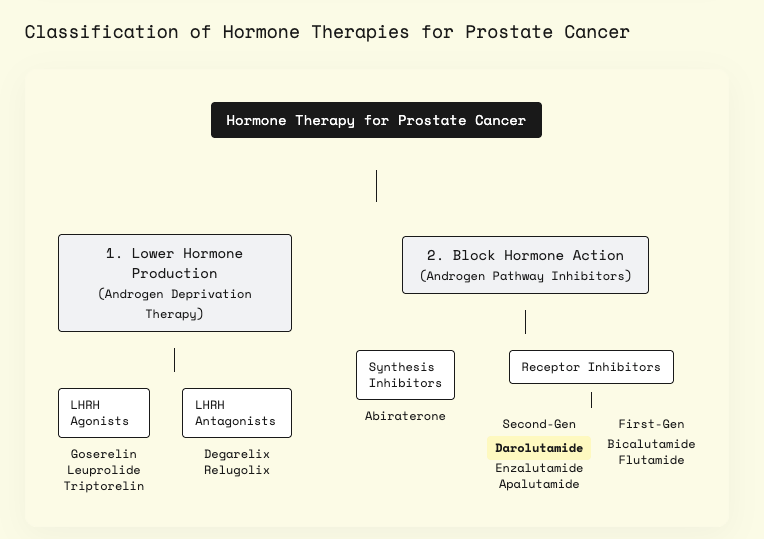

Prostate cancer is a general term used for diseased condition in which abnormal cells grow and invade in uncontrolled manner in the prostate. Prostate cancer inhibits production of male sex hormones (i.e. androgens) and ultimately blocks the action of androgen.

Antiandrogen drugs are medications that block androgens (male sex hormones) from binding with the androgen receptors that exist in prostate cancer cells. In its early stages, prostate cancer cells rely on androgens to feed their growth. By blocking the coupling of androgens with cancer cells, antiandrogens starve the cancer cells of the androgens they need to grow. However, anti-androgens don’t stop androgen production. Medical professionals often combine anti-androgens with other treatments, such as surgical or chemical castration.

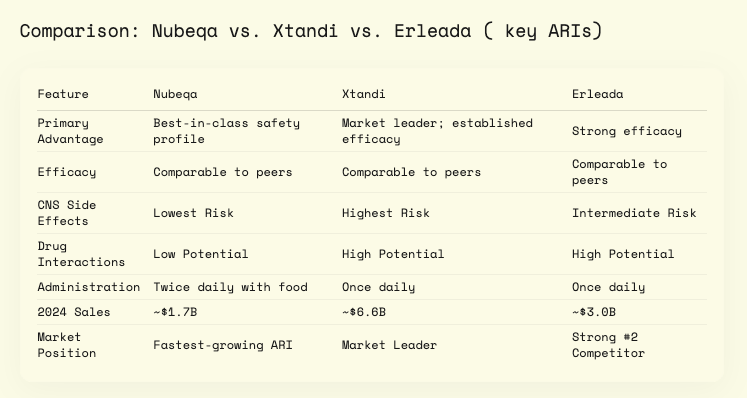

First-generation ARIs, like Bicalutamide, are the original, weaker drugs that partially block the androgen receptor. Second-generation ARIs (Nubeqa, Xtandi) are the modern standard, providing a much more potent and complete blockade of the receptor for a superior clinical effect.

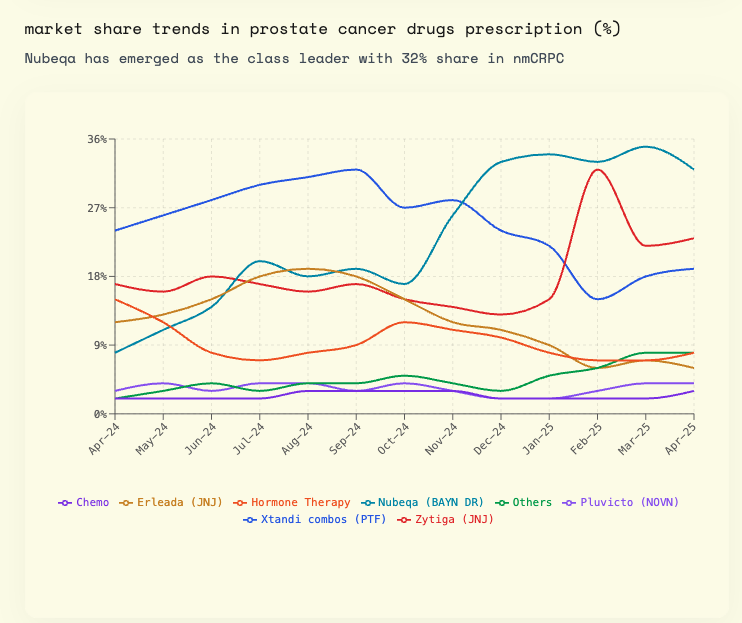

Across the prostate cancer space, older androgen receptor inhibitors command the highest share. With newer ARi assets Erleada and Nubeqa , despite being third to market, Nubeqa now leads Erleada in every setting , suggesting physician preference for Nubeqa which could be due to the benign safety profile of the drug with similar/ if not better efficacy.

About Darolutamide

Darolutamide (marketed by Bayer under the brand name Nubeqa) is a drug to combat prostate cancer. It was initially approved in 2019 to treat non-metastatic castration-resistant prostate cancer (nmCRPC), but subsequently in August 2022 also approved by the USFDA in fighting metastatic (i.e., cancer cells that are spreading to other parts of the body) castration-sensitive prostate cancer (mCSPC) in combination with docetaxel. Darolutamide was developed jointly by Bayer and Orion Pharma. Fermion (a fully-owned subsidiary of Orion) manufactures the darolutamide API, while Orion manufactures the formulations and Bayer holds the marketing and distribution rights.

Fermion manufactures the darolutamide API, upon which Orion manufactures the formulations and sells to Bayer at COGS; in exchange, Fermion/Orion receive a combination of royalties and milestone payments. The average annual royalty rate is currently above 20% including product sales to bayer. As the global sales increase, annual royalty rates will increase. If annual sales for darolutamide hits EUR 3 billion, Orion’s royalty rate will increase above 25%.

Efficacy of darolutamide versus peer drugs

Studies have shown that darolutamide offers certain advantages over other prostate cancer treatments, particularly in terms of efficacy and safety.

Minimal Blood-Brain Barrier Penetration: Its low penetration of the blood-brain barrier reduces central nervous system-related adverse events such as seizures, fatigue, dizziness, and mental impairment, making it better tolerated compared to other androgen receptor inhibitors.

Efficacy in Prolonging Metastasis-Free Survival: Clinical trials such as ARAMIS demonstrated that darolutamide significantly prolongs metastasis-free survival in men with nonmetastatic castration-resistant prostate cancer, with a median metastasis-free survival of 40.4 months compared to 18.4 months with placebo.

Overall Survival Benefit: Darolutamide significantly reduces the risk of death by approximately 31% compared to placebo.

Favorable Safety Profile: Darolutamide is associated with a low incidence of adverse events, with rates similar to placebo for many side effects including fatigue, falls, fractures, seizures, cognitive disorders, and hypertension.

Better Tolerability: Indirect comparisons suggest darolutamide has a more favorable tolerability profile than apalutamide and enzalutamide, with fewer treatment-emergent adverse events like falls, fractures, rash, fatigue, and mental impairment.

Looking ahead, Orion is conducting two significant clinical trials for darolutamide, named DASL‑HiCaP and ARASTEP.

ARASTEP (phase III, PSMA‑positive biochemical recurrence) - evaluates darolutamide + ADT in men whose PSA is rising after local therapy but before overt metastasis; success could shift Nubeqa into the early‑recurrence setting and extend therapy duration per patient.

DASL‑HiCaP (phase III, adjuvant high‑risk localized PCa) - tests darolutamide as part of adjuvant ADT after surgery or radiotherapy in very‑high‑risk local disease; a positive read‑out would move the drug even earlier in the treatment cascade, opening an entirely new adjuvant market.

Speciality Chemicals

Acutaas began to strategically diversify beyond advanced pharma intermediate in 2021, when it acquired two manufacturing sites (Ankleshwar and Jhagadia) from Gujarat Organics. In 2023, company acquired a 51% stake in Baba Fine Chemicals entering the niche of high-purity semiconductor chemicals. Company also has forayed into electrolyte additives where it will initially start with manufacturing Vinylene carbonate and fluoroethylene carbonate.

Electrolyte additives business

Acutaas has forayed into battery chemicals by setting up production capacities for electrolyte additives under a wholly owned subsidiary named ami organics electronics private limited . Company will have 2000kpta capacity each for vinylene carbonate and fluoroethylene carbonate and expects commissioning of plant by end of h1 fy26 and supplies starting from h2 of fy26. Acutaas has obtained an order from an OEM of a battery cell manufacturer which will take half of acutaas’s capacity. These additives are used in small doses within Li-ion battery electrolyte formulations to dramatically improve cell life, safety, and performance.

Acutaas will be the first global manufacturer outside China to develop electrolyte additives (vinylene carbonate and fluoroethylene carbonate) for lithium‑ion batteries; initial capacity of 2,000 MT each and a pipeline of 9+ additives under development. Company has also Signed an MOU with the Gujarat Government for about INR 300cr investment to set up an electrolytes facility. These additives are used in the preparation of electrolyte formulation of Li-ion batteries.

Gujarat Organics business

Acutaas acquired 2 sites at Ankleshwar and Jhagadia from Gujarat Organics in 2021 . Under this business Acutaas manufactures and supplies speciality chemicals and preservatives - including paraben and paraben formulations , methyl salicylate and range of other speciality chemicals used in personal care , pharmaceuticals and agrochemical industries. However, this line of business is largely commoditized with modest margins. Rationale for this acquisition per Acutaas’s management was to bag the manufacturing sites . Company does not have any major capex plans in this business and the unutilized land has been converted into a pharma cdmo unit.

Semiconductor Chemicals via Baba fine chemicals

This Segment Includes high‑purity semiconductor chemicals via the Baba Fine Chemicals unit and Acutaas is the only manufacturer in India producing photoresist chemicals domestically. These chemicals are used in semiconductor fabrication in materials for photolithography such as photoresists, anti-reflective coatings, and photo acid generators, as well as precious-metal-based conductive inks (silver, copper, gold, platinum inks) for chip and PCB manufacturing.

Company acquired a majority stake in Baba Fine Chemicals in 2023. BFC was founded by three scientists in 2002 , Before the acquisition by Acutaas , BFC was focused only on 1 single customer - Heraeus Epurio - a German company with operations worldwide . Volumes supplied had been very small and so business was very small at time of acquistion with revenues at 40cr in fy23 with ebitda margins of 65-70%.

Post acquisition, BFC revenues declined in fy24 and fy25 due to supply disruptions with demand weakness in semiconductor industry. Acutaas is actively in discussions with prominent semiconductor materials buyers in korea and japan and expects new orders to materialize by FY26 from these engagements , alongside a potential rebound from the original customer as the chip cycle improves. Furthermore, India’s push to establish a domestic semiconductor ecosystem (e.g. new ATMP/OSAT facilities by Micron, government incentives for chip fabs) could create local demand for photoresist and ancillary chemicals in the coming years.

Management guides that the semiconductor chemicals business could scale 2–3x its current sales over the next 2-3 years and it is relatively higher margin business ; so margins for the company will expand as this line of business expands.

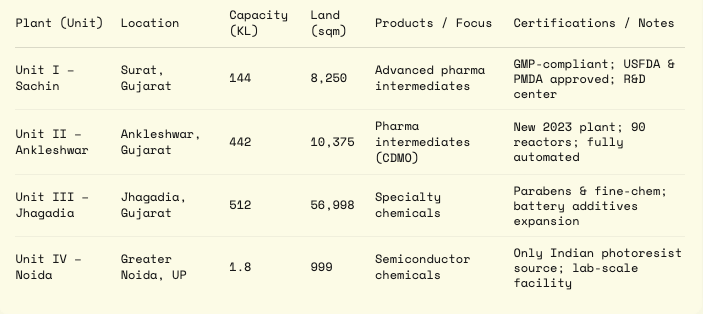

Manufacturing Facilities

Acutaas operates four manufacturing units in India, each supporting different segments of its business. Unit I - Sachin (Surat, Gujarat) is the flagship plant for advanced pharmaceutical intermediates. This facility has an installed reactor capacity of ~144 KL (with 13 production lines and 40 reactors) and is fully cGMP-compliant. Unit I also houses the main R&D center for the company, and it currently operates at around 70–80% capacity utilization.

Unit II – Ankleshwar (Gujarat) was inaugurated in December 2023. The company had acquired an older Ankleshwar facility in 2021 as part of the Gujarat Organics acquisition, but that aging unit was demolished and replaced with this state-of-the-art brownfield plant. The new Ankleshwar unit is spread over ~10,375 m^2 and is equipped with ~90 reactors (~436–442 KL total capacity) along with modern automation (DCS and powder transfer systems). It is designed to cater pharma intermediates and CDMO contracts.

Unit III – Jhagadia (Gujarat) is focused on specialty chemicals production. This facility (acquired from Gujarat Organics in 2021) is much larger in land area (~56,998 m^2) with an installed capacity of about 512 KL. It manufactures products like preservatives and personal care specialty chemicals such as parabens, methyl salicylate and other speciality chemicals. This unit currently runs at roughly 60% utilization and a new electrolyte additives plant is under construction here as a brownfield expansion. Company has ample land here for any further brownfield expansion

Unit IV – Greater Noida (Uttar Pradesh) is a small-scale facility operated via Acutaas’s subsidiary Baba Fine Chemicals (BFC) and installed capacity of ~1.8 KL of glass-lined reactor capacity geared towards semiconductor chemicals.

Key growth triggers

1. CDMO Ramp-up

Management targets ~1000cr revenues from CDMO by FY28 as it ramp up production of intermediates for darolutamide. Along with that company has a strong pipeline of molecules with many molecules in verification phase, which can be an optionality for the company.

2. Patent Expiry Wins

Several core pharmaceutical intermediates are expected to see volume uptick as major drug patents expire in 2025–2026, driving higher demand from generic manufacturers.

3. Ramp up of Speciality Chemicals

Semiconductor chemicals which are currently going through a down cycle, as demand comes back along with the company’s initiatives to expand customer base to Taiwan, Korea, Japan can bring new orders as customer qualifications conclude. Battery electrolyte additives are a new growth driver; a dedicated plant (Jhagadia) will be operational by H2 FY26 to start contributing to revenues. Company is positioned as a non china supplier for electrolyte additives. As speciality chemicals segment scales up , margins for the company will expand owing to better mix.

4. Capacity & Efficiency

Major capacity expansion at Ankleshwar (4x reactor increase) completed, ensuring ample headroom for growth. A new pilot plant is being set up to accelerate scale-up of high-potency chemicals and CRAMS projects, enabling faster commercialization of new products. Additionally, in-house solar power (10.8 MW commissioned) will reduce operating costs and support margin improvement as volumes grow.

Key risks

1. Semiconductor Demand Slump

Prolonged weakness in legacy semiconductor markets could delay the recovery and scale-up of Acutaas’s photoresist chemicals business (Baba Fine Chemicals), keeping the specialty segment growth muted.

2. Regulatory Compliance

As a chemicals supplier to regulated pharma markets, any lapse in GMP quality standards or environmental/pollution norms could lead to production halts or export restrictions. The business environment is highly regulated, and non-compliance can severely disrupt operations.

3. Tariffs if levied by the US on pharma imports

The US government has launched a investigation into pharma imports, which will likely culminate in tariffs within the next 6-12 months. This could impact demand for some of Acutaas’s customers, particularly those supplying generics to the US. It could also impact margins, as it may not be possible to fully pass on heavy tariffs to end-consumers.

4. Inability to secure customer approvals for new products in segments

Regulatory approval processes can be lengthy and uncertain, potentially delaying revenue recognition from new product launches.

5. Seasonality and lumpiness in business

CDMO businesses are generally lumpy and cyclical in nature. For acutaas H1 accounts for 40% of the topline and H2 with 60%. the nature of business is such where nothing happens for decades while months where decades happens. Company has been supplying intermediates to fermion since 2010, building relationships is a moat in this business . However if company fails to win new orders sales might get impacted.

6. Nubeqa’s growth slowing down

Any deceleration in Nubeqa’s market penetration or competitive pressure from other ARIs could impact Acutaas’s key CDMO revenues from darolutamide intermediates.

31 Likes