Regarding digging deeper into the company and analysing the company to its bare bones, sometimes this is counter productive.

We have to be very clear about what to ignore and what not to ignore. As long as company shows good growth along expected lines I tend to ignore factors such as promoter compensation, related party transactions (if these are not too material) and such other details.

Coming to examples the big winners came out of extreme undervaluation and subsequent rerating.

Canfin was showing 30-40% growth and available at 0.7 times book value. Since it was govt owned entity market treated it as a psu and was accorded poor valuations.

Ajanta used to trade at 5-7 PE inspite of 30-40% cagr growth. Here market did not fancy pharma stocks and since ajanta was not having a strong US presence, it was valued cheaply. Rest is history.

Similar things happened to mayur, kaveri etc. Even on valuepickr you can go through relevant threads and go back in time to see what arguments and counter arguments were put up at that time.

With my beginner’s understanding, still totally agree with this Hiteshbhai. There is vast amount of data and dimensions and we must be clear and simple-minded to be able to arrive at clear insight. Thank you.

@Bikram11206178 investing is always about rewards and the risk you have to take to earn it. Once cannot just look at the green flags and ignore red flags. My thinking is that green flags should be apparent and one has to dig deeper to find red flags.

Once you are aware of the risks then you should ask yourself what is the likely impact on the stock price and how will you react if or when risk materializes. When stock price drops, red flags are all over the place. If this is how you discover them, then you are setting yourself up for shock and awe. You cannot make rational decisions in this state of mind.

No. You never know what is small and what is large until a risk materializes and price drops. Even a small issue has a big impact when stock price is high. I try to quantify the risks as much as I can and if I cannot, I stay away. Finally I ask myself if I am willing and able to buy this stock if any of the risks materializes and stock drops 20% or more? If the answer is NO, then I stay away. In the end it’s always your psychology that takes over at crunch time.

@phreakv6, There is no doubt that books are useful and the cheapest source of knowledge even in the age of Internet. My only point was that one cannot read books for 2 years and become an investor.

Investing has an element of skill that one has to learn on the job much like how we learn to ride a bicycle or learn to swim. No amount of books will help us with that. A beginner should then wear protective gear or enter only a waist deep pool. That’s the equivalent of starting with Nifty 50 companies.

Once you figure out what’s working and what’s not, you can refer to books to learn the skills you don’t have. It could be mental framework, accounting or economics etc or something else. I found this mode of learning to be more effective than the other way around. Again, just my experience, may not work for others.

My two cents on the usage of books in investing. Even if a 200-page book contributes only 1-2 core ideas to your existing knowledge of investment principles, that’s substantial. As Charlie Munger liked to put it “It’s a lollapalooza.”

As a personal example, I just finished reading “The Black Swan” by NN Taleb. If I could sum up the book in a single sentence, it’d be “Expect, but don’t (try to) predict extremely unlikely events.” This is a very simple take away. However, it probably added a few layers to what I already knew about investing:

Reinforced the importance of a Margin of Safety in investments.

Reinforced the futility of trying to model extremely unlikely events, but keeping in hindsight the likely financial impact (i.e. Knowing my possible draw downs).

The “barbell” strategy, although not of much use to an investor, reiterates why one should consider both Equity and Debt as possible investment avenues and not just Equity.

The book even touches upon how Gaussian distributions could be used to measure the range of impact. I regularly “stress” my Valuations and turn the results into a Normal Curve in order to have a better picture. I regularly stress that the Value of a company is a range of Values and not a single Value. So, once again, I stand reinforced.

This is just a small example. As one reads more and more (Not necessarily just books, even magazines, articles or Annual Reports), one’s understanding compounds drastically. What one reads is his or her own choice. However, reading all together is a valuable tool.

Hi @dineshssairam

As far as normal distributions are concerned, they work well to estimate a range only when the outcome is random i.e there is equal possibility of set of events happening. A throw of dice for e.g. When outcomes are non random normal distributions cannot be used. The likely outcome of business decisions and their impact on margins and revenue is a non random process. If one must model this there are many non normal distributions that one can use but using a normal distribution for a non normal process is an incorrect implementation of statistical analysis. Talebs work has been shaped by his ex profession as an option trader where violations of normality are routine and the norm rather than the exception.

While business decisions and the respective outcome may not be normal (Say, Margins are more likely to follow a Triangular Distribution and so on), the ultimate outcome in a stress test is almost always normal. In our case, the Value of a company, based on our stressing of estimates, will throw up values that are almost normal.

Agreed that I use excel’s built in NORMDIST function to simulate a normal curve of Values, even if I didn’t, the resulting distribution wouldn’t be too different. After all, we’re simply trying to understand at some given level of confidence, what is the range of expected Values.

The reason why the normal distribution fails to capture the range accurately in cases most often found in business is because it doesnt consider scale. Talebs work has its genesis in the works of mandelbrot who was a pioneer in analysing scaling. With scale things dramatically and a business operating at a higher scale of operations displays characteristics that follow non normal properties. Ofc when businesses approach their opportunity size and continue to operate at that scale then its possible to use normality assumptions.

Let me try to explain how I go about doing this and perhaps you can help me judge whether a Normal Distribution makes sense. For all my Valuations, once I arrive at the final Value, I do the following:

Use RANDBETWEEN to fluctuate all the assumptions in a range of +/- 15%-20%

So essentially, I’m saying:

“At X% of Sales Growth, Y% of Margins and Z% of Operating Efficiency, the Value is V”

“At X1% of Sales Growth, Y1% of Margins and Z1% of Operating Efficiency, the Value is V1”

And so on

This is repeated at least a 1000 times and all the results of the Value (V, V1, V2, V3…V1000) alone tabulated.

I then use the NORMDIST function to build a Normal Curve of Values. This allows me to looks at the Value of a company in terms of probabilities rather than a fixed number.

Sorry if this is going off topic. Kindly reply in a Message if that’s the case.

@dineshssairam - If I may butt in - What you are doing is deriving value based on a set of assumptions - lets call this value V (As you have, as well). Now when you vary the assumptions any number of times by a fixed 15-20% in sort of combinations and generate V1, V2… VN, it will produce a normal distribution by design of what you are doing, because though the inputs are random, you are controlling the range for those inputs - This is quintessential Gaussian - something like distribution of height or age among a population - You are never going to find someone thousand years old or a thousand feet tall because these fall within a fixed range.

Mandelbrotian is self-similar, scale-invariant, like fractals - these cause fat-tails in the distribution. By self-similar in this context, you can think of it as a company that grows at 25% for 10 years and after that, still continues the same for another 20 years or maybe more (say 100 Cr to 100000 Cr in in 30 years) - In essence, its trajectory in the first 10 is the same as the trajectory in the second 10 and the third 10 and there-in comes the fractal nature of it. Granted, these are not common but that’s why these come out of the left-field and create once in a decade or once in a hundred year kind of companies/events/disasters etc. It will obviously be imprudent to assume such growth for such periods of time when valuing but stellar companies in extremely large markets can do it.

I believe we are going more and more towards the Mandelbrotian - think central bank printing presses, globalisation and the power of the internet coming together to create FAANG-type monsters. These cannot be modeled by a Gaussian and this is what NNT keeps on harping about in his books.

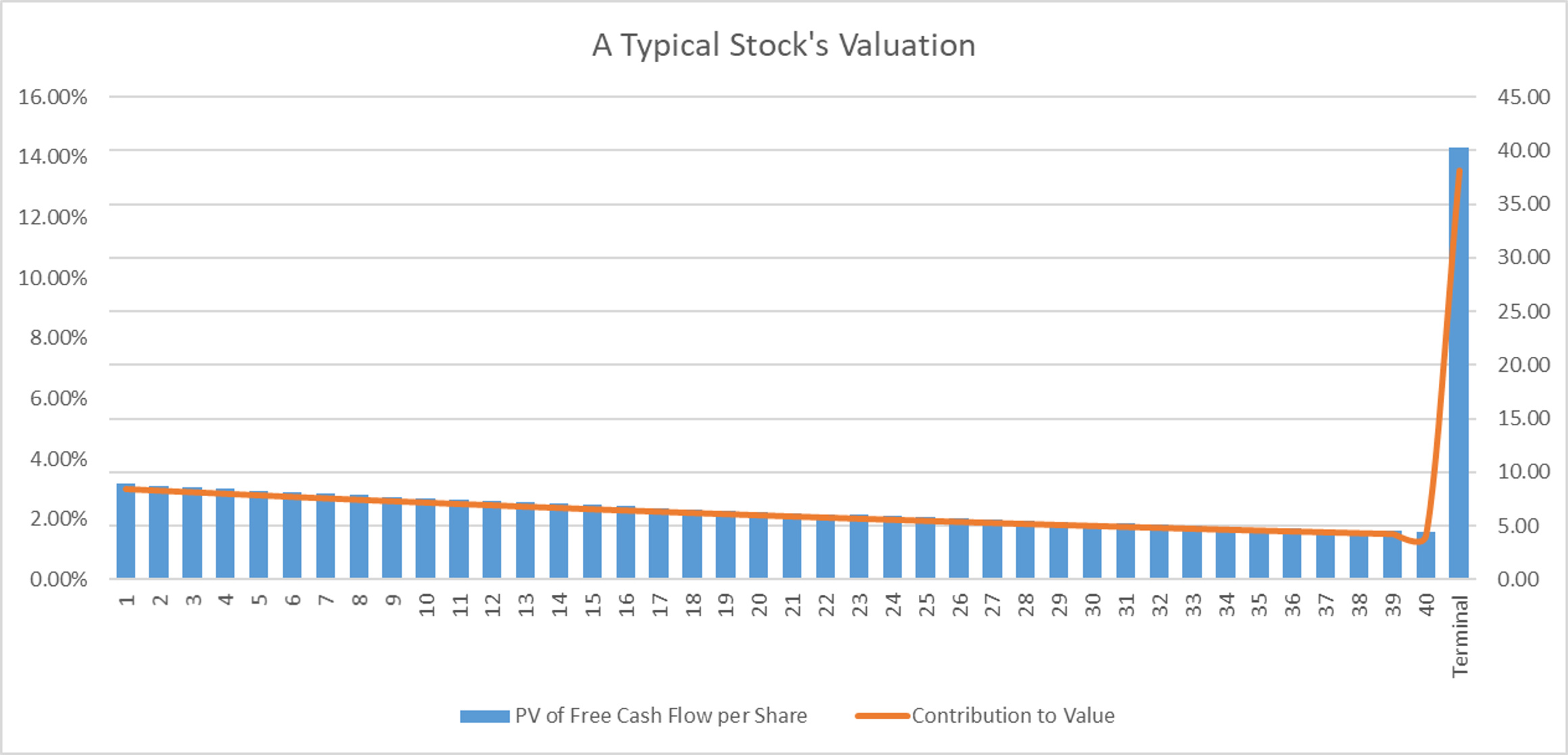

But when we’re talking about a stock’s Value, we’re essentially considering the discounted value of all future cash flows. Beyond a certain point (Say, 25-30 years), the denominator i.e. The WACC raised to the power of number of years will become simply too large. Considering how we typically value a stock:

That is to say, beyond a certain point, the marginal utility of adding one more year of projection diminishes drastically. It would like trying to fine tune whether a stock’s value is Rs. 99 or Rs. 100 – which is just a waste of time. Of course, the underlying assumption here is that the growth of any company eventually slows down.

The argument that there are companies out there which can grow like fractals decade after decade is an interesting one. But don’t you think by using a regular Valuation model (Say, one with a 20 year High Growth period), we’re actually being conservative? Conservatism never hurts when it comes to Valuing something for personal purposes (Sure, it hurts when we’re dealing with it at a corporate level i.e. M&As and Spin-offs). And as I have just shown, additional fine tuning to an already decent valuation model yields less impactful results, which aren’t worth the effort.

I understand that representing the probability distribution skewed to the left or right is the exact way to going about doing this. But a Valuation is anything but exact. It’s approximate at best. All we’re trying to come up with is a range of values and the probabilities that a specific value is correct. The Normal Distribution allows me to do that and at great ease.

I only read books to extend my knowledge. I have read most of the financial books out there from the age of 18. I do not apply the theories especially the financial parameters and rations. For me, track record of management and market they operate in is suffcient to take a call.

Most of the older generation of investors have not read any stock market or investment books, but I know of many who have minted hundreds of crores in hdfc bank, l and t, page industries, and the list goes on. Most of them were concentrated bets of 1 or 2 shares. I know of one gentleman who only invested in hdfc bank when it started, and today sits on thousands of crores.

Fair enough, us younger investors want to go one up in terms of knowledge, but nothing can replace timing, guts, and luck.

This is perhaps the single most useful post a novice can read. I have read dozens of investment books in the last 19 months and while they have been useful in populating mental models, those models are only truly imbibed when put through this process. Based on my experience, I recommend anyone starting out to read no more than 5-10 books before embarking on this journey of studying companies rather than investing principles.

Now everytime I feel tempted to start a new book, I re read this post and start analyzing a company instead

One of our valuepickr @margin_of_safety has started an educational course on :Investment Research – How to Research to Build Conviction.

Three Month Video + WhatsApp (For Queries)

I have recently suscribed to his videos and found it valuable.

I think building conviction in investing is important and for that learning is important.

Below link Growthx

I read the entire thread and it is very useful for new investor. I have read some books like 5 rules of investing, one up on wall street, intelligent investor etc. I am slowly building criteria on how to identify a good company. But still I am not able to build conviction on a stock. Just to give example for reference purpose, few days back I came across Hero motor. I found this stock good on financial parameters like good ROE/ROCE, low debt, good management and available at 14 PE as comparative to all time PE of 19. But I didn’t have high conviction on the story. So I bought small quantity of the stock. I have below thoughts on building conviction by reading @Yogesh_s portfolio and his comments on different thread. I would request to add/update to the list.

Read annual report for last 10 years as Yogesh mentioned in this thread. I think this is the tough task and need patience. But I believe it is needed in order to build conviction and see if management is fulfilling the promise they have made in past.

Read about the industry. e.g. for Hero motor, see if there will be demand for bikes in next 5-10 years and where urban/rural areas

Most important thing - write up 1-2 page about the company. I think this is most important as it will force person like me to do #1 and #2. Write up should have

Brief description about company. What it is doing and how it is getting revenue?

Story - why do you think company will grow in next 5 years

Financials - 3/5 year ROE/ROCE,Debt, promotor holding

SWOT analysis - this will force us to think about competitor

Price - What is the intrinsic value? I think we can use some excel from safal niveshak to come up with intrinsic value. In case current price is very high than intrinsic value, then wait for price to come down or start buying in small quantity and keep buying on dips.

Investment checklist - this could be an excel or part of writeup. I have to create a checklist. I looked at Capital allocation framework thread which has excellent input for the checklist.

Keep visiting the writeup every quarter to see if story has been changed

@hitesh2710, Hi Hiteshbhai

What are the steps (rough guidance )one needs to follow to do "feel " type of investing ( this is the one i prefer as against too much data crunching or over emphasis on quantitative which i do not prefer due to missing out on good investment ) as mentioned in your post ? What generally are steps you follow for initial shortlisting to final selection for investment ? Your investment process would help newbie investors like us a lot . Many thanks

As Buffett and Munger once said, If you started reading AR/businesses randomly, you would not learn as much. You have to have someone in theory in your head before diving into mass amount of data.

Buffett- Before diving into AR, an investment framework is necessary.

Following this, I read over 23 books on philosophy/psychology/investing reads, annual letters, podcasts, reading past investment success and failures trying to figure out what works and what does not, how they think, and other sources over past 2.1 years But, yeah! They really helped a lot.

Trying to collect mental models like Munger said. But, now feeling little bit disheartened after post of Yogesh sir.

Reading is just one aspect, there are cognitive strength, financial affordability, personal but not unchangeable psychological perception, time, age, professional expertise, experience, and a plethora of other things that come into the picture in whatever capacity and influence the journey going forward. So each one may have a different approach to reading, some may need the assistance of books to create a model, some may need just a few paragraphs, an article, a little direction, some concern only with quantifiable things.

Whichever is the reason for creating a perspective, the journey is also an introspection of oneself, being stampeded by market, getting lucky unexpectedly, unrewarded despite deserving, getting lifted by a rising tide, and whatnot. I guess anyone can write a book after spending some time in the market.

Believer and beneficiary of reading, the cumulative effect reading has with time is beyond words. This forum itself is helpful to have a broad understanding of the market, and there exists threads which hundreds of posts over the course of years, filled with objective and subjective arguments, logical and biased views, which to me are like books.