Company has confirmed NSE has listed their shares under the well established Permitted to Trade route where stocks listed on one exchange only can be offered on the other exchange without going through a formal listing process. Some companies choose to still go ahead with a “full” listing while others choose to continue in PTT. One article showed data that stocks listed on NSE via this route see +100% increase in trading volume within a year. This is great news and IMO a major trigger for the stock.

4 Likes

Came across an upcoming NSE Emerge IPO Q-Line Biotech which may be worth tracking from the perspective of the broader Indian IVD space.

This is not a direct comp to 3B Blackbio in my view, but it does give a useful datapoint on how the market may value Indian diagnostics / IVD manufacturing platforms.

Q-Line is a Lucknow based IVD company with 75% of revenues coming from UP state. As per the DRHP, it manufactures and markets reagents, kits, diagnostic instruments, equipment,across clinical chemistry, haematology, HPLC, rapid/ELISA, molecular diagnostics, etc. The IPO size is around 214 cr, with an IPO price range of 326 - 343/share.

Some rough numbers from the IPO docs-

-

FY25 revenue from operations: ₹314 cr

-

FY25 PAT: 28 cr

-

PAT margin: ~9%

-

EBITDA margin: 22%

-

Debt/equity: 0.87x

-

Implied market cap: ~800 cr

-

Implied valuation: ~28x FY25 PAT

While Q-Line does mention molecular diagnostics, its FY25 reagent revenue is mostly from:

-

Clinical chemistry: 64%

-

Haematology: 29%

-

Molecular diagnostics: only 0.1%

So Q Line looks more like a broad IVD reagents / instruments company, whereas 3B is much more focused on molecular diagnostics and PCR-based kits.

The IVD industry report in the RHP is also quite useful (directionally only, these are never accurate) to see where 3B plays vs Q Line.

3B’s portfolio most covers #4 Molecular Diagnostics (TruPCR) and #1 Immunodiagnostics (Trurapid & Coris). Q Line is focused on Clinical Chemistry + Haematology. Molbio is mostly into Point of Care Tuberculosis tests kits + devices so probably fits into #5 Others.

They have also shared financials of some peers including J Mitra, Transasia Biomedicals, Molbio Diagnostics, Agappe Diagnostics. 3B is not listed as a peer, I’ve added 3B next to them for easy comparison.

The valuation is interesting. If Q-Line can come at roughly 800 cr+ market cap / 28x FY25 PAT, despite lower margins, higher leverage and working capital needs, and Molbio targeting 12-15,000 cr valuation based on reports (100x FY25 PAT), then 3B at around 20x FY26E PAT, with net cash and much higher margins, continues to look like a bargain on a quality-adjusted basis.

Source - RHP https://admin.qlinebiotech.com/uploads/investor/14fb9b2d52e3ffc226eb0e5fb5955322.pdf

5 Likes

3BBB has always been cheaper valuation wise and every year we make the same argument but the stock price has been decreasing for more than 1.5 years with valuation halved from peak.

One of the main reasons I’ve come to realize is it’s inconsistent nature with regards to its results. There’s always room for surprises which the market doesn’t like. Once the revenue and profits become stable the stock might perform.

Also targeting 10-15% revenue growth even with a small base when big companies grow on similar levels with a much larger base doesn’t sit well.

2 Likes

The stock is up handsomely on 2, 3, 5 and 10 year timelines. Looking at 1 year price performance and judging a company is not reasonable IMO. The goal of this forum is to find dislocated opportunities in the market!

Would love to hear a counter thesis or why you think it won’t perform over the next 2,3,5 years - is the underlying business compromised?

6 Likes

I’ve held this stock for 3.5 years and it’s my biggest investment, so I’m speaking as a worried investor. The main reason I’m still holding is their cash balance and the fact that they’ve mostly used it well but it’s taking too long to show up in results.

2 quarters ago they were talking about 15–20% growth. Now it’s down to 10–15%. They seem honest, but for a ₹1,200 crore company they need to move faster and be more aggressive.

Take the Coris acquisition. Their sleeping sickness test kits will become useless by FY2028, and their only backup plan is US FDA approval. What if that doesn’t happen? What’s the Plan B?

There’s a lot of talk about digital PCR and NGS but no real revenue to show for it yet. The one thing I’m genuinely excited about is their POC sample to answer system, but when will it actually launch, and how will they compete against the big global players?

There’s a lot to be hopeful about, when will any of this actually start making money?

4 Likes

They posted about these three test kits in PGx category (Pharmacogenomics) on their LI page so I did a little digging

![]() TRUPCR® DPYD Mutations Detection Kit

TRUPCR® DPYD Mutations Detection Kit

![]() TRUPCR® TPMT Mutations Detection Kit

TRUPCR® TPMT Mutations Detection Kit

![]() TRUPCR® NUDT15 Mutation Detection Kit

TRUPCR® NUDT15 Mutation Detection Kit

TRUPCR® DPYD Mutations Detection Kit

- The Mechanism: Fluoropyrimidine drugs are heavily used to treat solid tumors, particularly colorectal cancer. In a healthy patient, the DPD enzyme (encoded by the DPYD gene) metabolizes and clears over 80% of these drugs from the body.

- The Danger: If a patient has specific mutations in their DPYD gene (such as the 2A* or HapB3 alleles), they produce little to no DPD enzyme.

- The Clinical Value: Administering a standard dose of 5-FU to a DPD-deficient patient causes the drug to build up to toxic levels, leading to severe diarrhea, vomiting, and potentially fatal bone marrow suppression. This kit identifies those patients so doctors can drastically lower the dose or switch therapies entirely.

TRUPCR® TPMT Mutations Detection Kit

- The Mechanism: Thiopurines are immunosuppressive drugs used for leukemias (like Acute Lymphoblastic Leukemia) and autoimmune diseases. The primary enzyme responsible for breaking down these drugs is TPMT.

- The Danger: Certain genetic variants (like c.238G>C and c.460G>A) cause TPMT deficiency.

- The Clinical Value: Without functional TPMT, standard thiopurine doses destroy the patient’s ability to produce white blood cells—a condition called myelosuppression. This kit detects the four most common TPMT mutations, flagging patients who require a fraction of the standard dose.

TRUPCR® NUDT15 Mutation Detection Kit

- The Mechanism: This kit serves a very similar purpose to the TPMT kit—preventing thiopurine toxicity—but targets a different genetic pathway (NUDT15).

- The Danger: While TPMT mutations are the primary cause of thiopurine intolerance in Western populations, NUDT15 mutations are the leading genetic driver of severe thiopurine toxicity in Asian and Indian populations.

- The Clinical Value: Testing for NUDT15 (often bundled into broader Pan-Myeloid or PGx panels) closes a critical genetic blind spot, ensuring that patients of Asian descent are accurately screened for drug sensitivity before starting treatment.

B2B biotechnology companies and kit manufacturers based in India that produce the reagents and assays for these pharmacogenomic tests, here is the breakdown:

1. 3B BlackBio Dx Limited (The TRUPCR Manufacturer)

- Location: Bhopal, Madhya Pradesh

- Kits Manufactured: TRUPCR® DPYD, TRUPCR® TPMT, and TRUPCR® NUDT15 Mutation Detection Kits.

- Overview: This is the specific company that researches, develops, and manufactures the TRUPCR® brand you asked about. Formerly known as 3B BlackBio Biotech India Limited (a subsidiary of Kilpest India Ltd.), they are one of India’s leading manufacturers of molecular diagnostic and oncology real-time PCR kits. They supply these ready-to-use kits directly to pathology labs and research hospitals.

2. Genecore Biotech India Pvt. Ltd. / Genequest Diagnostics

- Location: Ghaziabad, Uttar Pradesh / New Delhi

- Kits Manufactured: Genemap™ DPYD Mutation Detection Kit.

- Overview: Under the “Genemap” brand, this company manufactures a TaqMan probe-based real-time PCR kit specifically for DPYD mutation detection. Their kits are ICMR-approved and are distributed to clinical laboratories to screen patients before fluoropyrimidine chemotherapy.

3. Biogenix Inc. Pvt. Ltd.

- Location: Lucknow, Uttar Pradesh

- Kits Manufactured: TPMT ELISA Kits (8-patient and 40-patient formats).

- Overview: While 3B BlackBio and Genecore manufacture PCR kits to find DNA mutations, Biogenix manufactures ELISA (Enzyme-Linked Immunosorbent Assay) kits. Instead of looking for the mutated gene, these kits allow laboratories to measure the actual functional activity/levels of the TPMT enzyme in a patient’s blood. This serves as an alternative diagnostic pathway to prevent thiopurine drug toxicity.

Note: For the highly specific NUDT15 mutation—which is distinctly relevant to Asian populations—3B BlackBio Dx is currently the dominant, if not the only, major domestic manufacturer producing a targeted, commercialized PCR kit specifically for that gene in India. Many labs testing for NUDT15 without a TRUPCR kit rely on custom-built Next-Generation Sequencing (NGS) panels rather than boxed commercial kits.

8 Likes

In stock market for finding multibaggers,50%of the job is done when you have trustworthy promoters. Rest is checking the growth potential and having patience. I think they hv moved beyond India increasing addressable market.I feel scientists from coris can provide the non linear growth,if they are guided correctly. The cdmo companies now in trend are because of the research scientists accomplishments in formulating compounds.Yes but true patience is wearing thin. It’s like no growth in the company till 1 year. I am biased bcoz of being invested

1 Like

Was checking if company has Ebola antigen test and turns out it has trurapid lateral flow kit and it has been evaluated by one team against chinese, korean and japanese(published in Aug,2025). https://www.sciencedirect.com/science/article/pii/S1386653225000721 . Good news: its better than other available indian rapid test. Bad news: its performance is bad compared to chinese,korean and Japan test kits. company’s main product is RT-PCR for which it is not applicable and also kits might have improved by now.

3 Likes

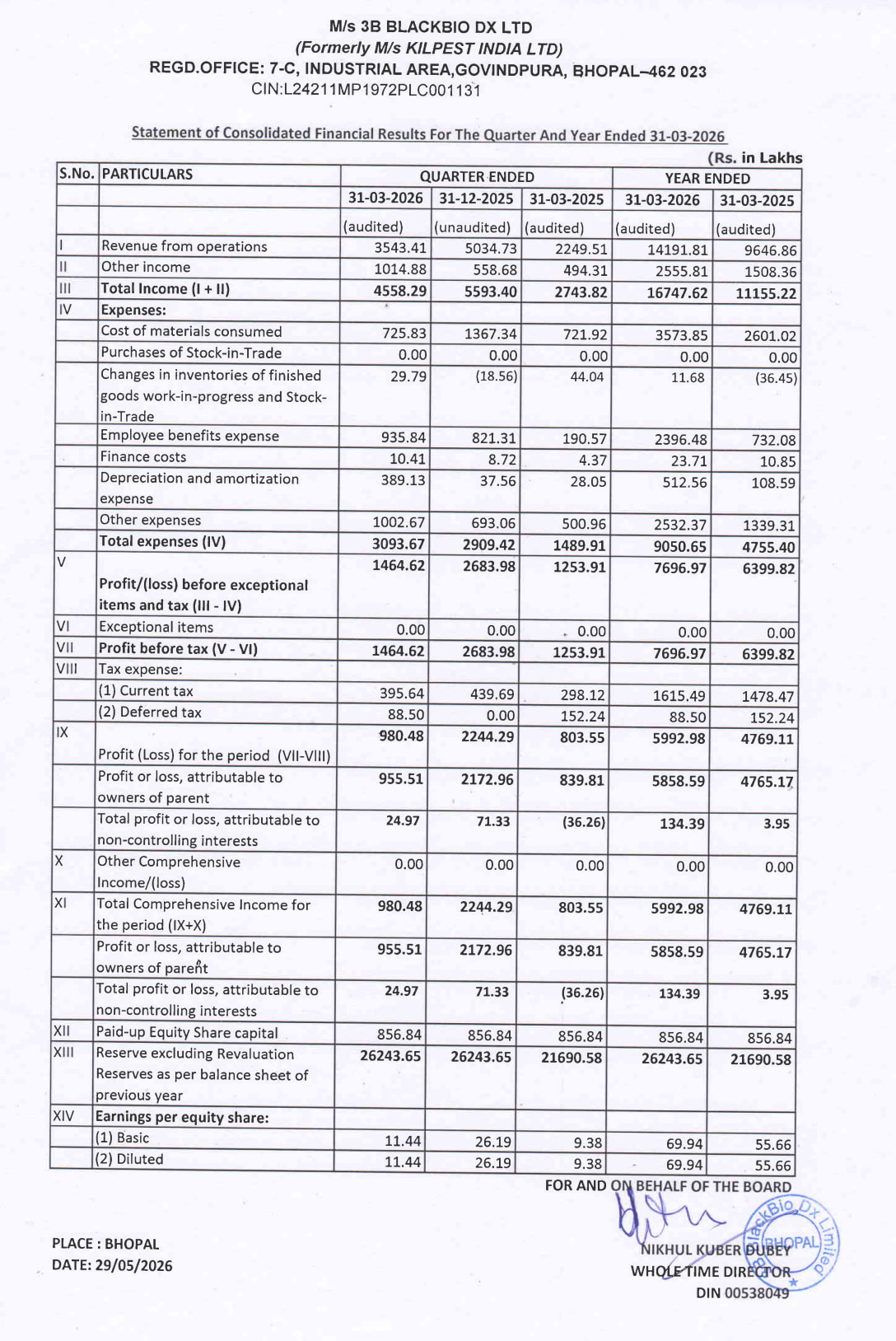

Results are out. Looks good at first glance, with solid top and bottom line growth despite Coris drag on margins. investor PPT mentions some impact of Gulf tensions but they have largely navigated things well. They are now sitting on 257 crore of cash!

4 Likes

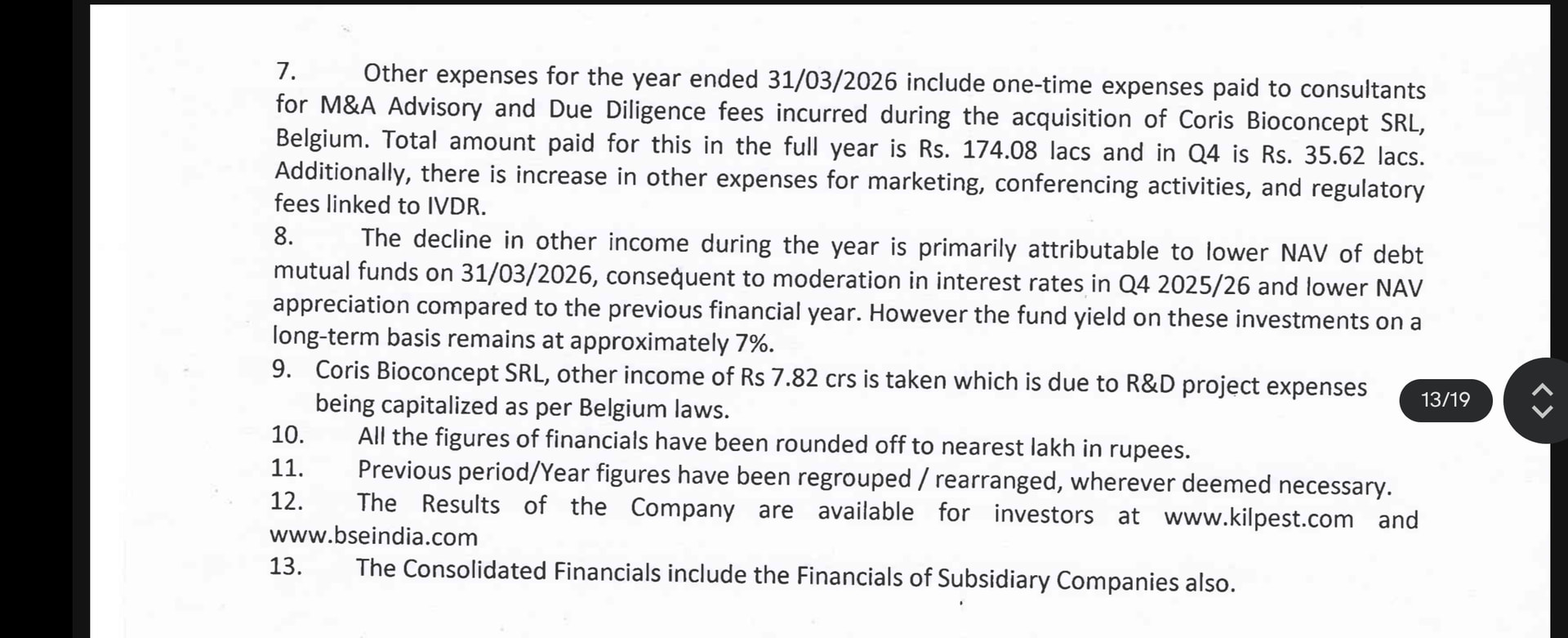

One very important finding at point 9

What they are saying is r&d expense is actually treated as other income in belgium, meaning that 7.82 cr is not some amount got by selling kits. This may or may not occur in the next year. That’s why if you check the coris whole year pat was substantially positive.

But I think this should be compensated with the non recurring M&A spends(around 2 cr) , debt mutual funds nav increase and so on.

Effectively next year they should do 30% sales growth, profit should probably be flat or very slight increase.

3 Likes

Yes one needs to remove any Coris profits from FY26 to normalize performance as they were only able to consolidate the profitable quarters post acquisition. H1 FY27 should be lower in terms of margins than H2 as these are Coris’s unprofitable quarters.

2 Likes

Did a rough projection for fy27

Assumptions :

Coris total sales for fy26 i took as 50 cr.

Trupcr Europe they haven’t explicitly mentioned the growth so I’m taking 25% since it is the fastest growth driver.

PAT growth will probably be in single digits.

1 Like

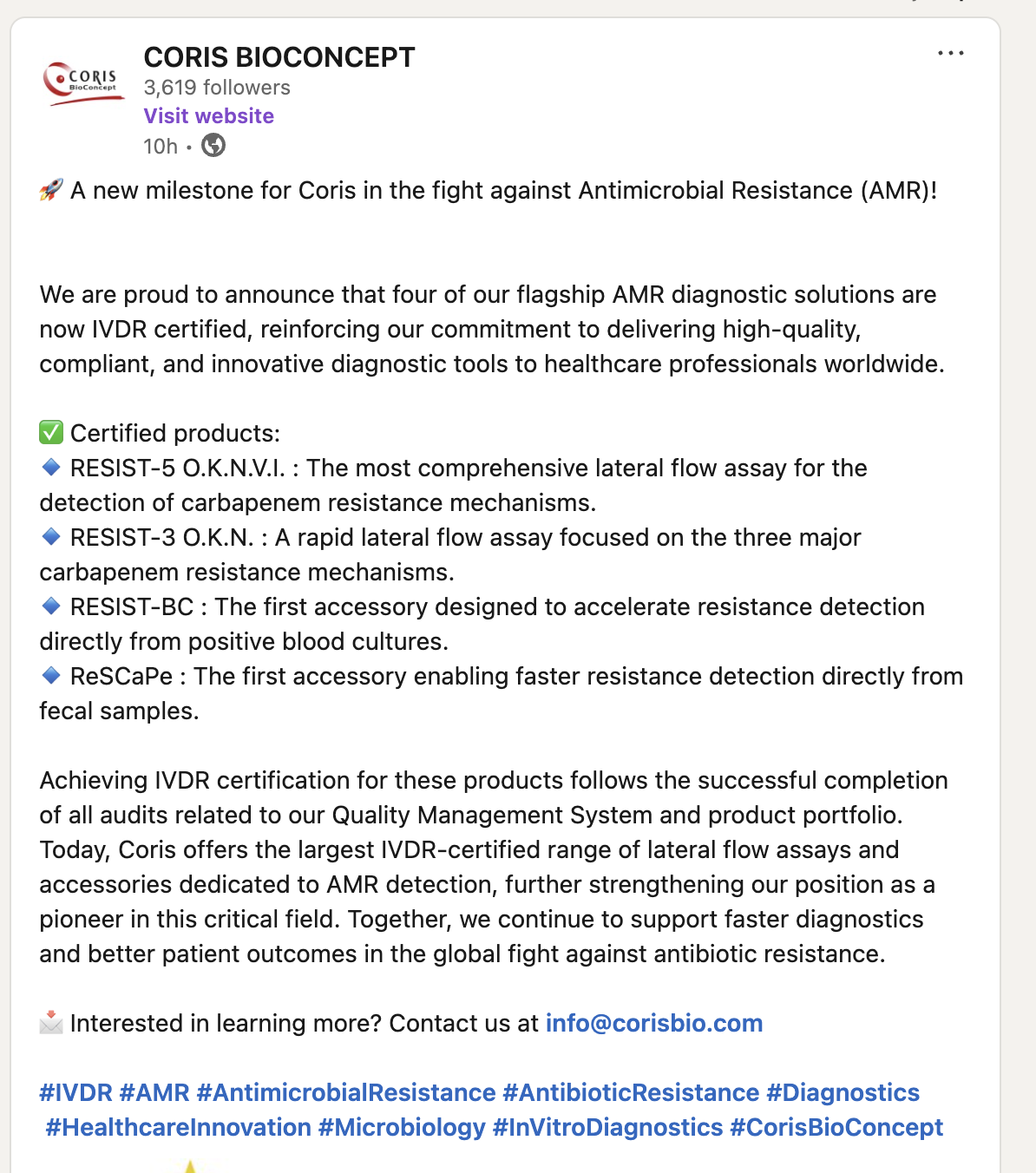

Coris announced yesterday that four of their flagship products have received IVDR certification. Under EU IVDR, the bar is materially higher than old IVDD/CE routes. Certification means these products remain commercially credible and tender-eligible in Europe.

13 Likes

The above revenue guidance holds.

Approx 175-178 Cr topline (25%![]() ).

).

PAT will probably come to 65-68 Cr (10%![]() ).

).

Should see another acquision in fy27.

Sample to answer will be live in Q3.

US FDA probably in fy28.

Will continue with same margins and maintain the market share(India) even with increased competiton and war.

Overall I think this was a positive concall.

10 Likes

Somehow I got a feeling of low TAM after the conf call. US FDA optionality from fy28 for only 100 cr market of AMR reagent. But I appreciate mgmnt to look for ways to increase shareholder value. They are moving to sample to answer device to increase TAM.I think the major market is in devices like these than reagents. Unless there is clear visibility of TAM , it won’t be assigned a reasonable PE

2 Likes

Their main objective is to bridge the gap of the hat order once it gets over by fy28. On an average, annually they are getting 15 cr from this order.

And the 100 cr tam being mentioned is only for 1 product (carba) that they are chasing the fda for.

I think once they get the fda, it should open opportunities for other products as well.

Also stock price appreciation will only occur once there is predictability in the business, now there are multiple moving parts. Unless everything comes together I don’t see the PE going beyond 20.

3 Likes

Can any one elaborate on other income standalone level they have reported 14 cr and consol level 26 cr. They have mentioned that 8cr of coris R&D has been entered as OI. then what abt the remaining 4 cr ? Cash flow statement is not providing any clue..

The Coris R&D Expense capitalisation (as per Belgian Law) explains majority of the Q4 OI difference-Standalone at 1.5 Cr and Consolidated at 10 Cr. The 4 Cr you are referring to is stemming from Q2 and Q3, could be related to exchange gains etc. We need the Other Income breakdown in the Annual Report to understand these.

1 Like

After Q Line Biotech, another SME IVD manufacturer Avience Biomedicals is coming out with an IPO this week. They are a Noida-based IVD consumables & devices company. Products include Covid, HIV, HBsAg, malaria, dengue rapid tests, serology products, biochemistry analyzers and reagents. Avience is mainly a trading company with 70% of revenue coming from trading products and 30% from manufacturing. One of the objects of the IPO is to expand their own capacities so they can product more inhouse and introduce newer products.

Basic comparison with 3B BlackBio –

Interestingly the IPO anchor book has some decent names including Sanshi Fund 1 (Mukul Agarwal), Meru Investment Fund, Fortune Hands Growth Fund, Shine Star Build Cap.

Still wondering what these investors see in Q Line / Avience that they don’t see in a market leader like 3B? Somewhat a failure of this management to not communicate their story well, though eventually the numbers will speak for itself.

8 Likes

There was no such bullish guidance regarding growth. It was just one person on the call trying to put words into management’s mouth while management made it clear multiple times that on a consolidated basis, they are looking at 15-20% topline growth and overall EBITDA margins would come down due to Coris being a negative EBITDA margin company still.

It wasn’t clear whether on consolidated basis, 3B margins would be 25% (same as Q4) or 40% (same as FY26) going ahead into FY27.

So more realistic expectation would be

FY27 rev: 165 Cr @17% growth

EBITDA: 65 Cr @40% margin

PAT: ~60 Cr (including other income) implying the forward P/E is ~17x

3 Likes