How do you see H1 results? Can’t find on NSEEMERGE site and it seems company website is down.

Hi Yogesh Sir,

Can you please provide suggestion on HEG and Philips Carbon to buy at current price for long term.

Thanks

Vijay

nothing to worry .site being upgraded.

1 Like

CMM infra has reported good growth over the last few years and order book is also good. For the kind of construction activity it does, the opportunity size is also large. However, its ebitda margin at 5% is lower than industry average of 10-12% and for these kind of activities I would expect EBITDA margin to be in the range of 14-15%. Margins may improve with scale but I won’t expect the margins to touch double digits.

I also noticed that company has poor cashflow and it has to borrow money to even pay operating expenses. This has limited its ability to invest in machinery which may be why margins are low. ROA and ROE is also low.

Low profitability may be because there are many unproductive assets on the balance sheet in the form of short and long term loans and advances. While short term advances are deposits with various government departments (which is common in a construction company), there are no details available about the long term loans and advances and there is a steady rise these loans and advances over the years. Together these advances are almost equal to its net worth.

Even in H1 results, there is sharp increase in loans and advances. Considering that assets are created out of reinvested profits, any uncertainty about assets on the balance sheets automatically creates uncertainty about reported profits. I would stay away until margins improve and more details are available about loans and advances in the annual report.

3 Likes

RKEC’s NSE filing are available here

https://www.nseindia.com/sme/marketinfo/corporates/announcements/announcementsList.jsp?symbol=RKEC

NSE Emerge site is available here

1 Like

On this forum we do not ask or provide stock recommendations as buy/sell decisions are up to each individual investor. We can only exchange ideas.

Two companies you mentioned are cyclicals and estimating demand, supply and timing is important in investing these kind of companies. I do not invest in cyclicals so cannot help you with these ones.

2 Likes

Really curious about this philosophy of yours. Stocks rarely stay undervalued. Doesn’t this cause too much churn and so, transaction costs, not to mention Opportunity cost?

I remember Philip Fisher writing something about this:

Read the last line, more importantly. I’d love to hear your thoughts on this.

3 Likes

Well said, Dinesh. Fisher’s argument of holding on to your great stock forever (if it is likely to continue growing) is easier said than done. Getting valuation argument in the middle to sell out (thinking it has got overpriced for its growth potential) will hurt one badly. But those who can practice it will reap the benefits.

I have been holding Page Industries for about 8 years now. Got frustrated about a year back when it had hardly moved for a long time. I sold some around Rs 14,000 out of pure frustration and thinking it had become overpriced for its growth potential. And lo and behold, it went up to Rs 24,000 in the next few months.

Lesson for me: Just hold on to your blue chips. As long as growth is assured and it a well run company with ethical management, just HOLD ON. You may not buy more but hold on to your investment.

Gruh is another stock I have been holding for around 7-8 years. This one I have not sold and am quite satisfied by the results. Growth is assured, management is ethical, sector tailwind is there and it is a well managed business. One can keep arguing that it is overpriced and a sell. Fisher’s above note quoted by you should be a guide to just HOLD ON TO YOUR BLUE CHIPS. Let the market keep debating about valuations.

The last line of Fisher’s article clearly needs to be read again and again before selling your blue chips.

“If the job has been correctly done when a stock is purchased, the time to sell it is — almost never.”

9 Likes

I think this debate about holding a stock forever or for the very long term has to be seen in context of the investment style one practices and kind of returns one expects.

Yogesh practices his own style where he re balances his portfolio every year based on certain fixed parameters. In this kind of style there will be no place for holding a stock for ever because at some point of time the parameters he has fixed will trigger a sell.

And once he has fixed up a system which he has back tested and which has worked for him over the years I think it would be unwise to change the strategy just for the sake of hoping for a multibagger.

And most large caps are very well researched stocks where most of the things are known to most of the people. Its how one interprets this data is important and which provides one the edge.

For other styles of investing this holding on for long time will definitely work but these theories have to be followed in context of one’s investing style.

20 Likes

Buy and hold forever is not for me simply because I don’t have the skill to find businesses that will produce good results for a number of years let alone forever. There are a number of businesses that I bought in the past that eventually lost more than 90% of their value. Fortunately I got out of these businesses much before that. With due respect to Mr Fisher, If I had followed his advice I would haven been bankrupt now.

How do we know if the job is correctly done? We can only know that in hindsight. What if after 10 years we realized that the job was not done correctly? And after realizing that if you change the way you do the job, do you wait another 10 years to see if you got it right this time? I think a more practical way is try out different strategies and make small improvements regularly. Over a period of time you will know what works for you.

It takes a great deal of skill to find businesses that will do well in the long term i.e. to do the job correctly. Unless you are extra-ordinarily talented, most investors reach that level of skill only after being beaten up by Mr. Market for several years, even decades. By the time an investor reaches this skill level (if at all), his investing career is almost over unless he is extra-ordinarily talented and started investing as a teenager. I certainly don’t fit in either of those categories.

Ideally, I would like to own businesses that produce a steady growth in earnings and stock price also goes up steadily and remains fairly valued. I will own that business for as long this situation continues. In fact, I did manage to buy few such businesses but I can only say that with the benefit of hindsight. Reality is that all good things come to and end and sometimes unexpectedly. In the long run we are all dead including good businesses.

Holding on to a business forever means we assume that there will be no good businesses in future. In fact half of my actual portfolio now consists companies that went public in last 2 years. Owner of a business does not have the option of switching from one business to another easily. As minority investors, we have the option of hitching our wagon to growth engine of a business and get off before it slows down and hitch it to another one that is picking up speed. Why not use that option?

I think you have answered your question. If stocks rarely stay undervalued, why hold them forever? An overvalued stock may be a good business but not a good investment. In fact there is an opportunity cost of holding on to overvalued businesses because you will not be able to invest in other businesses that are undervalued.

About churn and transaction costs, it depends on how often you review your portfolio and make a serious buy/hold/sell decision. For my low maintenance portfolio it is annual so there is not much churn. For my actual portfolio it is quarterly and sometimes more often based on how Mr. Market is behaving. Eventually, I will be moving on to my low maintenance portfolio so churn will go down in future.

My valuation model takes into account changes in risk premium so in a rising market risk premium drops and fair value rises although not by the same amount. Similarly, I consider (CAPM) alpha returns while deciding if a stock has produced abnormal returns and has become overvalued. Additionally, I have a tolerance band around the fair value so some overvaluation is tolerated especially if company is exhibiting earnings momentum. In the end I ask myself a simple question, if a stock drop 20% for ANY reason, am I willing and able to buy more? If the answer is no then I sell it.

29 Likes

I have made the same mistake in the past and likely to make the same mistake in the future if I keep holding on to overvalued stocks. This is precisely the reason I don’t hold on to overvalued stocks. Even good businesses will go sideways or down for a while and investor begin to question their conviction, some bad news will hit the stock and that will act as the last straw that will cause the investor to bail out at the worst moment. Now calculate your CAGR from the last time you decided to hold it until you bail out this way and add to that the opportunity cost of not buying some other stock that would have gone up during this time. I am sure, it ain’t worth holding on to overvalued stocks. Moreover, for every Page like stock that jumped right back up, there will be 10 that won’t. I am not even counting this probability in my calculations.

I know there are lots of if and buts and estimates in this whole logic but devil is in the details and precise math. Additionally what’s also important is the loss of confidence when I bail out this way. I can’t put a price tag on that. It will prevent me from making big bets on my high conviction ideas. IMO, making big bets means one has to have a high success rates in one’s decision making process and mistakes and loss of confidence will prevent one from reaching that level.

Most of the stocks like Page and Gruh have produced wonderful record of earnings but at least half of their returns are because of expansion in their price multiples which have reached a level where further expansion seems unlikely. Although I felt the same way three years ago and their multiples have expanded since then.

My experience is that for every overvalued stock that I have sold only to see it hit new highs, there are 3 that produced mediocre returns in future and some even turned out to be disasters. My preference of avoiding such outcomes far overshadows regret of selling a great business early. Moreover, if a business is worth holding forever, one can always get back in anytime, right? How many actually do that? Many investors are anchored to their historical buy price and that prevent them selling and buying it back as it will reset the price anchor to a higher level. For me the buy price is always the market price when I last reviewed my portfolio and decided to hold.

I also believe that all great businesses will turn into average businesses sooner or later and market will value then as average businesses when that happens. To me, it’s a question of when and not if. Many will disagree with this assumption though. There are businesses that have remained great businesses for decades but these are exceptions and we can only say this with the benefit of hindsight. I certainly won’t be able to tell which businesses that are great today will remain so in future. In my valuation model, if you project future cashflows with this assumption and discount it at your opportunity cost, all such businesses will appear highly overvalued. Its only when you assume that a business will remain great forever, you can justify current price and that too when using a lower discount rate. Since expected return on a fairly valued stock is the discount rate used in valuation, expected return on such stocks is far lower than what I have actually earned and expected to earn (i.e. my opportunity cost) on other fairly valued businesses.

Holding on to overvalued stocks is essentially betting on a greater fool who will pay an even higher multiple in future. Such logic doesn’t appeal to me and I certainly won’t make big bets on it. I also believe that if you look hard enough, you will find good and undervalued businesses in any market. If there is a good business available at reasonable valuation, why hold on to an overvalued one?

23 Likes

Something I read in Thinking fast, and slow about buying extended warranties comes to mind. Some will spend anywhere from 5-15% of the cost of product for an extended warranty on a product whose rate of failure might be much lower than 5% in the extended-warranty period. It gives a peace of mind to the individual buyer in terms of individual decisions pertaining to the specific product, but for all the products you ever purchase in a lifetime, you might be better off adopting to not buying extended warranty as a “policy” and stick to it.

Similarly, a decision like holding onto overvalued quality stocks should be seen from a portfolio perspective or rather, from a portfolio of an individual, run by the same individual’s perspective. This special case can allow for certain policies to be adhered to without external influence (all the portfolio money is yours, all the buying and selling decisions are yours and yours only), similar to not buying extended warranties example.

When done as a policy, not holding onto overvalued stocks means the individual perceives better opportunities and even if a specific overvalued stock runs up, in the long run, the strategy will yield better results. This is a classic case of verifying if inference from the general applies to the specific and also to not be affected by narrow-framing (specific stock running up) but see things with broad-framing (portfolio performance over time).

The caveat of course is the individual’s stock picking skills and the capacity for idea generation, the quality of such ideas which depends on time, effort, knowledge and intellect. The bigger caveat of course is that most of us think that the general doesn’t apply the specific that is us. So the best way to go about it is to try it out for oneself and if in a broad framing context, the individual decisions don’t affect negatively, then stick to that strategy (until it works that is).

12 Likes

Thanks for sharing the ideas Yogesh. It is definitely helpful for novice investors like me. Would love to hear your thoughts on the below observations -

-

Valiant - Promoter has diluted equity and holding has reduced from 52% to 47% in last 1 Yr. Receiavles/Sales vary in 20-30% range.

-

NGL Fine chemicals - (Inventories+Receivables)/Sales =45%. Isn’t that too high? Why is the company not clearing inventories along with setting up new capacity?

-

NOCIL - 13% of promoters shares are pledged.(Inventories+Receivables)/Sales =40%. Isn’t that too high?

Would you consider Castrol, HUL, Asian Paints and a few more similar who may have given good returns could be currently highly priced and therefore capital could be stagnating?

Valiant - Due to recent merger of group company Abhilasha, promoter holding has changed. It will change again once another group company Amarjyot is merged with Valiant. This is not an issue. Regarding receivables, receivables are somewhat higher than desired but it has not resulted in debt pile up. Company hs debt free so receivables are not an issue.

NGL FineChem - Agree. NGL does not have best of the balance sheets but they have mentioned that they offer generous credit to buyers hence receivables are high. They also have high margins so these credit terms are recouped as margins. FY18 there is some improvement in receivables.

NOCIL - Share pledging isn’t an issue here. Company is almost debt free and paid down debt taken for previous expansion. 40% is OK for this type of business. What I generally see if all internal accruals are getting tied up in working capital and that is causing company to borrow money for capex. That’s not the case with NOCIL. Also margins are rising so company is not pushing sales with generous credit terms.

5 Likes

Your questions is not relevant to my comments that you have quoted but I will try to answer it anyway.

HUL and Asian Paints appear to be overvalued but market is pricing several years profits in the price. This is because of visibility of their sales well into the future. With their dominant position in a large and growing economy with low penetration of their products, investors are assured of steady profit growth for several years. Such stocks trade like bonds as their profits are as steady and assured as coupons on a bond. Such stocks are priced such that expected returns works out to be 8-10%, just above interest rates on long term bonds and their prices reflect changes in global interest rates.

Castrol is not as overvalued as others but much of the same arguments will apply to Castrol as well. All these companies have little substitutes so investors have priced in several years of growth in the price.

6 Likes

Thanks Yogesh. Understand what you are saying.

Increasing oil prices benefit Castrol profitability ?

Hi Yogesh - I have been learning the ropes of Investing, can you elaborate this point a bit more on how do we calculate whether the internal accruals are not getting tied up with WC, sorry for asking too much.

Thanks,

Pandi

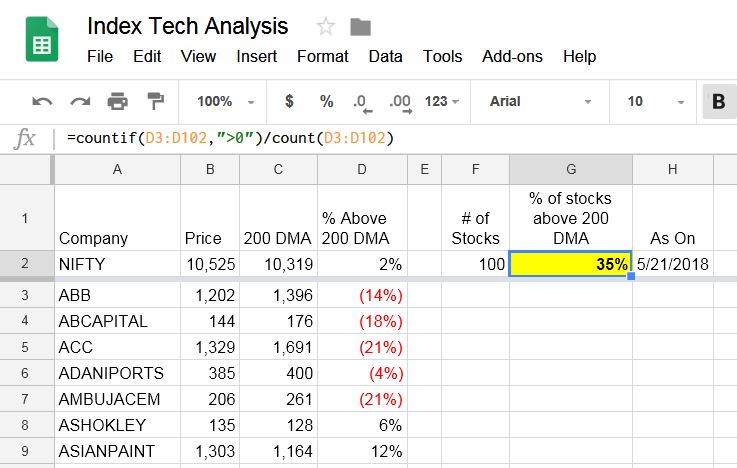

Although I don’t use technical analysis for picking stocks, I have been using a technical indicator to help me decide how much cash I should hold in my portfolio. This indicator is the % of stocks that are trading above 200 day moving average.

To calculate this indicator, I take 100 stocks from Nifty 100 index (nifty 50 + Nifty Next 50). For each stock, I calculate 200 day moving average (DMA) and compare it with current market price. The indicator is simply the number of stocks trading above their 200 DMA.

As markets rise, more and more investors turn optimistic and they push more and more stocks above 200 DMA. At the top of the bull market, this number is around 80. As market begins to correct, more and more investors turn bearish, they push more and more stocks below their 200 DMA. At the bottom of bear market, this number is usually around 20. This indicator is at 35% now and trending down.

I created a shareable version for VP.

Link to Google Speadsheet is below.

Note: Be patient. This sheet takes few minutes to open.

There are 3 sheets for Nifty 100, Nifty Midcap 100 and Nifty Smallcap 100. Nifty 100 sheet can be used for back-testing by changing the As On date.

This sheet uses GOOGLEFINANCE formula which has its own limitations like missing data and unadjusted prices. To that extent, results will be inaccurate but overall, results are fairly good.

As the indicator moves lower towards 20, I generally begin to deploy cash and as it moves beyond 70 or 75, I generally start selling if I have any overvalued stocks in my portfolio. This is a slow moving indicator, and it generally coincides with the bull-bear markets. As with any technical indicator, this is not accurate all the time. In some cases, indicator will top out or bottom out few days before the market does (which is good as it gives you some time to act) and other times it tops out or bottoms out much before the market (which is not optimum as this can be too early). But in either case, it is a good leading indicator and will act as a early warning.

Your views are invited especially how do you decide your asset allocation (if at all you manage that actively).

90 Likes

Do you use this indicator for any specific stock as well ? if so then how?