Is the management still off-loading its stake regularly?

Any graph comparing number of shares of the company, promoter holding and share buyback over the years?

Yeah, the management at Infinite has been participating in the buyback, but they can’t not participate - their holding is at the maximum 75%, so if they don’t take part, then their holding % rises above the SEBI mandated limit.

Also, you have to understand that if a company is trading at ~3.5x trailing EV/EBIT, buybacks are a very, very good thing. I want this company to have as many buybacks as it possibly can, as my beneficiary ownership % of the company and hence EPS increases everytime.

Hi @sarangg thanks for starting this thread. I see that you made some new additions to the portfolio based on recent correction. It would be helpful to understand your perspective for these additions.

I work in the same industry where HGS and Infinite belong and my take is that any company that is able to show consistent QoQ growth(even marginal) in this tough environment is a good bet from a long term perspective. I am invested in both of these companies but I have increased my investment in Infinite because its consistent QoQ growth from last 3 qtrs…

Yeah absolutely. What really pushed me over the edge were these Quarter’s numbers. HGS posted a fantasic set of numbers in terms of profitability - EBITDA and FCF that were masked by FX changes. I don’t see the rupee appreciation as having any fundamental backing, so I’m not worried by those hedging losses, and I think its a great opportunity to buy the underlying business at an unbelievable discount.

For Infinite, the FX charges weren’t the only problem - employee costs also shot up, but at these prices with almost Rs. 83/share of cash at a CMP of Rs. 223, I really don’t see how this company could possibly be worth less. I feel like consistent buybacks at market prices/slightly higher can create huge value for exisiting shareholders. At these valuations, if all of the profits were used for a buyback, the company would grow EPS at 18% p.a. JUST by buying back share every year (not considering the otherwise 10-20% growth in top & bottom lime).

I personally find HGS to be a value trap. It is languishing at these levels forever now. It used to be a dividend player. But it looks like even dividends have dried up. BPO//KPO is low value volume play. There are cheaper countries than India these days. So as such this business has low pricing power (been that way for a number of years and unlikely to change).

I would also say if you have high conviction to be long on the market. Short is a no for value investors as investments are not time bound and we buy on a time horizon of forever. Investing is a long learning process and we keep getting better with time. All the best.

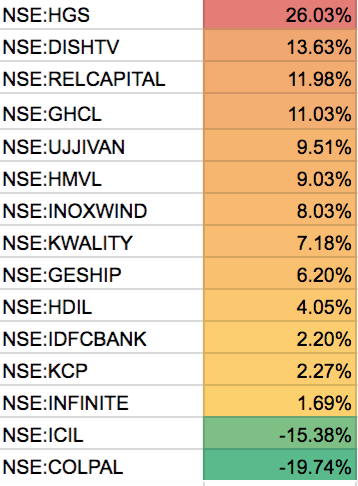

Here’s my current allocations for those interested. These deep-value type stocks have done well, and I’ve refined my short thesis into either more 1) catalyst driven (Colpal) or 2) as a hedge (IndoCount).

Although many stocks are repeated, here are some of the thesis for the new ones that aren’t covered in VP:

Dish TV: merger with VD2TH should drive synergies, purchasing power with media cos’, and pricing power in industry due to consolidation. Classic telecom sector consolidation wave, and a bet on the biggest player. As APRU increases, marginally flows straight to EBITDA. Very low base APRU in India vis-a-vis other developing markets. Also ~8x EV/EBITDA valuations

Rel Cap: RCOM bankruptcy is almost immaterial, huge value from SOTP perspective, bargain valuations with high growth

Short Thesis

Indocount: Much more highly valued than GHCL’s textile division, should be a good hedge if textile cycle falls off the cliff, allows me to hedge exposure to GHCL’s unit which is valued at almost 0 by the market. I am also just generally bearish on the textile cycle and I think it can turn bad very soon.

ColPal: Crazy valuations, almost saturated growth (~80% penetration of toothpaste in india), price war by Patanjali - a player with an unfair advantage of free publicity, no profit incentive, not paying employees (?), and super low pricing that is actively increasing its distributor network. Margins have remained good despite price cuts in recent quarters due to low oil prices, and even then they have steadily lost market share to patanjali.

Also, a note on shorting: I view having a short position a %age fraction of my net long same as holding that much in cash, since you effectively hedge out the market risk. Many known value investing hedge funds - Greenlight Capital, Julian Robertson and his ilk of hedge funds all use these tactics to find mispriced companies on the other end of the spectrum

Agree, there are well-known hedge funds which specialize in shorting.

In the US, one can short for a much longer duration (I guess in years), whereas in India, I am not sure if you can short for more than few (2) months.

Closed it net flat (small profit afaik) when I shifted to Colpal as it was more actionable. I still think its overvalued but there are better co’s to short such as Colpal which also have business threats.

Also @paragbharambe nothing stops you from rolling short f&o positions month to month. Overall transaction cost is low at Zerodha ~0.1% a year on avg. In the US, the borrow fee is actually larger than cost of shorting in india

I came across this forum recently, i have been following hgs from the past 1 year.

The company is aggressive in recruiting students for voice process, given the talk of automation i dont see any real transformation in the company, its peers such as firstsource have also been focussing on RPA and other tools.

The stock has been rangebound for the past 6 months.

What do you think about the future prospects of this company ?