For it to delist , I they would need to acquire atleast 15% such that promoter holding is 90% or greater. Last time the open offer met with poor response.

Again a conundrum, last time around the overall market conditions were quite optimistic unlike the current situation.

Delisting scenario looks quite unlikely, otherwise they would have quoted higher open offer price and grabbed as much as stake through this route.

4 Likes

Yup. Hope they don’t suck out the cash and make it take on additional debt. Best hope is being sold to Amdocs. Lets see how its packaged.

For taking out cash, only way is dividend - which is fair. Unless they do any siphoning, which broadly looks unlikely.

2 Likes

Selling to Amdocs? They just got acquired by Vista. May be you are speculating about distant future. For now with this price crash today, it will probably settle in 994 range and stay there until next set of good results. Was a good opportunity to exit yesterday.

1 Like

Yup, missed out on the exit opportunity. I was greedy ![]()

I agree its legit away, I was only stressing the fact,that the dividend payout were relatively higher compared to revenue growth. They are rightful in paying in out, It was error on my part to not discount this while taking a position.

Hi friends, I’m a novice investor. With this announcement of stake sale, should one continue to remain invested or exit? Please guide.

Received this from my DP

30/01/20- IDENTIFIED DATE & NOT A RECORD DATE

- Acquirer- Aurora UK Bidco Ltd.

- PACs- Vista Equity Partners Perennial, L.P and Vista Equity Partners Perennial A, L.P. Accelya Topco Ltd.

- Offer- 37,82,966 EQS (25.34%)

- Offer Price- Rs.956.09 per EQS (Includes Offer Price of Rs.944.19 per EQS + Interest Rs.11.90 per EQS @ 10% for the period between 15/11/19 to date of public announcement)

- Last Date for Competitive Bid- 21/01/20

- Last date by which the offer will be Dispatched to the Shareholders- 06/02/20

- Offer Open Date- 13/02/20 Close Date- 28/02/20 8. Last Date for Revising the Offer Price / Number of EQS- 11/02/20 9. Last date by which independent directors of the Co. shall give their recommendations- 11/02/20

- Last date of rejection/ acceptance and completion of payment of consideration-16/03/20 Description:

- Acquirers Acquirer has entered into SPA dated 15/11/19, with seller to acquire 100% of issued share capital of Accelya TopCo Ltd. indirect acquisition of 11,143,295 EQS in the Co. constituting 74.66% of the Voting Share Capital.

- Acquirers have deposited cash Rs36.72 Mln. (25%) in “ESCROW ACCOUNT” opened with CitiBank Ltd. At Mumbai

- The Offer is not conditional on any minimum level of acceptance.

- Unregistered shareholders can also participate in the Offer

- Pursuant to this offer if the public shareholding falls below the level of listing agreement then Acquirer will take necessary actions to raise the level of public shareholding to the level specified for continuous listing.

The buyer is a PE fund, it is in their interest to keep the stock listed. Thus, would not expect any revision in buyback px.

Would expect a larger dividend payout, as the co did not increase DPS in fiscal ending June 19, despite EPS moving from 60 to 71 Rs. Payout dropped from 80% average to 45%. To be fair, OCF dropped y/y, owing to increase in receivables. However, that might have been a short-term blip (hope).

Alternatively, the money could be used for an acquisition.

Either way, newsflow, ex of results (which is difficult to predict) is likely to be positive.

Valuequest India Moat Fund’s holding is now below 1%

1 Like

Any update on quarterly result & dividend? Can somebody summarize

Accelya dvd cut from 17 to 10 interim. Surprised why. Result bit weak, but understandable in transition phase between ownership change.

Overall lackluster result after some green shoots last quarter. The company is struggling on the growth front and unable to take advantage of operating leverage. Communication from management is very limited and directionally difficult to judge what company is trying to do. Hope they start concall after change in management.

Actually, both topline and ebitda is showing growth. I am ok, even if this co offers me 5%+ growth, but that is difficult to say. Other income has dropped sharply this Q, owing to drop in cash/investments, which has gone to fund higher debtor days. Seems a proper thing to do, or may be an aberration. Collection of debtors might help raise the payout again. I hope.

Situation at the moment seems unprecendented. Not sure how much of Accelya’s revenue now is pay as you go and how much is annuity? PAYG could be severely hit.

With majority of nations closing down borders ,lot of airlines’ business might literally come to standstill .A few might go bust in a few months as per CAPA report .

Airtraffic has decreased drastically with planes flying empty.

In the short term ,it’s a big & unpresedented business impact but in medium to long run , hard to imagine world without flights.

If a few of their clients go bust , this would have direct business impact even in medium term since new customer aquisition takes lot of time . Account recevable problems for Accelya could be furtur deterioted becuase of cash crunch airlines may face .

So next year outlook surely books bad.

Assuming that even if this corona epidemic is controlled somehow with in next few months , it might take a lot more months for people to calm their nerves & restart flying espeiallly for personal travel.

4 Likes

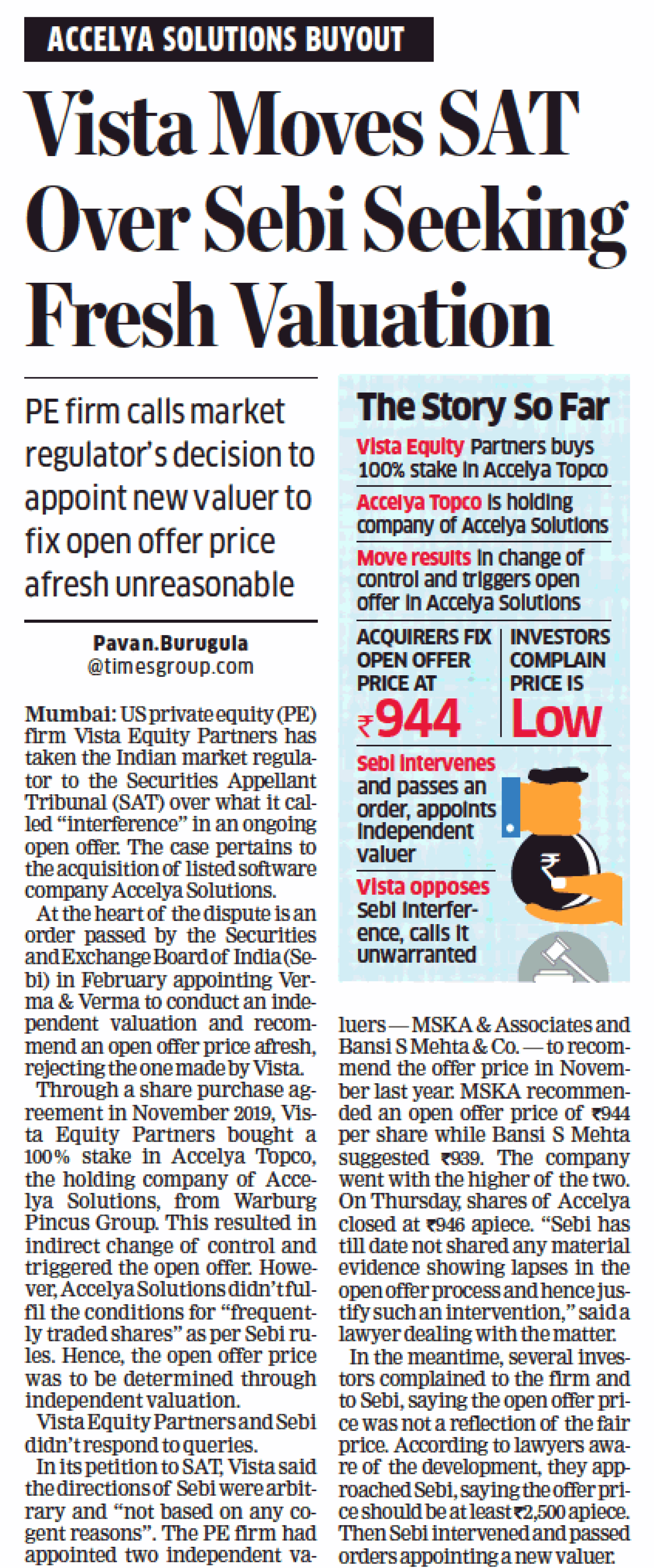

Vista Moves SAT Over Sebi Seeking Fresh Valuation

PE firm calls market regulator’s decision to appoint new valuer to fix open offer price afresh unreasonable

US private equity (PE) firm Vista Equity Partners has taken the Indian market regulator to the Securities Appellant Tribunal (SAT) over what it called “interference” in an ongoing open offer. The case pertains to the acquisition of listed software company Accelya Solutions.

At the heart of the dispute is an order passed by the Securities and Exchange Board of India (Sebi) in February appointing Verma & Verma to conduct an independent valuation and recommend an open offer price afresh, rejecting the one made by Vista.

Through a share purchase agreement in November 2019, Vista Equity Partners bought a 100% stake in Accelya Topco, the holding company of Accelya Solutions, from Warburg Pincus Group. This resulted in indirect change of control and triggered the open offer. However, Accelya Solutions didn’t fulfil the conditions for “frequently traded shares” as per Sebi rules. Hence, the open offer price was to be determined through independent valuation.

In its petition to SAT, Vista said the directions of Sebi were arbitrary and “not based on any cogent reasons ”. Vista Equity Partners buys 100% stake in Accelya Topco. Accelya Topco is holding company of Accelya Solutions

2 Likes

Any views on this business, in the current context?

Of course, the airline industry is under stress at present and will take time to recover.

From the credit-rating reports, there is customer concentration but have not seen disclosures - how much and to whom?

The LT financial performance is attractive. High ROCEs/dividend. Good ownership/governance.

Is this a good turnaround play? Appreciate views of experts who have been following this for a few years… Thanks.