Use URL Party Name | National Company Law Tribunal (nclt.gov.in)

Select Indore Bench, case year 2022 and Party name ‘Kilpest’

2 Likes

Thank you so much. You are a gem

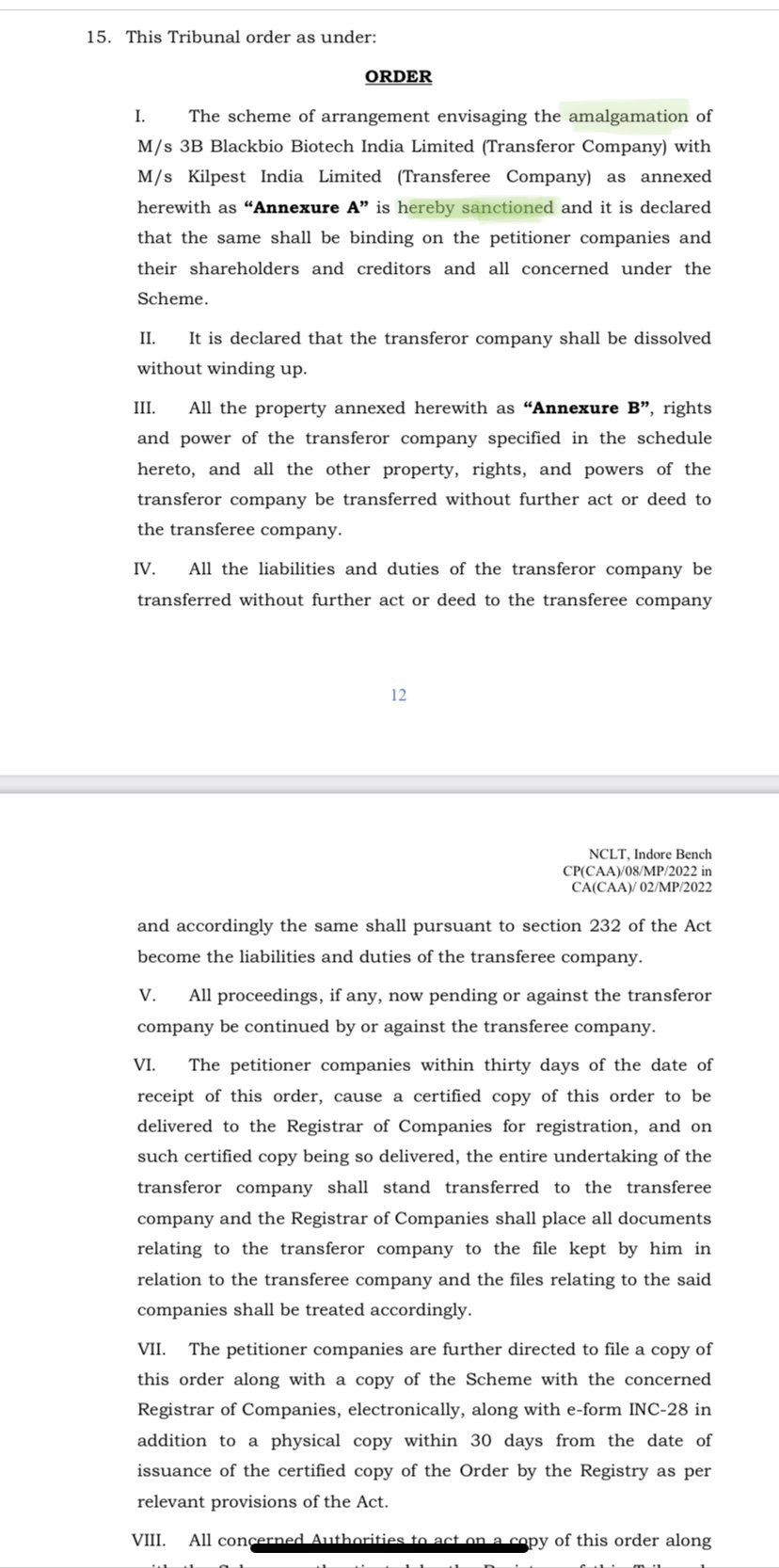

The Kilpest and 3B Blackbio Biotech amalgamation has been finally approved.

https://twitter.com/abhi16446/status/1688507241304068096?s=46&t=0tfc2Du9QmX2IMCgODtIuw

18 Likes

I have been tracking Kilpest through this thread on and off for the last one year without taking a very detailed look at it. With the amalgamation of 3BBB into Kilpest finally on the verge of happening, I decided to give this company a detailed read. Thanks to all the participants of this thread, this is one of the several amazing threads on micro-cap companies that only a platform like Valuepickr can have ![]()

Thanks to @Vineetjain111 I came across this company called Molbio Diagnostics (Molbio Diagnostics Pvt. Ltd.) which is in the same space as Kilpest - PCR based molecular diagnostics. The company is not listed and is valued at around ~$1.6bn (~13000Cr) at a 10x P/S multiple. Temasek and Motilal Oswal are existing PE investors in the company. The company is known for its TrueNat PCR platform which provides a portable end-to-end PCR solution from sample extraction to report generation for 40 different diseases.

One can see their TrueNat platform in action in this video where its being used for a Covid 19 test - https://www.youtube.com/watch?v=rPuSk4quQT4

If one wants to understand the science behind a PCR test (Polymerase chain reaction), these two animated videos are good for a first level understanding

Basically, a PCR test involves the following key steps:

- Identification of target DNA (part of the DNA that carries disease signature)

- RNA/DNA extraction from sample

- If RNA is extracted (in case of virus borne diseases), then use Reverse Transcriptase to convert the RNA to cDNA (The RT part of the RT-PCR test)

- The extracted DNA is mixed with primer, free nucleotides and Taq polymerase (an enzyme extracted from heat resistant bacteria)

- This mixture is put in a machine called a thermal cycler which multiplies the target DNA into billions of copies thus making detection possible

- In this concentrated sample of the target DNA, its presence or absence is identified via different probes for e.g. in the case of Covid 19 it seems to be a probe that causes fluorescence upon detection which is measured in the final mixture to give a positive/negative verdict.

The quoted report in this article (April, 2023) provides some important data points

Molecular Diagnostics Market in India is Expected to Reach US$ ~1.6 Billion by 2030, ET HealthWorld -

- Main use cases of MD - infectious disease detection like COVID-19, dengue, malaria, tuberculosis, influenza, HIV and hepatitis. Emerging areas - cancer detection, cardiovascular disease detection, neurological conditions

- Current market in India is just short of 1bn$ now and is expected to grow to 1.6bn $ by 2030 and 90% of the current MD market is PCR based, so that’s a market size of 1.44bn$ by 2030 (~12000Cr at today’s exchange rates)

- There are 3000 labs capable of doing MD tests in India now

- Key players in India - Molbio, Mylab and Tata MD. Large global players - Abbott and Roche.

Unlike Molbio, 3BBB seems to manufacture only the assays (primer + nucleotide + probe mixtures) and not the portable machines themselves. With that background, let me document a few open questions that I think we as a group needs to answer to nail down the long term potential of 3BBB:

-

Opportunity size for 3BBB - Of the current PCR market size of ~7000Cr, how much is from assays and testing (3BBB’s area) and how much is from diagnostic equipment (outside 3BBB’s purview)?

-

Why does 3BBB have such low market share even after being an early entrant? - 3BBB exists for more than a decade. Spain is a hotbed of biotech research, so the JV with the Spanish company was a step in the right direction in the early 2010s. But why does Kilpest only have a 50Cr market share in a 7000Cr market?

-

Business models of competitors - The likes of Molbio and Mylab both offer PCR machines in addition to assays and kits. Do they manufacture these machines or do they simply import them and sell under their own brand names? For a lot of pathology and radiology equipment, the machine is provided for free but the buyer has to buy a min amount of reagents/chemicals/kits from the OEM - is it the same arrangement for PCR machines and kits? If that is the case, then is a kit provider like 3BBB frozen out from diagnostic labs with Mylab or Molbio machines and only restricted to labs using imported machines like Thermofisher?

-

Product distribution and penetration in India - What is the buying behaviour of Indian labs and hospitals? Do they prefer to buy kits from OEMs who make machines or are they open to buying kits from a provider like 3BBB?

-

Can 3BBB move into PCR machines? - If players like Molbio/Mylab are simply importing or outsourcing the manufacturing of these machines, what prevents 3BBB from doing the same?

-

Finally the most important question - Does 3BBB’s business have any real barriers to entry? During Covid, 532 RTPCR kits were approved by ICMR as of Feb 2022 (https://www.icmr.gov.in/pdf/covid/kits/RT_PCR_Tests_Kits_Evaluation_Summ_17022022.pdf) of which at least 200 were manufactured by domestic companies. If any Tom, Dick and Harry can make Covid 19 RTPCR kits so easily, what barriers to entry does 3BBB actually have wrt kits for other diseases?

Tagging the erstwhile active contributors in this thread - @Vineetjain111 @sahil_vi @aga.ayush11 @ravish @Anand6 @msandip @enelay

20 Likes

Total molecular diagnosis market size 6000 cr in india, which includes PCR NGS Arrays etc. Reagents 50-60% of it, and PCR may be 50% (excluding POC tests where 3bbb has no presence) – 2000 cr opportunity size roughly. Excluded Rapid ELISA tests in this, so I might be totally miscalculating this. Others please confirm.

–Indian market (kilpest has export opportunities too), 3bbb has not covered all possible PCR tests, so adjustments needed in this.

Market is competitive and dominated by MNCs.

In a lab, PCR tests costs 1500-2000 or higher and kit CPT (cost per test) is 20-30% of that on an avg. So doctors don’t switch just for cost (covid was exception)

In pathology, two types of machines - Open system and close system.

3bbb makes kits for open system machines.

While Molbio is chip based close system PCR - POC machines mainly used in Gov hospitals to diagnose TB. 4 slot machine usually where u can’t use other cos’ kits.

I mailed management in past regarding such close system POC machines (PCR based, immunofluorescence based) that can be usuful especially at rural levels, but he was not much interested.

I am not sure, but molbio has given order to dixon for some machines.

No meaning of moving into Open system PCR machines as it is dominated by big R&D MNCs. Close system Point of Care (small machines) is only option which Mr Dubey was not ready to explore as it needs whole new talent and team in R&D.

Maintaining quality in whole spactrum of tests and supply as per demand are strengths of 3bbb. Otherwise, not high entry barrier business.

Holding some Free of cost.

16 Likes

About an year ago Kilpest entered into some kind of arrangement with a Singapore based company named Vela Diagnostics to sell their equipments in the UK. There has been no update from management since on how this business is doing.

Disc.: invested

2 Likes

The following is the excerpt of a scuttlebutt discussion I had with a doctor who owns two pathology labs (block and district level) and has been an investor in Kilpest.

- During Covid we saw that many Indian and Asian manufacturers of Covid kits emerged after the initial days and the space got commoditised. This makes me question - how much of a scientific moat is there for a molecular diagnostics-based kit maker like Kilpest? As the MD market grows in India, will this space get more and more crowded thus presenting a growth and ROCE challenge for Kilpest?

- Nothing like moat in PCR kit, USP is handing small volume orders efficiently. When covid type demand exists, where co is not bothered about selling small quantities and finding buyers, many can jump in due to scale but handling multiple SKUs (tests) with small quantities is not an attractive proposition for many. MNCs are themselves a crowd, but with higher pricing points than 3bbb, so 3bbb won’t be affected much

- What are the key drivers of demand in molecular diagnostics space in India?

- Mainly demand is derived from two sources with roughly equal split (not entirely sure about split)

*o Govt actively using MD in TB, HIV, Hepatitis B/C *

o Private diagnostics labs mainly using it in oncology and NGS (We can say NGS is a multiple PCR running simultaneously in one test – a different machine is needed for this). 3bbb is mainly associated with oncology and private part. Now govt is also coming up with oncology labs and hospitals, so Govt may also start driving this demand

- Given Kilpest has no capability for making PCR machines and apparently no intention to go into machines, what is the effective market size for Kilpest within the 3-3.6k Cr reagents/kits space? Is this market size shrinking by the day as closed systems gain share or is it expanding?

- I don’t think closed systems can gain market share in a big way besides the CBNAAT (PCR) Molbio. I don’t understand why govt is using Molbio type machines at district level hospitals. Closed system machines are for lower volume of patients at block level hospitals but Govt. is using them for district level hospitals too. Open system big machines are more favourable and I trust them more as a doctor

- Can you help me understand a little what is the actual scientific value addition that Kilpest does? Which of the components of PCR testing - nucleotides, primers, polymerase, DNA isolation, RNA to cDNA - is made in-house by Kilpest? What chemical/biological material does Kilpest buy from its suppliers and which kind of companies supply them? (Is it enzymes? Do companies like Laurus Bio supply to Kilpest?). Is there any scope/logic/possibility for Kilpest to backward integrate into chemicals/biological materials that it buys from suppliers?

- PCR is used to identify a particular target genome available in sample or not and then it can quantify it too in terms of concentration in the sample like per cubic ml, per cubic ul etc. I think Kilpest makes only buffers in house. One possibility is that, it is making sequences of nucleotides (reverse of the target RNA for binding) by itself by buying nucleotides separately and then using own PCR machine to amplify them. This is a very remote possibility however and there is no moat in doing this. Kilpest is mainly an assembler. Usually cos like Syngene, Laurus Bio make these biological entities/enzymes by fermentation which uses e coli and other bacteria to replicate needed sequences, called recombination techniques, a biotech subject about which I have no in-depth knowledge. The cloning of foreign DNA in Escherichia coli episomes is a cornerstone of molecular biology. The pioneering work in the early 1970s, using DNA ligases to paste DNA into episomal vectors, is still the most widely used approach

- Kilpest is talking about scaling up their PCR business in UK. What is your outlook about that business and its growth possibilities? Will Kilpest be the lowest cost producer/importer there? What drives contract wins in UK - is it cost and quality driven or are there other factors like certification etc. which act as barriers to entry?

- I think 3bbb will gain some market from MNCs in these export markets if they are able to maintain qualities like low false results, cold chain etc.

- Speaking to long term investors in Kilpest gives me the impression that management is either unwilling or incapable of taking the required steps to expand this business meaningfully. With its current strategy, can Kilpest grow its molecular diagnostics revenues from 50Cr to 200Cr in 5 years (30-35% CAGR)? If that is not possible, what needs to change in Kilpest for it to grow at that rate?

- I am aware that people have suggested to promoters to investigate closed systems-based hormone machines to test for Thyroid, Vitamin D, Beta HCG, PSA, HbA1c and other hormones at block level as logistics from block to district takes its own time (6-10 hours) and patients are always in a hurry and are ready to pay some premium for instant reporting. But management doesn’t seem too keen to tap into such opportunities, perhaps its too much to expect a company of Kilpest’s size and capabilities to be this agile or ambitious. The PCR based oncology market in India seems to be growing at 25-30% CAGR. But the kind of growth you are suggesting can only happen via exports if they can provide cheaper but and at the same time, high quality PCR testing alternatives to MNC kits for diagnostic labs and hospitals in UK and other geographies.

Disc: Invested recently, trying to form a view on long term potential.

22 Likes

3B BlackBio Non-Covid sales for last 4 year (From kilpest annual report).

74% Growth in FY22, 66% growth in FY23.

Export revenue (Including Covid)

“Real business” numbers for this company are quite impressive. How well they can scale and to what level of revenue is a big question yet to be answered. But growth trajectory is outstanding.

14 Likes

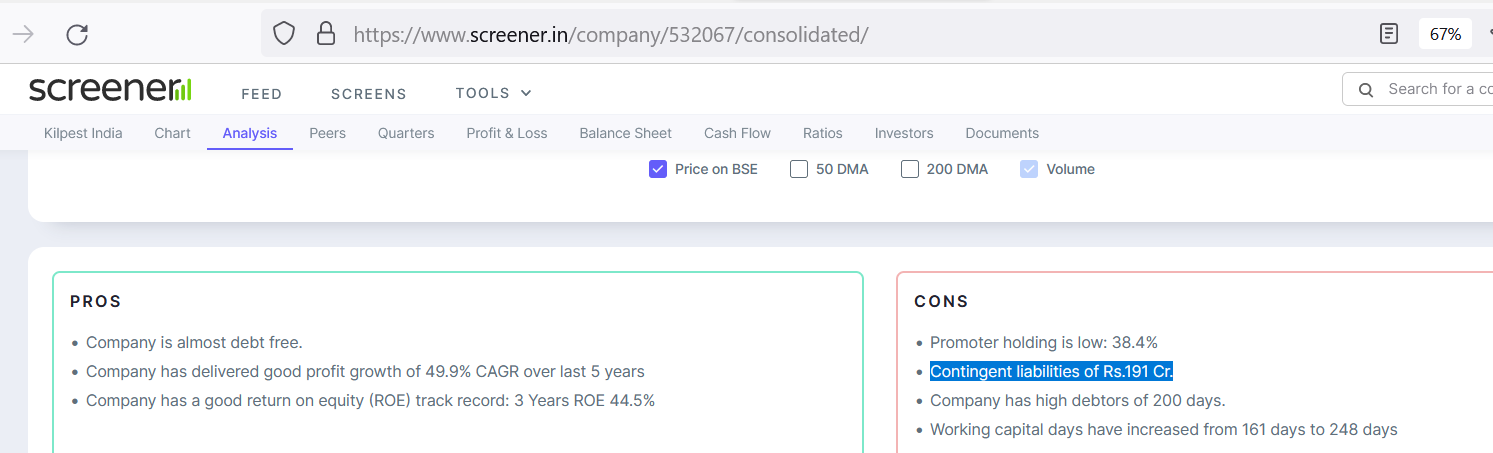

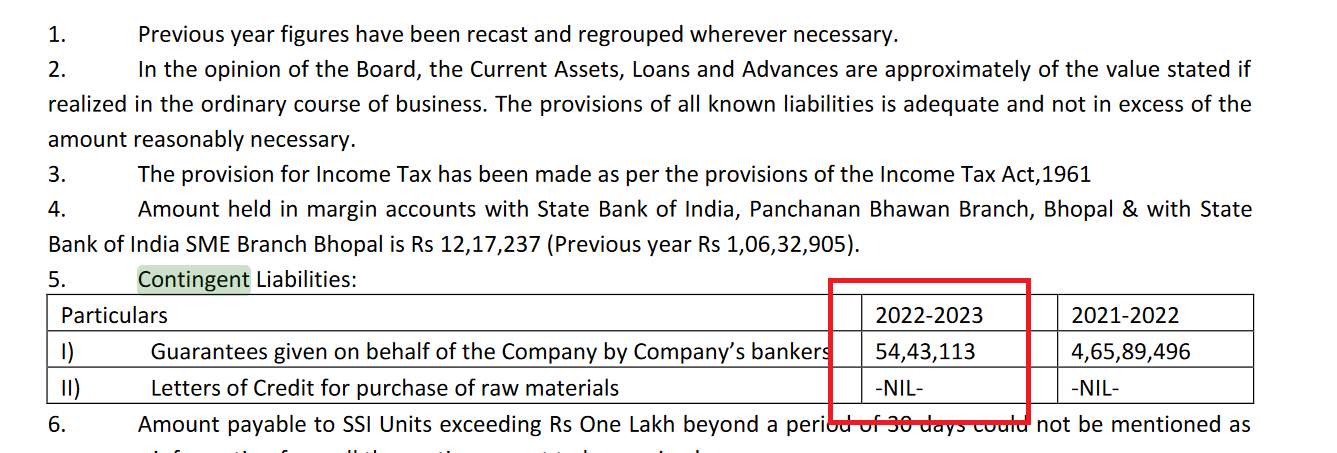

Can someone please help me with this query:

Screener shows a contingent liability of 191 Crore:

Whereas FY23 AR shows a contingent liability of 54 L

What is the source of information for Screener? Can I conclude that the number on Screener is incorrect?

Thanks

Update: the issue has corrected on Screener

1 Like

https://www.nuvamawealth.com/research/stock-specific-reports-1/kilpest-india--the-cub-series-e69ee0

Disc.: invested

4 Likes

On the surface, the estimates look very conservative and they still arrive at a healthy upside. Anyhow, comparing PEs to diagnostic labs makes no sense - in fact they’ve assumed half of the avg PE of players like Dr Lal to arrive at their targets. In my view, this is a much better business with much lesser competitive intensity and margin pressure.

I wish they had explained the basis of their growth assumptions. Also, any utilization of the massive cash pile for inorganic growth will be a big optionality. Very good to see Kilpest interacting with institutions - this seems to have stem from the meetings they held earlier in the month. Looking forward to more reports and hopefully some more communication with investors. The AGM may be a good opportunity to ask more questions.

Disclosure: Invested with about 15% of PF at cost (avg price is in the 450s), it has grown to well over 20% of PF with the recent run up.

6 Likes

13acbbf6-9677-4840-8333-c2489ec73e96-1.pdf (1.3 MB)

^ here is the report from Nuvama

1 Like

I hope there is someone in this thread who has registered themselves as a speaker for tomorrow’s AGM and can ask the following set of questions asked by Nirvana.

Kilpest FY23 AGM Notes

- Business growth and addressable market size

- FY24 outlook

- Guides for 25-30% growth in Molecular Diagnostic division

- Hoping for 12-15% export growth. Export business cannot grow faster because its regulated and approvals take time

- Hopes to maintain EBITDAM between 50-60% although competition in real time PCR is increasing

- Real time PCR market - PCR market new competitors are coming in and prices are going down in India

- Domestic addressable market in molecular diagnostics for 3BBB is ~300-500Cr, growing at 10%. 3BBB is only into open system kits/reagents. They have no plans of going into PCR machines. Currently not much demand for PCR machines, most machines were sold during Covid itself. Most hospitals already have machines installed

- 3BBB hopes to grow at 25% in this market on the back of

- TRURAPID launch for anti-microbial resistance testing – TRURAPID is awaiting some regulatory approvals, has already started contributing in FY23 revenues. 3BBB has to develop the market for AMR in India

- TRUNGS NGS business will start contributing from FY25 (NS1, Dengue) – Have launched one panel and will be launching another soon. NGS will become a competition for real time PCR in time. NGS market is nascent in India but will grow.

- Exports

- FY24 outlook

- Competitive advantages

- In house enzyme production (Did not specify what components of PCR testing they make in-house)

- Large product portfolio and quick response to customers are advantages that company has – 24/7 technical support, customer centric approach

- Strong, well-known brand

- Capital deployment

- M&A only if target valuations and IRR is met (Target IRR is > 10%)

- Will consider buyback after FY24 if M&A does not go through by then

- Others

- NSE listing will take time as share capital of the company has to increase – will take up post amalgamation

Disc: I exited after a quick trade (Prematurely, as it turned out) for now as I couldn’t see any lasting science based moat in 3BBB.

14 Likes

be157467-7ee2-4d20-9d75-86c63f4e80f4.pdf (948.4 KB)

AGM presentation

5 Likes

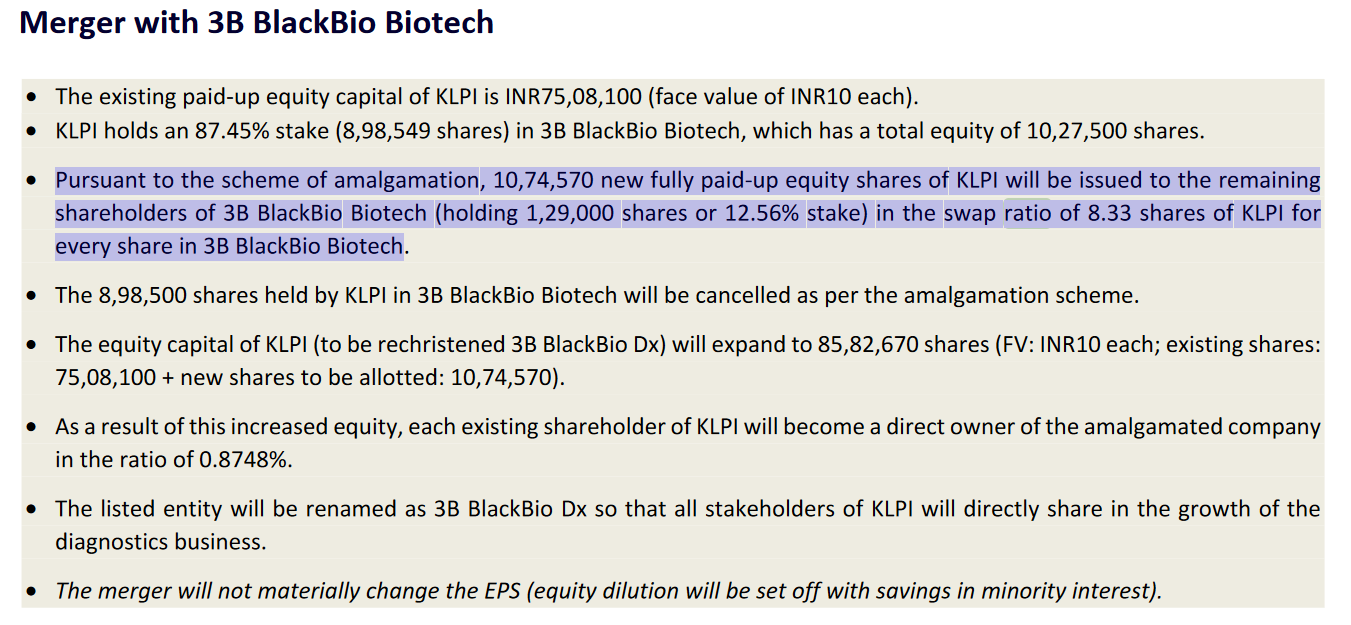

Would anyone know what is the ratio of 3BB to every share of Kilpest?

So for every share of Kilpest in our account how many shares of 3B Black Bio will we be getting?

Believe, the new fully paid up equity shares will be issued only to remaining shareholders of 3B BlackBio Biotech. Thus, there should be no change in the number of shares of existing Kilpest shareholders.

Believe, this also means that the eps will come down as the TTM earnings remains same and number of fully paid up shares increase. May be that is why stock price is falling.

2 Likes

Additional shares will be issued to the minority shareholders of 3b. This will increase the number of equity shares of kilpest,however eps will not be impacted as earlier it was calculated without 3b minority interest. In summary, it is a non event for kilpest eps.

4 Likes