Consolidated revenue up by ~10% QoQ

Standalone revenue up by ~7% QoQ

But PAT, PBT has declined due to higher expenses and interest cost.

As mentioned in results there is one time expense of 78 Lakh towards abortive inorgonic initiative. This dented PAT.

As per concall, company is focussing a lot on online sales in US to penetrate US market. There is new team for sternhagen sales. Grohe initiative is doing quite well.

5 Likes

Financial Results (Q3 FY19-20) - YoY Comparison

The company has reported net sales of Rs.74.92 crores during the period ended December 31, 2019 as compared to Rs.60.33 crores during the period ended December 31, 2018. The company has posted net profit of Rs.6.84 crores for the period ended December 31, 2019 as against Rs.3.06 crores for the period ended December 31, 2018. The company has reported EPS of Rs.2.60 for the period ended December 31, 2019 as compared to Rs.1.17 for the period ended December 31, 2018.

On quarter to quarter basis, sales has gone up by around 4.5%.

Looks like a decent result.

2 Likes

Kitchen sink business has been good for the company since very long. Its one of few companies into manufacturing of quartz sinks. Capacity utilization for quartz sink is almost 90% after they expanded capacity by 100k u/a in 2018-19. Designer SS sinks are also running at almost 100% utilization. Capex is going on for this segment to increase capacity by 25k u/a.

Valuation wise the company is trading at PE of around 12 while 8 years average PE is 24. At this valuation it might be attractive investment where you pay for their well established sink business and get many optionalities with great potential.

There are following optionalities which have good potential if any of them play out.

-

Company has been working on developing STERNHAGEN brand for luxury bathroom fittings and 3D wall tiles (which look great at lest in the picture)

So far it has NOT been working well. So far companys strategy was to expand distribution network and push the sales but it did not work. In one of calls, management has mentioned that they have now adopted a new strategy to push sales through more franchises and galleries. They have also completely changed the sales team. From last couple of quarters sales in this segment was negligible because of all these changes. It would be interesting to see how this plays out over next year. Management is optimistic that FY20 will be good for this segment. -

Home Appliances

This one is tricky but company has wide range of home appliances products like Chimneys, microwave etc which are more modern than other options. However, this too hasn’t played out yet. I personally don’t have much hopes from this one. -

Foray into US

Currently, export is mostly focused on UK, Germany and Europe. Company has been trying to set foot into US market and is also planning to open online portal for sales. -

Agreement with major GROHE

GROHE is a big brand and they have signed up with Acrysil for Quartz sink supply over next 3 years with expected revenue of around 60 crores. Interestingly, revenue expected from 1st year of deal was completed in just first 7 months. If this works well and this partnership continues to do well then this could be a game changer for the company considering the sheer scale at which GROHE operates. -

Continuation of trend in Europe and US for Quartz sinks eating up market share of SS sinks

Company has indicated that if they get enough deals for Quartz sinks then they may further expand their capacity by another 100k ( from 500k to 600k ).

It would be interesting to see how these possibilities play out in next year or so.

Disc

Invested

11 Likes

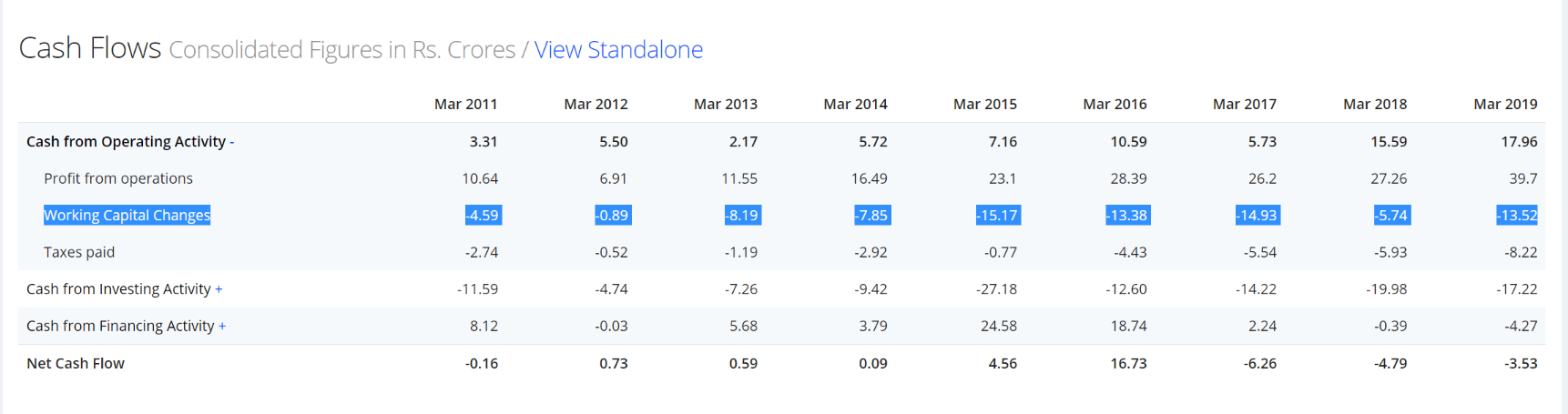

Company’s cash conversion is low as huge amount of money get blocked in working capital. And hence low ROE as well…

Disclaimer: Not invested, but exploring

2 Likes

Very succinctly made observations!!

Creating a line of kitchen appliances has synergies with the main activity of kitchen sinks as it enables the company to provide a range of products to its distribution chain. There is a space for a good quality kitchen appliance seller in the highly diversified market. The strategy should pay in long term if the efforts are continued to be made in a focused manner

The focus on Bath, however seems clearly value depletive as it is neither synergistic nor is it an easy play. The kitchen range market in itself is so huge and complex to provide the Company both, good growth and keep them challenged, there seems no logic for focus to be diverted to a new segment

The company has undoubtedly earned a place of pride by remaining a dedicated player in its area of core operations (despite it being a very small niche). Its core line of operations has reached a size and stage where the survival risks seem to have been successfully mitigated

It’s a dividend paying, profitable company with a global presence available at cheap valuations of sub 10PE

It has been able to successfully compete in an area of high design and quality element

It also has a reasonably strong shareholding structure

Promoter 44% (could have been higher)

Schock 8% (this appears under overseas corporate holdings)

HNIs 15% (led by Ashish Kacholia holding 4%)

MF 1%

Issues

- Dilution of resources and efforts by spreading out too far and thin. Recent Initiatives are yet to show results

a. Domestic market was approached in 2012, still after good 8-9 years, the presence is marginal at best - has not been able to create traction and a good supply chain

b. Bath Range neither synergistic, nor strategically thought out - There does not seem to be any reason for its raw material processing being carried out in a promoter company - corporate governance issues

- High debt, mainly due to increased working capital requirements, which can be a cause of concern from the point of view of governance or receding business fundamentals

- The founder promoter has passed away recently. Though the CMD has been at the helm for a long time

6 Likes

Very good results

1 Like

Company announces supply agreement with Ikea Switzerland.

1 Like

They are expanding capacity to meet export order. Expansion will be funded with internal accruals

4 Likes

What I found studying this company is,

- 3D Tiles, Sanitary ware, Appliances businesses look diworsified to me.

- Only Quartz sink & Steel sink business is worth on valuations parameters.

- most of their export orders are unbranded, they send finished product to established brand (Schock). so no brand popularity in foreign markets

- They will always be dependent on other large brands to sell their products

- They will always be dependent on other large distribution chain networks (Like IKEA)

- They are more interested in entering new countries, whereas they should first properly penetrate the ones where they are already present. ( I think there are many countries where they are already present have potential to give the turnover they are doing cumulatively, they are focused at nowhere-land)

- Promoters only know how to manufacture these premium quality products ( thanks to technology guidance by Schock), they lack in branding, distribution network etc)

Company looks fairly priced at 300cr valuations for monopoly business of quartz sinks(72% of revenue) which is expected to grow at 5-7% CAGR in the future.

I will think about entering this business only in case they hire experience CEO/Consultant who know how to build proper distribution sales channels.

These are my thoughts on this company.

Disclosure - not invested

11 Likes

Would like to get your thoughts on the recent IKEA order:

1/ Does this kind of partnerships are stable/sustainable in future or this is one-off order. If I am correct IKEA does strict due dilligence while selecting suppliers.

2/ Is this partnership a game changer for the company and increase their credentials in export market? Or this is just another decent order from a new customer.

3/ They have set up US subsidiary recently. How big this can be contributor to the future growth?

Last but not the least, does this look like a candidate for a PE investor to invest and steer the company in a new direction. Reading from the earlier posts, looks like they have the capability but lacks the strategic direction to move to next level.

Any inputs are highly appreciated.

Thanks Much

2 Likes

Resonates with me a lot, especially points 2, 6, and 7

Looks valued to me as well, may relook when it becomes reasonable…

I have issues with their focus, capital and resource allocation

2 Likes

Its surely a feather in the cap in terms of association, profitability is however suspect as the partners extract good pricing. It already has a relationship with Grohe…

Asset turnover is not very strong, due to which ROCE may get impacted

Yes, a PE is a good idea, but handling PEs is not an easy job

Current Financial liabilities are way higher than CASH and Equivalents in hand. It will definitely eat chunk of profits in near future.

Sunil Singhania’s Abakkus Fund buys 1.7 million Acrysil shares in a bulk deal on the BSE…

6 Likes

CNBC interview (link)

- Strong international demand witnessed in home improvement; 80% of their products go into home renovation

- In domestic market, they are 60-70% into renovation

- Expanding by 20% because currently running >90% capacity

- Witnessing very strong demand from international clients such as Ikea

- First phase of expansion of 15cr. is funded by internal accruals

- Looking to reach 500 cr. topline in the next 4-5 years time

Disclosure: No investments

12 Likes

I didn’t understand the initial part of the video where the management says that partnership between Schock and them was ended in 2002 itself and now they had just a equity position which they sold recently. In conclusion the business is not affected.

But there are reports of 2015 states their about their partnership, then article of 2020 talking about the same.

So, I can’t understand what really is happening?

Can you please share those reports of 2015 and 2020?

Second one is not a report its an interview of the management.

2 Likes