Accelya looks very interesting at this point. I have been tracking this company for over a decade. The first time I bought Accelya was way back in 2012 and exited completely in 2018. I started buying again in January this year and will continue to add.

Few points on why Accelya should do well:

Valuations are cheap, be it historical or absolute.

Recovery started in late 2021, and numbers have been decent since. My first target was matching 2019 numbers, which was done in this quarter.

A new growth cycle is underway, I expect earnings growth to be around 20%, revenue growth around 15%. There are quite a few reasons for this -

(i) There’s a trend of new carriers emerging all over the world, so a lot of these incremental partnerships are higher margin in nature

(ii) There’s renewed energy in the airlines sector once again, which means there’s focus on getting a better price for their inventory and also reducing costs, meaning outsourcing of non core functions. This helps Accelya cross sell better. Recent examples are Frontier Air adding Accelya’s AirRM 2, and Thai Airways adding outsourced revenue accounting services 1 to their renewals.

(iii) The biggest driver of growth is this new distribution system launched by IATA, that is called NDC & ONE Order. Will expand more on this –

NDC (New Distribution Capability) is a travel industry-supported program (NDC Program) launched by IATA for the development and market adoption of a new, XML-based data transmission standard (NDC Standard). The NDC Standard enhances the capability of communications between airlines and travel agents and is open to any third party, intermediary, IT provider or non-IATA member, to implement and use.

NDC transition is underway, which means this will see more one time project spending on transition, which benefits Accelya and the other existing players. Accelya has already started working on NDC implementation, plus they’re getting more allied work. For example, one of their big customers, American Airlines engaged them on a different project to support sale of unused EDIFACT tickets exchangeable through NDC connections 3. For reference - EDIFACT is the old standard and NDC is the new standard.

Resources to understand NDC and ONE Order –

Interesting times for a monopoly player that has been sleeping for years!

Adding some more insights on the implication of NDC adoption -

NDC decreases the value add of GDS companies like Sabre, Travelport. (How? Single integration with NDC APIs of airlines which gives out all offer and order related details. Infact ability to provide auxiliary offerings like luggage, seat, lounge, tour packages etc. is an add-on under NDC. In the existing pattern, GDS system maintain multiple integration with airlines (and other 3rd parties) to bring all these offerings under 1 roof. NDC will move this value add and move it inside airline servers.

What does it mean for airlines? (a) Relatively lower service fees paid to GDS - Lower fees due to lesser value add compared to existing integration. This incentives airlines to move towards NDC. (This is an educated guess and yet to find a very specific evidence from airlines or GDS companies’ annual reports/concalls. A quick scan to Sabre stock price chart and financials does confirm this theory. Sabre’s latest qrtly revenue is yet to reach 2016’s qtrly runrate). (b) Shifting of traffic to airline websites - As and when airlines rolls out NDC alongwith removing Edifact based content, in the short term, all the OTAs and TMCs who do not have NDC integration with GDS, will not be able to provide NDC based content to customers. In the short term, until NDC integration gets built into OTAs and TMCs, customer traffic will shift to airline websites. This just played out with American Airlines who took a bold step of removing Edifact content, and still able to maintain their revenues.[1][2]

Now what does all of the above mean to companies like Accelya?

As already highlighted by @saurabhved above, airlines sees incentives to move towards NDCs, and Accelya gets one-time opportunity to build it for them.

(Note that there are airlines like Delta who do not have any plans to move to NDC and favor staying with existing integration mainly to avoid any impact to corporate bookings which are through TMCs like cwt, which do not have NDC integrations with GDSes)

On top of air traffic growth, there is an optionality for Accelya as traffic shifts to airline websites Remains to be seen whether the shift is permanent or temporary, which depends on the evolution of seller side (GDS, aggregators, TMCs, OTAs).

I am just starting to study this company, and below is the key unknown I have.

Vista Equity Partners bought this in 2019. This would have perhaps taken care of the growth rate concern, but it followed COVID-19. The whole industry went southward. Things are slowly looking good now but it is unclear why an open offer wouldn’t surface again given that both Accelya Group and Vista are from the US/Europe. In that case, it just becomes a special situation where retail investors just watch from the sides.

If I understand your question correctly, you are afraid that Vista Equity Partners will come out with an offer to sell their stake.

Vista Equity Partners have bought into Accelya under their Perennial strategy. This particular strategy as per their website is focused on providing ‘permanent capital’. They say that under this strategy the investment commitments are for a much longer period than the traditional PE strategy which typically invests for 3-5 years.

If Vista Equity Partners has weathered the storm of COVID-19 with Accelya, I don’t think they will be in a hurry to sell out now that things are finally starting to look good.

Mansimar, there was an open offer triggered in 2020, which I read as Vista’s attempt to take the company private. The company is listed in India, but the promotor is US based. I honestly do not know if there is any downside to keep the company listed in India for them, so had this doubt in my head.

Exceptional items in consolidated financial results for quarter ended March 2024 consist of impairment of Goodwill pertaining to its subsidiary Accelya Solutions UK Limited (Cash Generating Unit - CGU), as a result of reassessment of potential of the business of the CGU, which is not a significant contributor to the earnings of the Company.

The Exceptional items in standalone financial results for quarter ended March 2024 consist of impairment of investment in its subsidiary Accelya Solutions UK Limited, as a result of reassessment of potential of the business of the subsidiary, which is not a significant contributor to the earnings of the Company

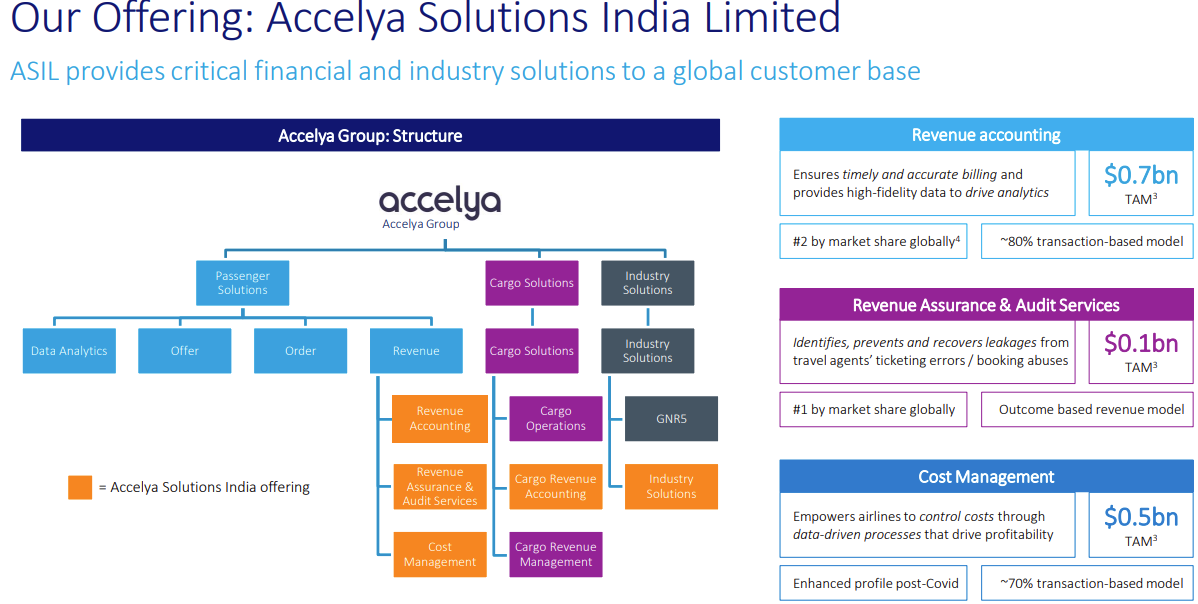

Gone through Accelya a bit but I dont understand why the listed Indian entity should benefit from the acquisition of Farelogix and the related benefit they are likely to gain from the growth of NDC. Correct me if I am wrong but as far as I can understand, the listed Indian entities business areas remain around the settlement side of the equation (Revenue accounting, Cost Management) and Revenue Assurance/Audit, while the newly acquired NDC tailwinds do not seem to be accounted here.

My understanding is that the growth of Indian entity is linked to global air traffic volume growth (majority of the business is transaction based), with the incremental NDC/ONE Order benefits not likely to be reflected here

Model is pretty simple. Backend development center is at lowest cost. Marketing strength in all the markets. It is a PE investment, their objective is maximizing profit. They have recently hired best possible industry veterans to lead the business. The results are showing up in terms of order flow. It lost Air India as a client and some notional loss in UK subsidiary. Seems ripe to scale up.

As per reports, Accelya is the clear leader in terms of a 50% market share in NDC transactions (Source), and NDC is the future standard that is expected to be adopted by the airline software industry in the next 10 years because it dramatically saves operational costs and time (I don’t have growth numbers to validate this).

A parallel point to consider is that Accelya operates in an industry that has inertia built in its core, which means that its customers i.e. airline companies are loath to fix what’s not broken. Accelya has been operating in this industry for the last 20+ years and counts 200+ airlines as its customers (Source). Most likely, unless these 200+ airlines don’t significantly come across better software, they will most likely not switch to new players.

So in short, there are 2 ways to look at this:

In the worst-case scenario, Accelya doesn’t grow its revenue but hums along with a 1-2% y-o-y growth rate because adoption of NDC is slower than expected and airlines are fine with ‘not changing what’s working’. In this case, Accelya won’t appreciate but is still a great source of dividends i.e. ~4% dividend yield.

In the best case, Accelya grows because of faster than expected adoption of NDC, increasing its revenue by 10%+ y-o-y. In this case, Accelya is not only a great dividend source, but also a potential source of capital appreciation.