So don’t you think that you should work on finding the answer. Why for eg Nestle, HUL, Asian paint, Ramco etc have had high PE since decades.

Can market be wrong for decades at a stretch.

Since I started investing in 2006, HDFC Bank has been expensive. It still is. It may become cheap now because some changes are happening in Top Management but for past 14 years people kept finding value in PSUs and this guy kept doubling money every 2-3 years

Let’s put this line into play for next 2 years… Let’s see how Shree Cement copes up with the Corona issue and how others cope. That will tell you why Shree is better.

Ofcourse there will. Be multibagger is KCP and Digvijay for a 3 year perspective. But compare large to large

How a Kotak Bank has been behaving for past 2 years which will help him today vs how an IndusInd or Yes or RBL will be impacted. For past 2 years or so, Kotak has been extremely conservative

2 Buildings on the same road are valued differently because of Built Quality, Type of Residents, Maintenance quality, Look and Feel and so many other factors.

Why is a Samudra Mahal in Mumbai more expensive that a building just next to it. (Google about Samudra Mahal)

That makes sense. My issue regarding pricing was more of an issue regarding larger FMCG players than Kotak Bank. Nestle or HUL used be 40-50 P/E companies much like Marico or Dabur. What I can’t seem to wrap my head around is why a company like HUL or Nestle can have valuations at ~80 P/E ratio where companies like Marico/Dabur/Godrej gets correction in prices at 60 P/E threshold. If they can be considered expensive and get correction even with good performance, why should one assume that HUL/Nestle/P&G will continue to maintain such higher valuations in future too. Also, regarding Kotak Bank/Shree Cement, I think we’re in same boat where I also look at valuations same way as you do.

Also, I personally think looking at P/E at the moment is tricky situation where even with fall in prices, we don’t know how much of earnings will stay after present Corona situation. I think conventional ratios at the moment are deceptive in present situation where companies like HDFC Bank/ITC are way better prepared to tackle fall in earnings than a leveraged firm.

Sometime in longer bull run in some sector makes us to believe that high PE is good for the best companies. However, if you refer Nestle, HUL or any strong consumer companies around 2006-8, they all were available at very reasonable valuation (less than 50% of current PE) even though their growth rate was higher than present growth rate!!.

Euphoric PE in current market favorite companies is driven more by people (MF/AIF/ETF/FII/DII) who are in search of ‘safe house’ and not solely based on growth forecast. I think next one month will be crucial for such companies if FII keep selling (Sovereign oil funds liquidate their asset in India) - we will get these companies at reasonable PE. If these companies don’t correct in their PE, i think in uptrend you will not get good return from these companies but you will find multibagger in other names!!

Superb discussion on highly cyclical story like cement.

Meanwhile we get that Shree cement is excellent long term play,I would like to draw attention to investors here who thinks low PE stocks does not reward on long term.

Prashant Jain from HDFC AMC,fund manager of largest MF schemes of India since two decades is continuously raising his stake in one cent counter ,which may be not worth looking for retailers and the player is in the market since three decades…

It’s Ambuja cement.

He is continuously raising his hold in this counter since last one year.

This is the quantities as per feb 2020 data.

jamit05,

screener says cash flow from operations is negative for 2019 while its net profit is 249 cr.

other software companies generally converting > 75% of reported net profit to cash.

what could be the reason?

I majorly agree with @ashwinidamani what is another point which we are forgetting is that the reduction of corporate tax will be playing a significant role in companies with high ROCE’s and that is majorly achieved by quality companies who have established and proved themselves decades after decades so they do deserve a higher valuation unless the industry which its catering to is undergoing a disruption.

So a bear market is an ideal time to add these quality companies and during a raging bull market one can go for value bets.

This is my take and I may be wrong. Views invited.

23937 Net Profit Before Tax

3712 is Net Cash Provided by Operating Activities. So OCF is positive. Even the FCF is positive. So not really a cause of concern.

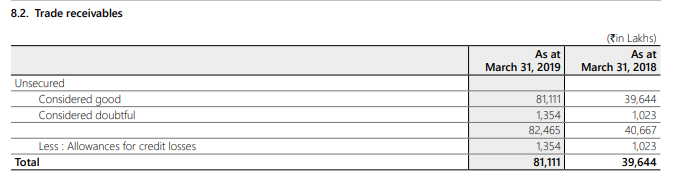

A concern though is that the Debtor days are highest in last decade. This AR shows Trade Receivables increasing from 2640 to 9325. This is significant.

Thanks. Though stand alone Cash From Oper is positive, consolidated numbers is negative cash flow from operations.

I think screener gives consolidated numbers usually.

It was never negative at consolidated level from 2008.

Sonata, in 2018-19 AR Consolidated Cash Flow statement reported a Profit of Rs.31550 (up from 26457 y-o-y). Which is nice. But after working capital adjustment the figure became negative mainly due to a sharp spike in Trade Receivables 39867.

The detailed explanation for which is given in the Notes 8.2

If it is at all to be trusted, then most of it is late, but recoverable.

A house at Nariman Point will surely be more expensive and for good reasons. But that doesn’t mean you will pay say 100 Cr. for a 2 BHK flat there, right ? Whether its real estate or shares in stock market, everything must have a price beyond which its just bubble. You can argue some things deserve premium, but “how much” is the question, which is what value investing questions and which is exactly what is never brought into arguments. Rather what is indicated subtly is ignore valuations and buy at whatever price.

Secondly, and this one is more important- why compare Nariman Point with Dharavi only ? Are these 2 the only places to live in Mumbai ? The point is, and I have observed this very often, why people always compare their fav. companies with DHFL, Edelweiss, Yes Bank etc. ? Is it because they are cheap ?

There are many good companies in mid cap and small cap spaces, at good valuations too. And I don’t mean to say “valuation = low or high pe” at all. But whenever there is talk about respecting valuations, why yes bank and the likes are always brought for comparison ?

My simple point was, if a locality keeps growing and adding amenities and other good aspects , it’s price will keep growing and expensive shall become more expensive. The savvy developer shall once in a while do innovation or pull a rabbit out of a hat and add value to the locality