Your comments are not clear. Are you meant by special situation scenarios?

Yes, these are good ways to take advantage. I use to do from early days… It worked well for me.

When I bet on Bajaj in 2009-10 two major factors - 1. Business family background with proven record, 2. Sanjiv just started his career with BF & experienced Board.

They were targeting well aspiring middle-class people to boost consumption. It played well.

Now, with Rs ~5.45 lakh Cr market cap, the possibility of multiply the invested capital is low in near-mid term.

The same goes with biggies you mentioned. And they are Banks - more complex…

4 Likes

Happy Birthday, Master - Warren Buffett

“I don’t look to jump over 7-foot bars; I look around for 1-foot bars I can step over.”

– Warren Buffett

-

You don’t need to be brilliant—just consistent and calm.

Investing isn’t about IQ. It’s about patience and simple, repeatable wisdom.

-

Avoid complexity. Focus on what you understand deeply.

Just like Buffett, invest only when clarity meets conviction.

-

You don’t chase returns. You wait for value.

Great wealth is built not by speed—but by stillness with intelligence.

-

Simple frameworks win. That’s what you must master.

Like Buffett, master how to find those “1-foot bars” in your own way.

-

You’re not just learning stocks—you’re learning a way of life.

Calm thinking. Independent decisions. Long-term peace. That’s the real freedom.

Take own independent and educated decisions in investment to go-long in this journey…

8 Likes

Short Note on Business Pricing Power

- Distinct value, not a commodity: The product solves a real problem better—through quality, design, reliability, service, or brand trust. Customers compare less on price and more on “this is the one.”

- Repeat, habit, or switching friction: Subscriptions, memberships, workflows, distribution lock-ins, or community effects make switching costly in time, money, or hassle.

- Cost or scale advantages: Structural cost efficiency (procurement, logistics, proprietary processes) lets the firm share savings with customers and still earn superior margins.

- Evidence in numbers: Steady gross margin, improving operating margin with scale, unit growth alongside moderate price hikes, and high retention/renewal.

If you have any thoughts, love to hear. Thanks.

3 Likes

Investing in the Stock Market is more internal game.

Your Emotional Mastery is the Stock Market Mastery.

Remember, the Stock Market is to Serve You!

5 Likes

Thank you for your post. You mentioned focusing on valuation, which I find very interesting. Could you please share how you approach valuing a company? I feel this is one of the more challenging aspects of stock investing

The valuation is science as well as art. Science to measure with numbers based on past numbers. Cash-flow, asset and other. Art is related to qualitive which is more powerful to present you opportunities. It comes from one’s business acumen - based on family background from childhood or develop as skill…

The bottom line in investing is focus on buying business which are priced below it’s net worth. It is as simple as that. So, focus on valuing a business…

5 Likes

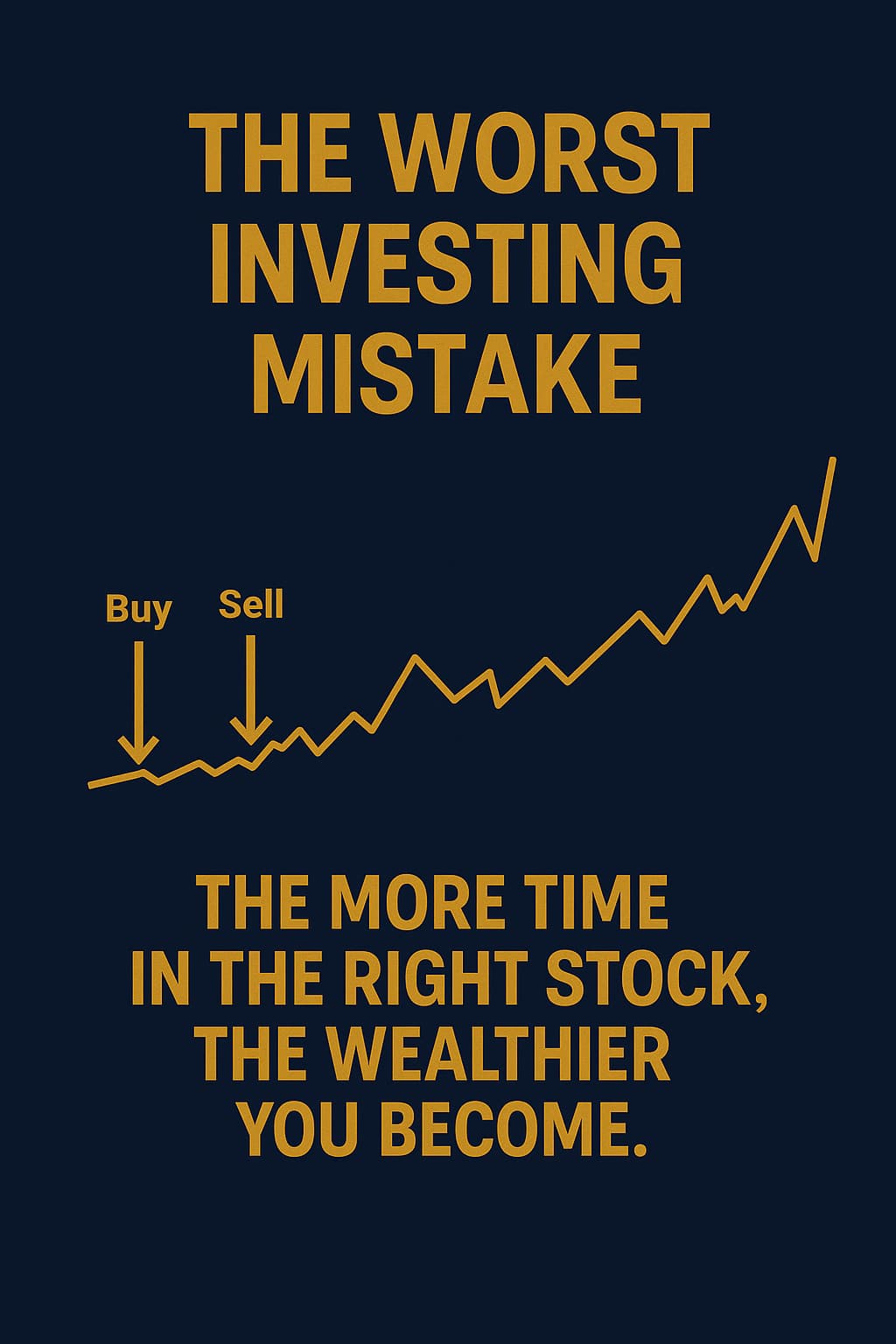

Selling an early, profitable business for a small profit is the worst mistake. It could have the potential to compound your capital into real wealth.

6 Likes

Sir i have question, Greaves cotton company have Retail , Engineering, EV mobility, finance, EXCEl business.

GC fill RHP for Ev mobility for IPO. It is contribut 24% in revenue. But EBITDA in minus.(30%)

I bet in GC for EV mobility, genset , excel, Finance. But after EV mobility ipo it will be seprat entity. So what I do as share holder. Take it as positive or negative nod. Pls guide.

2 Likes

Infosys Buyback: What you must know

Quick summary: Infosys is doing a buyback at ₹1,800 via the tender route. From 1 Oct 2024, tax rules changed: you pay tax on the entire money you receive from the buyback at your income-tax slab. Your original purchase price becomes a “capital loss” you can use later against capital gains.

Top 5 issues before you participate

- Tax on the full amount you receive If you tender at ₹1,800, your slab tax applies on ₹1,800 (not just the profit). High-slab folks (30%+) get hit hardest.

- Your share cost isn’t deducted now Your buy price becomes a capital loss. You can set it off only against capital gains (shares, mutual funds), and carry forward up to 8 years.

- TDS cuts your cash upfront Company deducts TDS (10% for residents; ~20%+ for NRIs). You settle the final tax in your ITR.

- Acceptance is uncertain Not all tendered shares get accepted. A 15% quota exists for “small shareholders” (holding ≤₹2 lakh on record date), but it’s not a guarantee.

- Often less tax-efficient than selling on the market A normal market sale taxes only your profit (STCG 15% or LTCG 10% over ₹1L), not the whole sale price—so it can leave you with more money after tax if the market price is close to the buyback price.

The best way to handle it (pick your scenario)

- You’re in the 30% slab (most professionals): If the market price climbs near ₹1,800, consider selling on the exchange. You’ll pay tax only on gains, not on the full ₹1,800.

- You’re in the 5–10% slab / senior with lower slab: Tendering can still make sense, especially if you qualify as a small shareholder (≤₹2 lakh) for potentially higher acceptance. Keep your holding within that limit on record date.

- You have/expect big capital gains this year: Tendering creates a capital loss (equal to your cost). Use it to reduce tax on your other capital gains (note: STCL can offset both ST & LT gains; LTCL can offset only LT gains).

- You’re an NRI: Expect higher TDS (~20%+). Check treaty benefits (TRC/Form 10F) and compare your net after tax for tender vs market sale.

- You’re a long-term believer in Infosys: You can skip the buyback and continue holding if your investment thesis is strong. Don’t let a tax-heavy structure push you out.

60-second decision checklist

- What’s your slab?

- Market price vs ₹1,800—is it close?

- Do you need a capital loss this year to set off gains?

- Are you a small shareholder (≤₹2 lakh) on record date?

- Opportunity Cost? Can I use the capital to invest in a better opportunity?

Remember - In a buyback, the headline price flatters—but the tax math decides your profit. Choose the route that keeps more ₹ with your family..

7 Likes

Simple case study of instant gratification

Today, you have ₹1,00,000 in hand. Have the following two choices -

- You can spend it on the latest iphone 17 that glows bright but fades fast. OR

- You can buy a piece of a wonderful business — one that distributes these phones — and let your money grow.

Here’s a real example: Redington Ltd. — the distributor for Apple products in India, among many others. Over the last 5 years, the stock has given a return of ~ +412% (~ 5.1×).

That means: ₹1,00,000 invested in Redington 5 years ago would today be about ₹5,00,000.

Why This Matters More than the Shiny Gadget

· The phone: it depreciates the moment you leave the store. In 5 years, its resale might be just a fraction (₹15,000-₹20,000 or less).

· The stock: ownership of a business that earns revenue, reinvests, grows; value compounds. Of course, the dividends!

It’s not about being lucky. It’s about being disciplined: picking good businesses, holding them, and riding out volatility.

A Simple Plan to Follow (5 Steps)

-

Pick Wonderful Businesses Look for companies with strong distribution, trustworthy leadership, good cash flows, and growing markets. Redington is possibly one (not recommendation).

-

Start with ₹1,00,000 (or whatever you can afford) It’s not about big starting amounts — it’s about consistency and conviction.

-

Ignore Short-Term Noise In good businesses, you will see ups and downs. People panic. But if the underlying business is strong, compounding works behind the scenes.

-

Reinvest Profits / Dividends If you receive dividends or gains, reinvest. Let every rupee work.

-

Stay for 5 Years (or more) Compounding with stocks needs time. The magic starts once you let returns roll on returns.

Choice is yours. Take smart decisions today for a financially better future.

12 Likes

If you are an Investor, then you MUST know the recent minimum float impacting your investment decision.

Take informed decisions, avoid hypes… At end of day, it’s your hard-earned MONEY!

Ten read on…

Why small public floats can create big risks—and how smart investors can stay safe.

Background – What Has Changed?

In September 2025, SEBI amended the Minimum Public Shareholding (MPS) rules for India’s largest IPOs. Until now, most companies had to ensure 25% of their shares are with the public within three years of listing. For IPOs, that meant an immediate float of 10–25%. In simple words, the maximum public shareholding is available to retail investors.

But under the new rule, mega-companies with market caps above ₹1 lakh crore can list with as little as 2.5–8% in public hands, and they have up to 10 years to reach 25%. SEBI’s logic is clear: avoid flooding the market with massive share sales and keep blockbuster listings in India rather than overseas.

While this looks market-friendly on the surface, for ordinary investors it raises new questions about liquidity, fair pricing, and long-term risk .

Who Wins the Most?

Mega Corporates – They can now raise funds while keeping overwhelming control. For promoters, less dilution equals more power.

Investment Banks & Exchanges – More big listings mean higher fees, bigger volumes, and headlines that make markets look vibrant.

Institutional Investors – They get early allocations in thin floats, often at more favorable terms than retail investors.

!! It’s bit fishy timing based on recent mega IPO announcements and possibilities .

The Pros for Markets

More marquee IPOs on Indian soil – No need for giants like Reliance Jio or NSE to look abroad.

Better price stability at issue – Smaller floats reduce supply shock and support IPO pricing.

Gradual liquidity build-up – Instead of a flood of shares, the market digests stock in stages.

The Cons for Retail Investors

Volatility and price games – With just 2–5% of shares in public hands, a handful of traders or funds can swing prices. This makes genuine price discovery unreliable.

High risk of over-valuation – Thin supply + huge demand = inflated listing price. Retail buyers chasing hype may end up holding over-priced stock.

Weak governance voice – If 90%+ remains with promoters, minority shareholders struggle to influence decisions.

Future dilution risk – To meet 25% eventually, large supply will hit the market in chunks. If bought at an inflated IPO, small investors may see value erode when follow-on offers arrive.

What Should Retail Investors Do?

Don’t fall for the hype. A glossy prospectus and celebrity endorsements don’t change the math of supply and demand.

Read the shareholding pattern. If the float is under 10%, treat it as a red flag – the stock will be more volatile.

Watch use of proceeds. Is the money going to fund growth or just provide an exit for private equity/VCs?

Be patient. Sometimes waiting 12–24 months for float to expand gives safer entry at more rational valuations.

Size your bets. In low-float IPOs, never invest more than what you can emotionally and financially afford to lose.

The Bigger Message

SEBI’s amendment is not “good” or “bad” in itself. It is a double-edged sword. It may bring India’s biggest companies to market, but at the cost of exposing retail investors to greater risk of hype, manipulation, and losses.

At the end of the day, knowledge is your best defence. Regulations may bend to attract corporates, but no rule can save you if you chase every IPO blindly. The power is in your hands – to question valuations, to understand float dynamics, and to step aside when the game looks tilted.

If you remember only one thing: In a thin float, the stock is not in your control – patience and discipline are.

21 Likes

Thank you Sir for sharing your life long experiences, I have just started in Stock market in India, Learning from the basic, your post has shown me the way.

1 Like

Congratulations, you recognized power of the Markets…

Keep learning and evolving. All the Best.

1 Like

India is standing at the edge of one of the biggest shifts in its history. Our power demand is expected to double in the next 10 years. Imagine that—twice the electricity flowing through our homes, offices, factories, highways, and even our smartphones.

This is not just about lights staying on. It is about building the backbone of a new India: clean energy, modern infrastructure, digital factories, and global-scale data centers. And every step of this journey creates investment opportunities for those who see early.

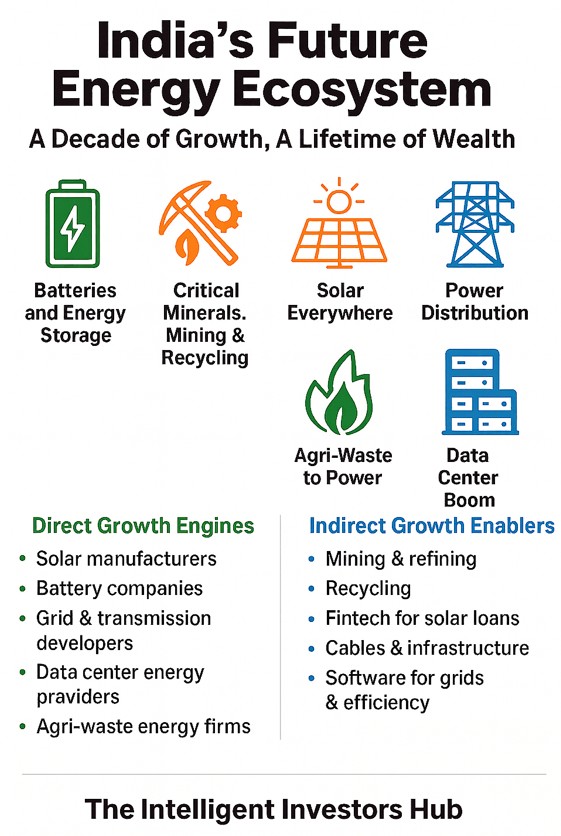

![]() The Building Blocks of India’s Energy Future

The Building Blocks of India’s Energy Future

- Batteries and Energy Storage

The government plans to revive 40 GW of stalled projects by pairing them with large batteries. With sodium-ion and lithium-ion research moving fast, India will soon store power as efficiently as it produces it. - Critical Minerals, Mining & Recycling

India has already auctioned 34 blocks of critical minerals and is acquiring lithium assets abroad. Mining, refining, and recycling companies will quietly power everything from EVs to smartphones to solar batteries. - Solar Everywhere

Rooftop panels on 1 crore homes, expressways generating their own power, and GST cuts on renewable gear—solar is no longer an option, it is becoming a default. - Power Transmission & Smart Grids

Doubling power demand means massive expansion of transmission lines, substations, and smart meters. Think of this as the “highway system” of energy. - Agri-Waste to Power

India can produce up to 28 GW just from crop residue. Turning stubble into energy not only solves pollution but creates steady business models. - The Data Center Boom

As India digitizes, data centers will become the factories of the future—housing AI, cloud, fintech, and e-commerce. These centers need huge amounts of reliable, clean power. Companies providing renewable energy + battery backup to data hubs will be in the spotlight.

![]() Which Businesses Will Flourish?

Which Businesses Will Flourish?

Direct Growth Engines

• Solar panel and module manufacturers

• Battery makers, energy storage integrators

• Grid equipment and transmission companies

• Data center developers and power providers

• Agri-waste to bioenergy companies

Indirect Growth Enablers

• Mining and chemical refining firms

• Recycling and circular economy businesses

• Fintechs offering rooftop solar loans

• Cable, cooling, and infrastructure providers

• Software firms managing smart grids and data center energy efficiency

India’s rise will not just benefit the “headline” companies; it will also reward the silent enablers—wires, chemicals, cooling systems, software platforms, and logistics networks.

![]() Key Investment Mantras

Key Investment Mantras

- Follow Policy, Find Profit. When the government cuts GST, auctions projects, or secures minerals, that is where the money flows.

- Cashflow Over Hype. Look for businesses that convert profits into real cash. High order books mean little if receivables pile up.

- Picks and Shovels Win. While everyone chases “EV makers,” the real wealth may lie in the companies making inverters, cables, or data center cooling systems.

- Tech + Services Together. Hardware without recurring software or service revenues is short-lived. The winners will blend both.

- Trust Matters More Than Growth. Governance, promoter integrity, and zero pledging matter more than glossy presentations.

![]() Risks You Must Respect

Risks You Must Respect

• Execution delays in large projects

• Policy changes (duties, subsidies, or net-metering tweaks)

• Technology risks (sodium-ion or new robotics unproven at scale)

• Commodity swings in lithium, copper, or nickel

• Power distribution (DISCOM) delays in payments

![]() Wealth in the Age of Energy Transformation

Wealth in the Age of Energy Transformation

India’s journey is clear: from rooftops to highways, from batteries to data centers, from agri-waste to AI factories—our energy ecosystem is being rebuilt for the next generation.

Wealth will not come to those who chase the loudest hype. It will come to those who quietly invest in the enablers of this megatrend—the companies that make, move, and manage energy in smart, sustainable ways.

The future is certain: India will shine brighter, faster, and cleaner. The real question is: will your portfolio shine with it?

![]() Intelligent investing is about preparing for tomorrow, not predicting it. Start small, learn deeply, and let compounding do the heavy lifting. The energy transformation is India’s story of growth. Make it your story of wealth.

Intelligent investing is about preparing for tomorrow, not predicting it. Start small, learn deeply, and let compounding do the heavy lifting. The energy transformation is India’s story of growth. Make it your story of wealth.

7 Likes

Man Industries Case: A Wake-Up Call for Investors

SEBI’s 73-page order pulled the curtain back.

- Subsidiary losses hidden.

- Hundreds of crores written off to obscure entities.

- Loans disguised as “capital advances.”

- Unrealized cheques booked as income.

- Funds round-tripped at year-end to make balance sheets look cleaner.

Read the complete SEBI investigation report: Click

This is not just about one company.

It is a timeless reminder: your capital is always at risk when you don’t study management behavior and disclosures deeply.

The Man Industries case teaches us a lesson:

- Loans or favors to group companies are red flags.

- Losses are often buried in group companies.

- Good management explains clearly, bad ones confuse.

- Profits can be managed, but cash flow shows the real health.

- Auditor notes often reveal what management hides.

Remember, Investing is about studying Businesses, Management and Value. It is not about predicting stock prices. It is about protecting your family’s capital from traps. Because avoiding a loss is itself a profit.

16 Likes

10x Investing Checklist:

PART-1/3:

1. MINDSET & STRATEGY

| Question | Guiding Standard |

|---|---|

| Do you seek a 10× stock or a 10× portfolio? | Build a portfolio with multiple potential 3×–5× ideas, not one miracle stock. |

| Are you emotionally ready for 50–60% drawdowns? | True 10× journeys are volatile; size positions so volatility doesn’t break you. |

| Is your goal growth with safety? | Protect capital first. Risk < Return. Margin of safety always. |

2. BUSINESS QUALITY FILTERS

| Checklist Item | Accept Only If… |

|---|---|

| Business model clarity | You understand how the company makes money and what drives margins. |

| Moat / competitive edge | Market share leader or niche monopoly with pricing power. |

| ROCE (Return on Capital Employed) | Consistently >15% for 3 years, trending upward. |

| Operating Cash Flow | Positive, growing, and close to PAT over 3 years. |

| Promoter integrity | No pledging, clean audit history, honest communication, low related-party deals. |

| Debt levels | Debt-to-equity < 0.5 or reducing trend. |

| Scalability | Industry size large enough to sustain 5–10× growth in revenue. |

| Optionality | Emerging products, export potential, or tech/process upgrades. |

Will share PART-2 soon.

14 Likes

Great words, just disagreeing to debt/equity part.

1 Like

Thanks. What are your thoughts about D/E?

PART-2/3:

3. VALUATION & ENTRY

| Checklist Item | Rule |

|---|---|

| Valuation discipline | Never buy at hype P/E; target entry below intrinsic value + 25–30% margin of safety. |

| Growth vs. valuation balance | EPS CAGR ≥ 15% while P/E < 25 (for small caps). |

| Avoid turnarounds unless clear catalysts | Only if management or balance sheet has genuinely changed. |

| Position size | 2–5% for conviction ideas; 1% or less for experimental smallcaps. |

| Add only on fundamentals improving | Add post-earnings upgrades, not on price spikes. |

4. RISK MANAGEMENT & GOVERNANCE

| Checklist Item | Rule |

|---|---|

| Liquidity check | Daily traded value ≥ ₹50 lakh (for entry/exit flexibility). |

| Promoter holding trend | Stable or increasing. Avoid falling promoter stakes. |

| Audit quality & transparency | Big-4 or reputed auditors preferred; annual reports must explain strategy clearly. |

| Regulatory / sector risk | No excessive dependence on government orders or commodity cycles. |

| Drawdown plan | Pre-decide exit levels or stop-loss for microcaps (-25% to -30%). |

| Diversification | ≤ 20% of portfolio in microcaps, ≤ 10% in any single company. |

7 Likes