Yes agree with you. This post is quite old and still resonates now…

Q4FY25:

• The Board has approved acquisition of the remaining equity shares of 20 Microns Nano Minerals Limited (20MNML) from its existing shareholders, thereby increasing the Company’s holding from 97.21% to 99.99%, making it a wholly owned subsidiary.

•

• We have built a portfolio of Industrial Micronized and Sub Micronized Minerals backed with our expertise in Micronization. India’s largest producer of micronized industrial minerals

We are now expanding our portfolio into the world of Performance Minerals, Speciality Chemicals and Functional Additives catering to the niche segments and formulations made through advanced and superior technology to serve our existing and new customer base for diverse applications.

• We have achieved the highest-ever revenue in FY25, driven by the addition of new clients, expansion of our product line, and the widening of our distribution channels

• Paints continued to dominate our revenue landscape, holding a 48% market share in 2024-25, followed by polymers at 25%. The entry of new players in the paints industry presented a significant opportunity for us, given our established reputation in the market, and contributed to our growth during the year. However, higher freight costs from raw material imports, which couldn’t be passed on to customers, reduced margins in the paints business and muted overall margins. While dependency on paints will continue over the medium term, our focus is shifting towards the plastics and rubber industries with the development of new products. In the coming years, we expect growth in the plastics and rubber segments, leading to a shift in the overall mix and improved margins.

• Export revenues constituted 13% of our topline in 2024-25 and are expected to remain in the 13-15% range going forward. Markets in Latin America and Southeast Asia—especially Indonesia, Vietnam, and Thailand—are promising, with significant potential in the coming years. Even in exports, our primary focus remains on paints and coatings, plastics, and rubber.

• Outlook: We expect to achieve 15–18% revenue growth in FY26, with stable EBITDA margins, supported by improving demand, economic conditions and easing input costs. Our Malaysian mine acquisition secures long-term & quality raw material supply for manufacturing and we remain open to strategic mining acquisitions to strengthen our cost base and supply chain resilience.”

• The carbonate industry continued to face margin pressures due to rising raw material and freight costs, which is highly import dependent, and have been difficult to pass on to customers amid intense competition.

• Value-Added Niche Solutions: Apart from our conventional industrial sectors, we have started focusing on niche segments such as Adhesives & Sealants, Petrochemicals, Cosmetics and Personal care, and the Tyre industry. The company is transitioning from supplying basic fillers to producing more advanced, value-added materials that can serve as substitutes for high-value imported goods.

o Tyres: At our pilot plant, our delaminated kaolin substitute passed rigorous plant, quality, and system audits by tyre manufacturers and is now moving toward commercialisation.

We’ve also developed a talc-based material that has been approved by a leading global tyre company as an imported-material replacement.

o Cosmetics: We introduced our hygienic calcium carbonate into the personal care sector—winning approval from a leading manufacturer and beginning supply to another major FMCG company.

o Petrochemicals: After a year of commercial success with our CaCO₃ antiblocking agent at a major petrochemical firm, other petrochemical companies have begun pilot‐plant evaluations.

o Adhesives & Sealants: We’ve introduced nano calcium carbonate specifically catering to the Sealant industry which is on the growth track showing immense potential for the future subject to approvals from customers.

• Capex and M&As:

o We plan Rs 100 crore of capex for various projects lined up for the next 15-18 months in phase-wise manner encompassing expansion of our recently acquired Malaysian Operations, more mine acquisitions, regular expansions in Calcium Carbonate and Talc and significant expansion in Kaolin, all funded via internal accruals.

o Malaysian mining operations are set to begin by mid-2025, securing high-purity limestone to boost global output.

o Operational since Q4 2025, our new expansion at Makrana Operations with roller mill grinds ultrafine calcium carbonate, boosting annual capacity by 12,000 tonnes.

• Opened a new Quality Control (QC) Laboratory and Administration office in Udaipur, Rajasthan

•

•

CONCALL NOTES:

• ON COMPETITION: Now when we look at the global scenario, we do have competition coming in from the world’s largest industrial mineral manufacturers who are very big on scale compared to 20 microns and we see them as competitors on a global platform. But when it comes to India, we have a lot of regional competitors and each mineral that we discuss about it will have different competition in the landscape. So, it will not be a similar competitor which will be across different minerals that 20 microns is into.

• VALUE-ADDED PRODUCTS GROWTH RATE: 18 to 20% growth rate is what we usually go with looking at the current market trends even in the value-added segments and the approvals of the products, which take quite longer in the value-added segment compared to the traditional segments that we usually are in. So that’s what we look at in the next 2 to 3 years that you can estimate it to be.

• ON MARGIN EXPANSION ONCE MALASIYAN MINES START: It is too early to say right now because we have not yet started the mining operations. We would start it somewhere in the next 2 months where we would actually get to understand what kind of ore would be useful for us in different parts of the process and the supply chain what we what would be a part of it. So, it will be too early to comment on it as to how much we are going to be adding in terms of the margin space. But yes, we would be gaining more in terms of the dependency that we earlier had on external, you know suppliers. That dependency is now gone and we will be mining as per our own requirements for the production processes that we have across India and abroad. And so based on that, we will be kind of working around selecting the right kind of ore for our own processes and selling the non-required ore to external industries which need that kind of a material. So, I think it will be too early to comment on the margin space right now.

• What is different between Malaysian and Vietnam calcium carbonate?

There is a lot of difference in terms of the purity. There is a lot of difference in terms of the brightness. There is a difference in terms of, you know the end use where only some industries can use a Malaysian calcium carbonate due to the typical properties it carries versus a Vietnamese calcium carbonate versus Indian calcium carbonate versus an Egyptian calcium carbonate. So there are various properties which people look at, the industries look at and we have to solve those industries through that particular ore itself.

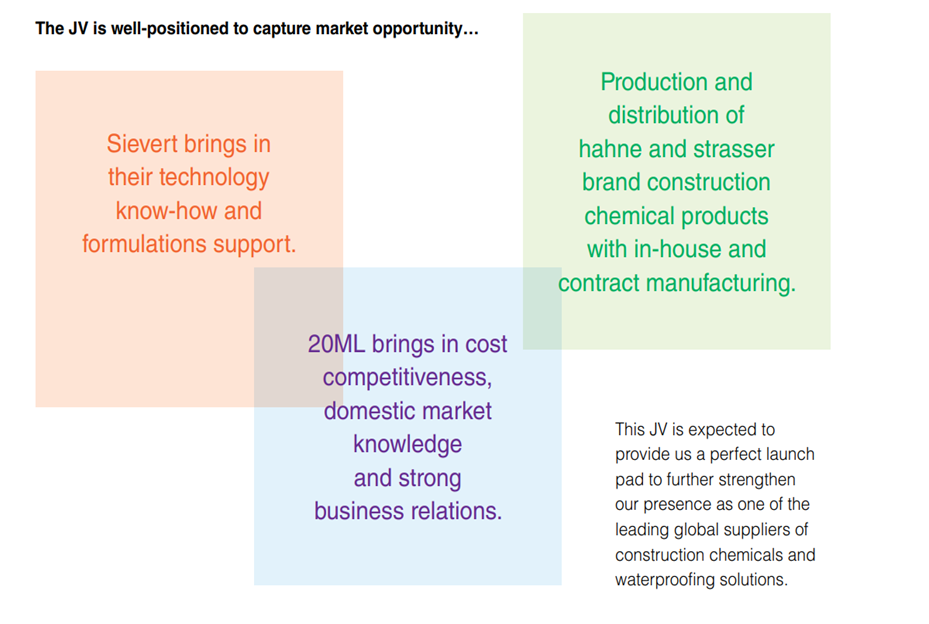

• CONSTRUCTION CHEMICALS JV: Sievert JV, we recently just inaugurated the plant this month and that is regarding the construction chemicals business which we are going to be looking into where we are starting with tile adhesives. It’s just the first phase that we have started with and then we will be going in with liquid construction chemicals in the second phase for the same.

• 20 MICRONS NANO CAPEX: So, we will be investing about 15 to 18 crores of CapEx in 20 microns Nano Minerals Limited where we are putting up a calcination facility for the rubber industry. And we will also be catering to some specialized paint grades for the clay; you know the specialized grades of Kaolins that we will be doing in the Nano with a different kind of a technology that we will be using there

• INVENTORY JUMP: There are many reasons for the same. The supply chain related situation is kind of, you know playing a very important role in the raw materials for 20 microns and 20 microns Nano Minerals Limited. So, we are quite dependent on imported raw materials which account for 36 to 37% of our total raw material usage. And when you are dependent on imports, you have to build up on inventory because there is you know dependency on the freight factor, there is dependency on the availability of the vessels. We have moved towards bulk shipments to retain the freight cost or to lower the freight cost to an extent. So, we need to build up the inventory in India because just in time does not work for these kinds of minerals and due to that and when you look at the jump in the turnover that kind of an inventory buildup was required and so that was one of the reasons that you know you see a you jump in the inventory.

• PLASTIC AND RUBBER SEGMENT FOCUS: So, there are quite a lot of products that we do for the plastics and rubber industry. And we see a lot of opportunity in the coming years for these 2 industries in terms of the value-added minerals. And that is the reason that our focus has been primarily on these right now and developing more products for these 2 industries.

• COMPETITIVE ADVANTAGES: So, when it comes to stickiness of the customers, the customers have different policies when they you know, look at suppliers. So sometimes if we have a whole basket of different products that we offer to our customers, they would like to work with 20 microns and that is one of our competitive advantages. Competitive advantage is the basket of products that we carry all the way from 20 microns to 20 microns nano minerals. We have a variety of products that we offer to the same industry. So that gives them you know a very heavy lineage of working with us.

Secondly, all our customers know 20 microns as a very innovative company, highly focused on research and development. And many of them have already visited us and they know the strength that we carry in terms of the R&D facilities that we have and the product application centres that we have at our Vadodara location and the quality of people that we have recruited to innovate these kinds of products for the industries. So they know that strength very much and they work very closely with us in terms of product development and in terms of any import substitute that they would be probably buying and they want to, replace it with a Indian made product then they definitely feel 20 microns could assist them with and so that is one of the areas where we also hold a lot of strength and competitive advantage and also we are very well located in terms of infrastructure. So, you know we have 9 manufacturing locations, we have 15 warehouses and distribution sites across the country in India and we also have international subsidiaries from where we cater to some of the Indian clients also. So, keeping all these infrastructure related geographies into mind and the workforce that we carry at all these locations which are very close to the customer locations when it comes to service. So, all these play a very, very important role in terms of competitive advantage and where we have an edge over our competition when it comes to, you know, non-carbonate products.

Because in carbonate, definitely we see a lot of, you know, competition from the international and the domestic competitors. But it’s a volume game and it’s a huge, you know, there’s room for everybody. So, whenever we have, you know, the basket to offer calcium carbonate is always a part of it. So, that’s how we are kind of very well placed in the marketplace

• So, I think this year onwards, we will be investing quite a lot in the CapEx to generate better capacities and acquisition of you know more mines. So that is going to add more to the value chain overall in in 20 Microns.

THINGS TO TRACK

• Value added products progress

• Non paint segment growth + recovery in paint segment

**• Progress of new mining operations and its impact on margins: **

• Ebitda margin: How does Ebitda margin shape up going forward?

• 20 Microns Nano growth: Does 25-30% growth continue?

• Export sales: Will they bounce back as freight costs have reduced?

• Demand pickup: Will demand pickup in FY26?

3 Likes

The robustness of the business is increasing

-

Focus on value-added niche products and reduction in dependency on paint segment (already down by 2% percentage in terms of sales mix)

-

Increasing value added products will result in better pricing power and customer stickiness for the company (as products take a long time to get customer approvals)

-

Mining operations will help in backward integration and reduction in dependency on import of raw materials (thus reducing exposure to freight or raw material price volatility)

-

Increasing capacities to improve scale

All these should help the company keep on growing at a healthy rate in the long term.

1 Like

Do we know the approximate worth of the captive mines they have? It should help to value the company right?

In the recent conference call, management said the company’s captive mine reserves are about 170 million tons (17 crore tons). Because the mineral content varies, it is difficult to calculate the exact cost per ton. However, management believes these reserves will be enough to support operations for the next 10 years, assuming steady growth.

3 Likes

Hello Madhav

This is a minor mineral so not really in the focus of big players. Calcium Carbonate is itself quite plentiful in the planet. China will be a big player. The operation itself done by 20 Microns may not involve a lot of value addition depending on use case.

Companys management seems to have skin in the game.

Malolan

1 Like

Annual Report FY25:

• Product innovation: Introduced 43 new products across various end user segments; 18 in core applications and 23 in retail via subsidiaries

• Present in 83 countries. (65+ last year)

• 14 State-of-the-art warehouses strategically located across India (vs 12 in FY24). 4,04,613 sq. ft.- Total warehouse area. 70,000 metric tonnes - Total warehousing capacity.

• 8 mining locations (Same yoy) - Five captive mines with 20ML & three captive mines with 20 Microns Nano Minerals Limited

Mining reserve capacity of 11.3 million Tons

• Workforce - 800+

Retention rate: 86%

Median Remuneration of the employees of the company for the financial year is 5.75 lakhs (vs 5.25 lakhs yoy)

The percentage increase/(decrease) in the median remuneration of employees in the financial year ending March 31, 2025: 9.46% (vs 8% yoy)

The number of permanent employees on the rolls of the Company as on March 31, 2025: 411 (vs 383 yoy)

• We remain focused on delivering across the four pillars of our growth strategy: (i) a unique, low-cost production process; (ii) the manufacture of value-added micronized minerals and speciality chemical products tailored to customers’ needs; (iii) a reduced time to market for new products, benefitting from considerable accumulated technical know-how and strong R&D capabilities; and (iv) market reach leveraged through carefully curated partnerships.

• Malaysian acquisition secures access to high-quality limestone reserves from Malaysia, home to some of the finest calcium carbonate deposits globally, ensuring long-term resource reliability.

• We’ve recently begun exporting Mineral Fertilizer products to Africa, opening up a new and exciting avenue for business.

• A major milestone was receiving the BIS certification for 20MCC in FY25, specifically for the roads and buildings segment. This achievement is a significant step forward, as it positions us to participate more actively and competitively in large-scale road and infrastructure projects.

• Digital transformation: Several standalone software solutions are currently being deployed with the goal of eventually integrating them to enable seamless, real-time data sharing across departments. While our external communication systems are already well-established, internal coordination, especially around logistics, imports/ exports, billing, collections, and container tracking, are still human dependant. Our aim is to bring all these systems online and synchronise them for improved transparency, accuracy, and operational agility. This will be a phased journey: first, digitisation; next, integration; and ultimately, a unified, real-time management solution. It’s worth noting that this transformation is being driven independently of SAP, using purpose specific tools tailored to our needs.

• Renewable energy: On the renewable energy front, while discussions began last year and continue to evolve, we haven’t yet achieved a breakthrough. Due to internal restructuring—particularly in production management—and the volatility experienced last year, plans for renewable integration saw some delays. Initially, we had considered a broader rollout, including in southern locations. However, based on revised assessments, we’ve now prioritised renewable energy initiatives in Rajasthan and Gujarat for the first phase. With a clearer strategy in place, we’re approaching this year with renewed focus and seriousness on scaling our renewable energy efforts.

• Upcoming regulatory changes, such as the mandatory BIS certifications, further reinforce the need for compliance and quality, areas where we continue to lead with confidence.

•

(Rubber segment contribution increased 2% in overall sales mix and plastics segment grew 1% while paints decreased by 3%, in line with management strategy of focusing on plastics and rubber industry through value-added products)

• The Company has in place all the required approvals and has already acquired a limestone quarry and crushing unit covering an area of 23.85 acres and a rock deposit of 11.00 million metric tons. This new plant with a production capacity of 40,000 M.T. will not only increase the present capacity of the Company but will also make 20ML the only Indian Company within its industry space to set up a sourcing unit and plant in Malaysia.

Beyond the immediate increase in production, this move offers crucial advantages. Most importantly, it strengthens our ability to manage supply chain risks by reducing our dependence on a limited set of raw material suppliers. Furthermore, it establishes our presence in a region anticipated to be a significant driver of future growth. We also anticipate that this acquisition will provide 20ML with access to superior quality limestone and enable us to more effectively serve our international clientele directly from Malaysia. This proactive investment ensures that the Company is strategically positioned – with the right capabilities, in the right location, and at the opportune moment – to capitalize on emerging opportunities.

• Sievert JV:

• R&D Centre: 2

R&D and Technology talent pool: 36 (vs 41 yoy, 40 in FY23)

Total R&D spend (in FY25): `1.86 crores (vs 3cr yoy vs 4.2cr in FY23)

• Dealer count: 170+

Key customer associations: 25+

(both same as last year)

• We believe in understanding our customers deeply, which is why we have a dedicated, local sales team with a strong scientific background – not just distributors. This direct approach lets us forge strong relationships and gain crucial insights into our customers’ needs, which is the very foundation of our innovation. We don’t just sell; we actively engage with our customers, even co-creating solutions to accelerate our products time-to-market. This deep connection, together with our innovative spirit, empowers us to anticipate future market demands, such as the demand for sustainable ingredients and solutions for helping our customer with import substitutes matching the international standards.

• During FY25, we hired 70 new people to boost our sales and marketing team.

• Substantial Increase in remuneration of both MDs –

Rajesh. Parikh – Ceiling increased to 5cr, up from 2.85cr last year

Atil. Parikh – Ceiling increased to 4cr, up from 2.33cr last year

(Net profit FY25 – 60cr)

•

• The Statutory Auditors’ report on the financial statements for FY 2024-25 does not contain any qualifications, reservations or adverse remarks or disclaimer.

• Secretarial Audit Report contains no qualifications, observations, adverse remark or disclaimer in the said Report.

• Fixed Deposits: The Company accepts unsecured fixed deposits exclusively from its shareholders. As on March 31, 2025, the total outstanding fixed deposits from shareholders stood at 2,304.16 lacs, of which deposits amounting to 1,239.67 lacs are due for repayment on or before March 31, 2026.

During the year: • Deposits amounting to 1,429.12 lacs were renewed.

•

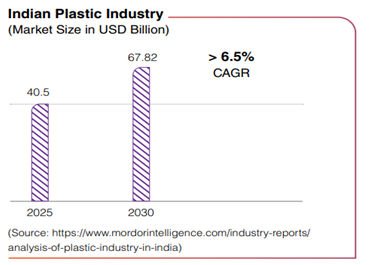

• Growing usage of minerals in the plastics & polymer industry: Over time, the Indian plastics industry has seen a steady rise in the use of minerals, recognizing their vital role in enhancing the performance and versatility of plastics and polymers. Mineral based additives like calcium carbonate, talc, silica, and clay have become essential, serving as fillers, reinforcements, and functional agents that significantly improve the strength, durability, and other key properties of plastic products. Calcium carbonate, talc, and silica, for example, are widely used to increase rigidity, reduce shrinkage, and enhance the overall cost-efficiency of the final products. Meanwhile, clay minerals act as both fillers and reinforcements, elevating the performance of plastics and broadening their range of applications.

Beyond strengthening physical properties, certain minerals also boost the electrical conductivity of plastics, paving the way for their use in high-performance and specialized industries. Mineral additives further enhance heat resistance, making plastics more reliable in high-temperature environments. Importantly, they contribute to sustainability efforts by enabling the incorporation of more recycled or bio-based materials into plastic formulations. Some minerals even support the recycling process itself, helping to separate different types of plastics and improving the quality of recycled outputs — a meaningful step toward promoting circularity within the industry.

•

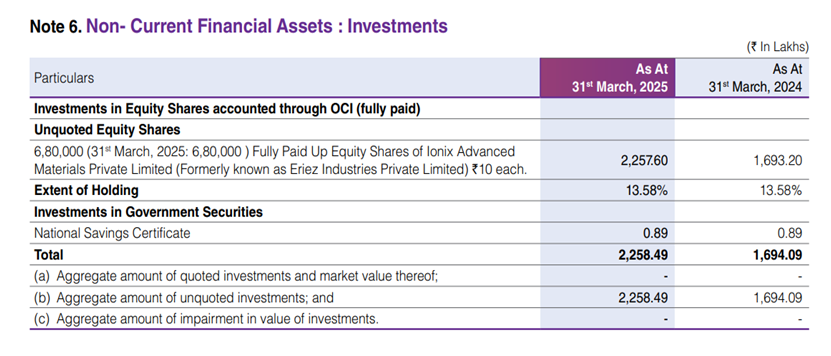

(Ionix is 25% shareholder in 20 microns)

•

•

•

• Hundi Discounting Charges: 526.23cr vs 573.60 yoy

•

•

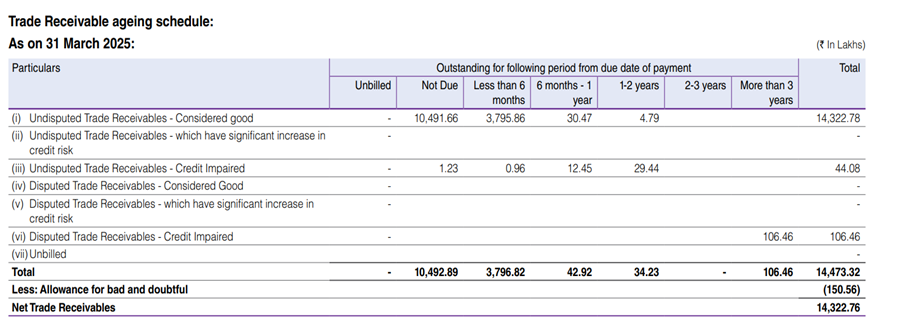

• CUSTOMER CONCENTRATION: There are two (P.Y - two) customers to the company which accounts for more than 10% of aggregate sales. Net sales made to this customer amounts to Rs. 20,181.34 lakhs (P.Y 16,803.85 Lakhs)

10 Likes

Q2FY26:

• Extended monsoons and the late onset of the festive season slowed demand for paints during the quarter, while intense competition weighed on the profitability of paint manufacturers. However, despite these headwinds, we strengthened our position, gaining market share and maintaining margin stability.

• The paints segment remained the largest revenue contributor (48%), followed by Plastics and Rubber at 25% and 9% respectively.

Our continued emphasis is on innovation and product diversification, especially in plastics and rubber segments. We expect them to drive future growth, resulting in a favourable shift in the overall revenue mix and improved margins in the coming years. While new product introductions and deeper market penetration drive Plastics business, Rubber segment will be supported by rising demand in industrial applications and improved distribution reach.

• We are confident of a demand recovery in the second half of FY26, driven by the festive and wedding season.

CONCALL NOTES:

• OPERATING EFFICIENCY: The margin improvement is a direct outcome of continued cost initiatives, operating discipline and more efficient sourcing.

Even in a revenue constricted environment, operating expenses were tightly controlled, declining 7.7% qoq and 5% year on year. This demonstrates how our efforts on cost efficiencies, alternative sourcing and manufacturing discipline are translating into measurable financial gains.

• The paint industry had gone through a temporary slowdown driven by external rains, subdued customer movement and competitive pricing actions. But within this environment, 20 Microns strengthened its market share, especially as paint manufacturers increasingly prefer reliable suppliers and diversified offerings and consistent service level. We remain a strong alternative to the traditional suppliers and our diversified customer mix help cushion the downturn.

• While paint remains the largest segment, our strategic direction is clear - Growth through innovation, new product introduction and deeper penetration in the plastic and rubber segment where our margins are structurally higher. This shift will keep will help us further rebalance our portfolio in coming years.

• DEMAND TO IMPROVE IN H2: Looking ahead, we expect a more constructive environment in the second-half of FY 26. Festive and wedding season typically drive consumption cycles and early indicators of October and early November suggest improving activity level. International enquiries have also picked up from the recent industry exhibition we entered. While we stay conscious on micro uncertainties, we do believe that the world worst of the demand softness is behind us.

Our deep integration with leading paint manufacturers positions us to capitalise swiftly on a cyclical uptick.

Looking ahead, we anticipate a recovery in the demand, though slowly, particularly in the paint and construction segments fuelled by festive and wedding season consumption and the infrastructure upgradation activities.

• With stabilizing raw material prices, improved utilization level and continuous focus on operational efficiencies, we are confident of maintaining margin improvements in the coming quarters.

• The polymers and rubber division showed growth in the industrial application, though at a measured pace due to the global raw material volatility.

• Product innovation and value-added formulations are helping us capture higher value market segments, which is evident in our Q2 performance.

• Based on our offerings, our B2C portfolio in the construction chemicals and mineral fertilizer space is also gaining traction, particularly in the underserved Tier 2 and Tier 3 markets. The distribution network continues to expand, offering potential for incremental growth from a smaller base.

• Our recent expansions into Poland, Latin Middle East and South Africa are beginning to yield results offsetting some plateauing in saturated Western European markets. Our deals strategy is helping us win new clients seeking alternatives to traditional supply chains and export revenue is expected to climb in the coming quarters.

• Our focus in the next half would be on accelerating growth in value added segments and speciality chemicals to enhance our margins and reduce the cyclicality.

• CAPEX: Our planned CapEx fuelling growth in capacities has been slightly deferred but will smoothly be executed from Q4 onwards.

The CapEx currently has been slightly deferred because of the current lowering of the demand. We are revising our CapEx plans and we will in the in the coming months come out with hopefully a press release with the new CapEx plan that we will be having based upon the 100 crore plan that we have announced.

Our Malaysian CapEx plan is on track. So, we have already finalized plans of infusing funds into our Malaysian subsidiary for the expansion of our calcium carbonate operations.

• Well, usually the second quarter is at its peak, but this time due to the lower demand which has been there, we are expecting that the third & fourth quarter should be decent compared to the last half.

• GUIDANCE: We are hopeful that with the encouraging demand coming up in the next few months, we should hopefully achieve the targeted growth rate of 13%. Margins should be in the range of 13-15%.

So, I think currently we are at 13.7% where we moved from 12.7%. But when the demand goes up, the margins might get compromised a little bit. I think 13 – 13.5% is something that we expect to close at the end of this financial year.

Steady state EBITDA margins will always remain in the 13 to 15% range depending on how the

product mix and the demand is.

• MALAYSIAN MINES: The Malaysian mines have recently been operational and to go full-fledged it will take another few more months till we reach the optimal level where we will then be able to get a proper guidance about how much savings that we can do in terms of the margins.

Because currently we are working on all different grades that is coming out of the mines. And once we segregate those grades in the near term for our own production, based on that, we will be able to have a fair picture about the cost inclinations and the improvement in the margins that we can see in the forthcoming quarters.

We will be able to get a better idea about it only at the beginning of the next financial year.

• NEW PRODUCTS: We have introduced a whole range of different products in the last quarters of the last financial year. And in this first half we have been trying to promote those products, from organic thickeners to pacifiers to flame retardants and activators to partial replacement of zinc oxide. So, these products have been slowly accepted by the markets in the domestic front as well as in the international markets**. And we are very hopeful that in the upcoming quarters also we will see a significant growth in these products.** And we are seeing quite encouraging results currently.

And hopefully there are a few more products also in the pipeline, which is too early to comment on right now, but they will be introduced in the fourth quarter when we will be showcasing those products in our upcoming exhibitions for plastics, rubber and paints in February, March and April of 2026. So that is the time when we will be launching those products as well.

• RARE EARTH MINERALS: There’s not much clarity from the government about the rare earth minerals that are available in India and the processes and the availability of these rare earth minerals in different parts of the country. So, we are working closely and trying to explore to see if there is any potential that we can establish in terms of rare earth minerals in the future. But it’s too early to comment right now because it’s just a very new area to be looking into.

So, it’s very different from what many microns currently does. But yes, if the opportunity arises and if we have good initiatives and information available from the government, then definitely we would be looking more into it in the future.

• 20 MICRONS NANO: In H1 we have not seen a significant growth. We are at the same levels that we were in the H1 of last year. But yes, we have significantly decreased our raw material cost in Nano in in this financial year and also that has led to increased PAT margins and PAT of 20 microns nano. So that has been a good sign which we were anticipating for quite a long time.

In terms of the overall revenue growth, as the demand is currently sluggish, we are hopeful that the demand will improve in both the exports and the paint segments in the upcoming quarters. But in polymers and in rubber segments, we are on track and we have seen a good growth in these two areas in in the first half of this financial year.

• INDIAN MINES: Our Bhuj mine is completely operational. But apart from that, all the other mines that we have, we have already started to do core drilling to establish the quality of the materials which is available in the mines at a certain depth.

So, once we get more data on the core drilling operations, we will be able to establish a plan about the mining in the coming quarters. And we will be doing it 1 by 1, opening the mines one after the other and not all at once because we will have to look at the cost structure also, which is a significant part of the mining. And so, we will have a better idea once we get more data on the drilling operations which are under process right now.

• JVs: We have seen a very good increase in the revenues in our Dorfner JV for coloured quartz. We have almost doubled our turnover in the first half when we compare it to last year.

And we have recently started the production of our adhesives with Sievert 20 microns Private Limited. And there we have just introduced the product into the markets. Recently we participated in one of our recent exhibitions which was quite successful in Mumbai for construction chemicals where there was a lot of traction for the new brand and the new products that we’re launching in the market.

So slowly and steadily we see a lot of growth that we are expecting in this particular company as well. But it’s too early right now since we have just started production. So maybe in the next quarter we might have some, you know, figures to share.

• Well, the competition is increasing in the paint industry and they are working on reduction of the raw material cost due to stiff competition between the paint manufacturers. And due to that they are trying to, you know, squeeze our margins for the raw materials. And so, we work on a very selective approach when it comes to paint industries in terms of our product offerings to sustain our EBITDA margins currently. But in the future, if the competition gets eased out a little bit and there’s room for growth in terms of the product portfolios, then definitely that will allow us to improve our margins.

THINGS TO TRACK

• Value added products progress

• Non paint segment growth + recovery in paint segment

• Progress of new mining operations and its impact on margins:

• EBITDA margin: Will efficiency gains and improved EBITDA margins continue?

• 20 Microns Nano growth: Does 25-30% growth continue?

• Export sales: Will they bounce back as freight costs have reduced?

• Demand pickup: Will demand pickup in H2?

3 Likes

20 microns has undergone a big consolidation phase over the last 1 and a half years, driven first by margin pressure and then by demand slowdown in paints segment.

Margins have already recovered and now, with expectations of good growth in paint segments, Paint segment should improve as well.

In this period, they have done all the good things. Improved operating efficiencies, increased market share, introduction new products, entering new export markets & Malasiyan mines for backward integration and supply chain control.

These should now begin to yield greater fruits once demand from paint segment accelerates.

Things should start improving in q3 itself, 15-20% yoy growth expected, given q3 of last year had the worst of margin pressures.

DISCLOSURE: INVESTED (Biggest position in portfolio in terms of cost)

2 Likes

1 Like

The management in earnings call had mentioned that higher competition in paint industry could mean lower margins as everyone will try to squeeze the vendors.

So, while demand will be high, margin pressures might continue I think. Tricky one to foresee.

1 Like

Fierce competition along with slowdown in demand has been witnessed in paint industry for the last one year, yet 20 microns margins have improved!

So, I think even though paint manufacturers will try to squeeze supplier margins, 20 microns operating efficiency will ensure stable margins going forward. Plus back ward intergration benefit will also come of Malaysian mines.

1 Like

The ‘boring’ mineral company quietly transformation into a specialty play

20 Microns is quietly transforming from a cycle-exposed industrial mineral supplier into a more resilient, value-added business with steadier margins and returns.

Today, a combination of deeper integration, a changing product mix, margin discipline and steady capital allocation is slowly reshaping what was once seen as a plain commodity-facing business.

For most of its listed life, the company has been viewed as a steady supplier of micronized minerals, tied closely to cycles in paints, plastics, ceramics and construction. Useful, dependable, but rarely seen as a business with structural upside.

That view no longer tells the full story.

This isn’t a pivot; it’s an evolution. There is no sector shift or headline-grabbing acquisition. Instead, the company is layering multiple small but meaningful changes that together are altering the quality of earnings.

An industrial minerals business with uncommon integration

Most industrial mineral players in India operate as processors rather than owners of resources. They buy raw material, add processing value and compete largely on price and service.

20 Microns has chosen a different path.

The company has access to captive mineral resources across multiple locations, giving it greater control over quality, consistency and cost. Mining reserves run into millions of tonnes, spread across key mineral belts.

This matters because integration is not about growth during good times. It is about margin protection during bad ones.

When logistics costs rise or raw material quality fluctuates, companies without integration feel the pressure immediately. Integrated players absorb shocks more smoothly.

This advantage rarely shows up in a single quarter. It reveals itself across cycles.

The portfolio is quietly shifting upward

Industrial minerals are often viewed as low differentiation products. That assumption breaks once the portfolio evolves.

20 Microns has been pushing steadily toward functional additives and speciality applications. These are materials designed for specific performance outcomes rather than generic filler use.

Functional additives need application expertise, research and development support and long customer relationships. Once approved, switching suppliers is uncommon.

During the year, the company introduced more than 40 new products across paints, plastics, construction chemicals, rubber and speciality applications. A rising share of revenue now comes from products that sit higher on the value chain.

This shift improves margins and reduces volatility at the same time.

Margins that hold when volumes soften

The first half of the financial year 2026 offered a useful stress test.

Paint demand softened due to extended monsoons, delayed festive activity and pricing pressure across the industry. Revenue growth slowed and turned negative on a year-on-year basis in some quarters.

Yet EBITDA margins expanded.

In the September 2025 quarter, margins moved close to 14%, supported by cost discipline, sourcing efficiency and a better product mix.

That signal matters.

Commodity businesses usually see margins compress when volumes slow. Margin expansion in a weak demand environment suggests that structural changes are working.

Defending margins is often more important than chasing volume growth.

A strong balance sheet built for downcycles

One of the least discussed strengths of the company is financial discipline.

There has been no attempt to force growth through debt.

In industrial businesses, clean balance sheets are not optional. They are insurance.

They allow companies to invest when others are forced to pull back.

Working capital remains an execution test

Working capital discipline remains an area to watch as the company moves further up the value chain and expands its global footprint.

Inventory management and receivables control will matter more as product complexity rises. Management has acknowledged this and is working on supply chain optimization and vendor rationalization.

The intent is clear. Execution will determine outcomes.

There are no visible governance red flags such as heavy pledging or aggressive related party transactions.

Valuation still anchored to the old narrative

Despite these changes, the market continues to value 20 Microns like a traditional industrial mineral supplier.

Valuation multiples reflect a business exposed to cycles rather than one gradually insulating itself from them.

That disconnect often persists until margins prove resilient across multiple demand phases. It also persists until return metrics begin to look less volatile.

In 20 Microns’ case, return on equity has settled into the mid-teens, driven by operating efficiency and improving working capital turns rather than leverage.

Re-ratings in industrial stocks rarely come from announcements. They come when investors realise earnings and returns are no longer as fragile as assumed.

The risks investors must still respect

This is not a risk-free story.

Demand from paints, construction and plastics remains cyclical.

Mining operations face regulatory and environmental constraints.

Export markets carry currency and geopolitical risk.

None of these can be dismissed.

But risk must be weighed against preparedness. And 20 Microns appears better prepared than it was a decade ago.

Why this feels like a different kind of industrial story

What makes 20 Microns interesting today is not growth alone. It is the quality of growth.

Integration improves cost control.

Product mix supports margins.

Digital systems improve visibility.

Capital allocation remains disciplined.

The balance sheet reduces downside risk.

This is how industrial companies transition from price takers to solution providers.

Not suddenly.

But steadily.

20 Microns is not a momentum trade. It is a structural shift unfolding inside a company that has spent years doing unglamorous work.

Investors chasing headlines may overlook it.

Those watching margins, balance sheet strength and product evolution may not.

And in industrial investing, those are usually the stories that endure.

9 Likes

Ebitda margin improved from 12.8% to 13.6% yoy.

Finance costs reduced to 4.07cr vs 5.25 cr yoy.

Very decent. Margin improvements continue. Now once paints pick up steam, we can see good growth going ahead. Own mines benefits will also kick in from next Fy.

Some costs related to mines may have occurred this qtr as consolidated numbers have dropped lower than standalone qoq.

1 Like

20 microns has around 80% sales in commodity products with high competition and 20% in value added products.

The current margin expansion inspite of muted sales growth (majorly in commodity segment catering to paints), shows that value added, new products are taking hold.

Focus is on value added segment going forward with rubber and plastic segments

It’s a slow transition but one that’ll pay big dividends in the future.

And Malasiyan mines will help in backward integration and improving cost position in commodity segment (the one thing that can give competitive advantage in commodity segment is cost advantage). And reduce any volatility in margins going forward. While increasing export sales (international markets to be catered from Malasiya).

Things look good going forward, especially with paints bounceback and mines getting sizable operations (mines already operational) and value added products taking shape.

The thesis is completely intact (infact improving).

4 Likes

Why the company is giving 50crs loan to company in which director is interested?

Hi,

Loan is clearly not in minority shareholders interest. I had sent a mail. Naturally there is no reply. Clearly there is debt which can be repaid. There is no significant FII or DII on board to question this. Postal Ballot with Promoters owning 45% will go through. No concalls this quarter meaning, it will likely be passed before you get to ask Question. Corporate Interest rates are low at the momment. Realign thesis that management may not be minority holder friendly or may improve over a period of time if planning to invest or if continuing to hold and accept the truth and move forward

Disclosure : Holding for the last 4 years

1 Like

This raises corporate governance issues which derails the momentum of the company

20 Microns Limited has announced a strategic capital expenditure (CAPEX) plan of ₹100 crore to be deployed over the next 24 months. This initiative is designed to expand production capacities, upgrade operations, and accelerate growth in high-margin segments.

The planned Capex is expected to deliver:

-

Projected 18% CAGR over the next 3 years

-

Margins anticipated to rise by 200–250 bps

-

ROCE expected to strengthen to 18–20%

-

Strengthening share in Performance Minerals & Functional Additives segment, targeting 20%+ market share in high-value products by FY 2030

The expansion will be funded through a balanced mix of internal accruals and selective debt.

Source: https://www.bseindia.com/xml-data/corpfiling/AttachLive/b054a101-c1ea-4acb-96ba-1501c4bffb83.pdf

3 Likes