If one has to go by technical chart and price volume action then it seems more downside can be expected in this stock. There is more sellers than buyers at every fall and today closing also happen at close to day low of RS 161.

Disc : was thinking for taking some position but no investment till date and seeing technical chart decided against it

2 Likes

What has gone wrong with Yes Bank

- Yes Bank was run like a tight ship by Rana Kapoor and with his departure investors are worried about growth.

- Regulator removing a bank CEO sounds like a bad headline and many money managers must have exited the stock as they cannot justify holding on to their clients.

- Financial companies generate ROE of 15-20% but can grow their per share book value at 25-35% by raising fresh equity at a huge premium to book value. Some investors (me included) would have invested in Yes Bank as it was planning to raise capital in 2018-19. With these troubles, fresh capital raising looks far away and at 1.5 times book value, will not boost the per share book value as much as it would have when shares were selling at 3.5 times book value. Such investors would have left (me excluded) and will not come back until shares trade at a high premium to book value and there are fresh capital raising plan.

- Yes Bank has been slow to make provisions for NPAs and it was even slow to recognize NPAs to begin with. This is because (IMO) it makes loans to non-prime borrowers who often fall behind on their payments but do not default. RBI is getting tough on such cases which means Yes Bank will have to recognize more NPAs and also has to increase provisions until the coverage ratio jumps back up to 65-70%. My estimate is that it can wipe out one year profits.

- RK has the ability to ensure that borrowers pay. With RK gone, bank may see some trouble on recovery side but this is all guesswork and speculation so I am not too much worried about it. IMO Yes Bank is no more a one-man show and a portfolio of 2 lakh crores cannot be managed by a single person. There must be a second tier that has the skills to assess credit and make recoveries.

- With promoters fighting over control, there is considerable uncertainty over when can the bank appoint a new MD and get it approved by RBI. Uncertainty has pushed price lower.

- Media hungry for ratings, is busy digging for red flags.

- Directors resigning won’t go well with investors irrespective of the reason. Investors are choosing to stay away first and ask questions later.

- Ratings downgrade is the latest shoe to drop. It will increase borrowing costs and reduce profitability.

45 Likes

Huh! Now I feel like I underestimated the problem. This is like full fledged well diversified biz by Yes capital. Are they really operating or just shell companies? It seems he wants another banking license. I might be wrong but I smell another Kochar story here. The most knowledgeable economist of this country i.e. Latha V of CNBC said that the bank promoter legally can’t have competing interest in another financial institution. If it is true his continuation on the board will become untenable and rightly so.

I will refresh memory of RK fans here. I will stop with a reminder that the rot is deep and wide and value investors should wait for Mr RK and his team to exit YB completely before taking a call. I am certainly waiting for a new team at YB.

2 Likes

Yes Bank has now turned into the proverbial falling knife. It has always ignited strong passions from both the believers and non believers. While as Yogesh says investors should welcome lower stock prices so that they can load up more, sometimes discretion is better than valour. Just as markets tend to take up the fancied stocks up to unimaginable levels, they also tend to take the currently out of favour (which once were the darlings) down too to such unimaginable levels.

With so much of information dissemination happening so quickly nowadays, there are bound to be over reactions from various classes of investors. There will be some who will pull the trigger first and ask questions later. This often causes big swings in pendulum. The average human mind is capable of handling only so much information and after a point, it tends to induce irrational behaviour.

As @richdreamz has so clearly articulated, stocks that collapse so much dont fall so fast without any reason. Yes Bank has had such falls in the past too but recovered quickly. That doesnt mean it will always recover in such a manner every time. In shaky markets even a whiff of suspicion can lead to the kind of cuts we are seeing in Yes bank.

And usually there is never a single cockroach. As seen in Yes bank’s case the negative newsflow keeps on piling up. We can come up with 10 logical reasons what is wrong with the bank and then the stock price falls becasue of eleventh reason we have not ennumerated.

These kind of falls rarely induce a V shaped recovery. Those wanting live examples can have a look at charts of Edelweiss and IIFL. There are hardly any bounces. If in case of Yes bank too a similar path is followed it will at some point of time stop falling and move in a tight range. In the current market mood I dont think the price of Yes Bank is going to go up in a hurry. There might be the odd 10-20% upmove off and on but when the broad trend is down why should there be any haste in buying? One just needs to have a look at the kind of price damage that has happened in most financial stocks. When a sector previously fancied goes out of favour, this is exactly what happens. These falling stocks will become cheap and cheaper on all valuation parameters on their way down.

Just as stocks posting 52 week highs usually (note usually, sometimes in rare instances, stocks go up without fundamentals in some kind of operator frenzy) have a lot going for them, similarly stocks going down and creating fresh 52 week lows off and on have a lot going against them. Even if we miss the odd stock which has been beaten down without reason and which bounces back quickly, the sky is not going to fall. There are plenty of more stocks to select from.

Stock markets are not here to serve our egos. Sometimes we have to be humble and bow down to what the stock prices are telling us. Yes bank may very well make a comeback but when it does so there will be a lot of tell tale signs.

There will be a lot of arguments and gyaan baazi about efficient market hypothesis and what WB said about them. For all practical purposes, once a sector loses its most favored status, it takes a lot of time for it to make a comeback.

53 Likes

As Yogesh rightly pointed out "High Uncertainty and Low Risk " - with no brainers and not using much of xl sheet as Monish Pabrai - current scenario of “Yes Bank” suits very well - 4th larget Pvt bank with impacable track record of innovate ways to get more CASA deposits in past - some time in 2010, I opened account bcz of 6% savings account far from place around 150 km - plz note , This 3 trillion book not handled by one person - they have right system in place - some mis governs issues - In financial space , if promotors stays in top , somehow they wanna milk from company … our big brother RBI watching closely and won’t go bankrupted … timewise correction but price settle down somewhere - intially I thought 2 times BV and now 1.5 times - … Value is most important as like Quality of comapny - now days , both value and quality not available in market - we have to screfice either one without loosing shirt - I don’t expect my money to be double in on year but I can wait as long as I don’t close account with Yes bank - rejig portfolio and added few more @162 levels and now around 10% my portfolio- I will go up to 20 to 30% of portfolio if price stay below 160 -

4 Likes

Anyone who is investing in Yes Bank should consider following questions:

- Are problems that bank is facing so severe that bank will not be able to recover from them? Is bank’s profits, book value and share price going to go all downhill from here?

- Is the balance sheet so bad that it will wipe out or substantially reduce bank’s book value?

- Is there a systemic company wide issue in how bank lends money or recovers it?

- Are banks borrowers facing problems that they will default en masse?

- Is Yes Bank sole lender to industries or groups that are in trouble?

- Do you have the ability to value a bank based on its numbers and all the qualitative factors surrounding it?

- Do you use quality and sentiment as a substitute for valuation and are you likely to get scared by further negative news flow?

- Are you likely to throw in the towel if the price falls further for any reason? Do you really believe that the bank is a real fraud and the shell around it is falling apart?

- Do you have the patience to wait and ability to hold your position until promoters settle their disputes, bank gets back in the good books of the regulator, balance sheet is revalidated by the next CEO and investors come back?

- Do you think that as and when bank returns to normalcy, it will have a decent profitability and fundamentals for the market to rerate this stock higher that its current valuations?

31 Likes

This is probably why the RBI wants RK to completely sever ties with Yes Bank.

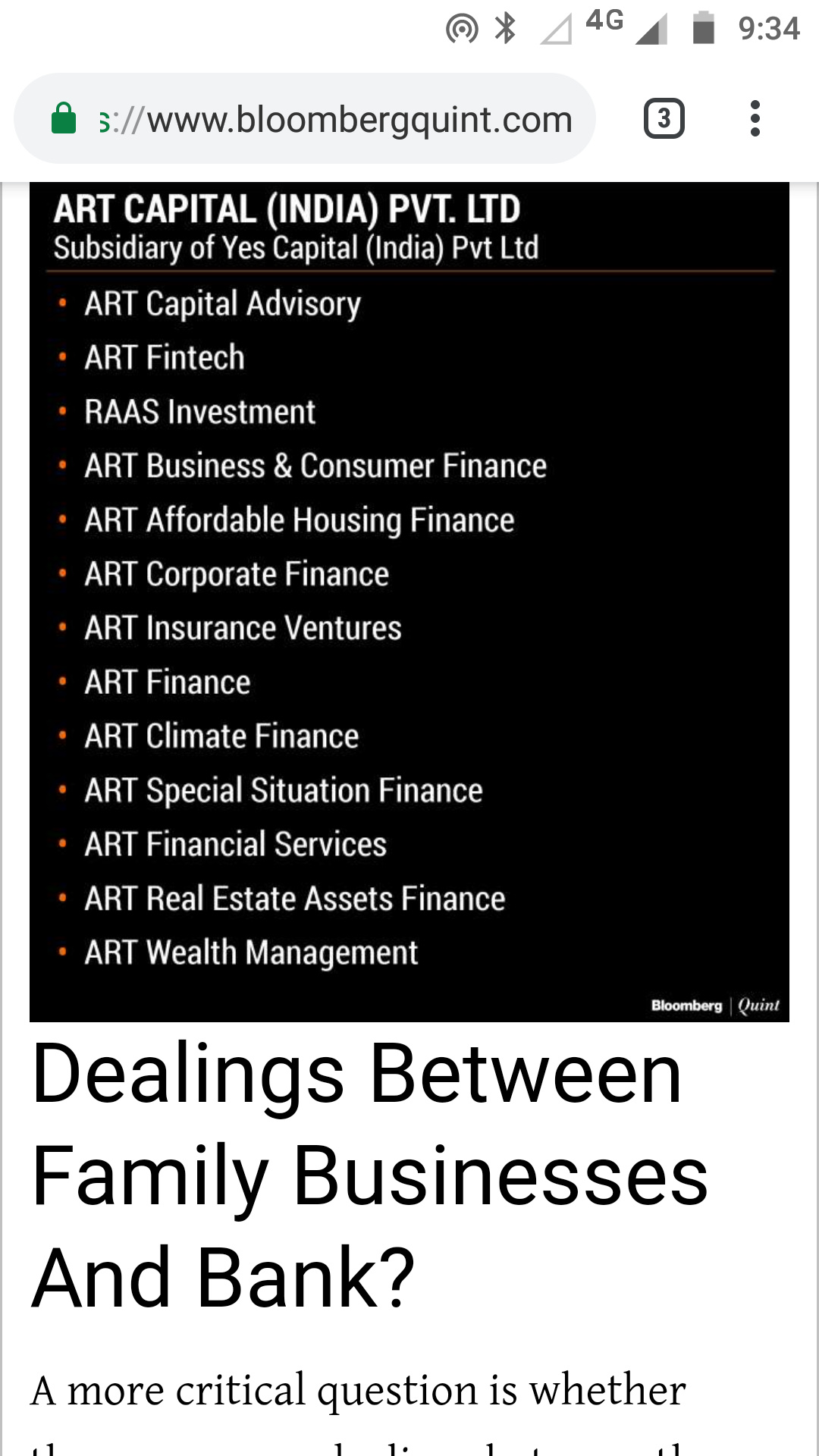

today’s newspaper reads that Morgan credits and yes capital have raised borrowings to the tune of 18000 million. This is a huge number looking at yes banks balance sheet.

This amount has been routed to Art capital, which is completely owned by the three daughters of RK and have nothing to do with the business of Yes Bank.

in other words 18000 million is the liability of RK and not Yes Bank.

Therefore it makes perfect sense for RBI to ask RK to isolate himself from Yes Bank. In spite of him being such a powerful entity in the banks business.

however like Yogesh mentioned only when the new CEO comes in we will know the real picture.

2 Likes

Statement from Reliance MF in today’s ET:

In bad times, even standard practices are made to look like a scam. Information already in public domain becomes scandalous!

Hi

Sorry missed your post. @Yogesh_s has written down succinctly all the pertinent questions we should be asking ourselves.

One thing which I have pointed out earlier somewhere is YBL’s liability franchisee. The market/media/forensic guys will find it difficult to question this side of the business but at the same time this will be undervalued along with the beating the asset side is getting(affect on price). Question to ask is - What is the worst that can happen? Imagine that.

I have always believed “It is better to be out of the market and hope you were in than to be in the market and wish you were out”.

Else I have nothing to add to what Yogesh, @hitesh2710 and @richdreamz have said.

Regards

Deepak

disc: I have no holdings in YBL but have more skin in the game than a stockholder.

9 Likes

disc: I have no holdings in YBL but have more skin in the game than a stockholder.

Hi Deevee,

If you don’t mind can you please explain the above statement.

Thanks

…Excellent self questions of Yogeh ji , kudos … Market not liking downgrades or Rana want to be chairman - reflected in today price - Certainly I like the price and added more today - where do I see the bank next 1 to 3 years ? Let say market falls like 2008-09 and Do I have patience to hold even price go half here ? Yes , as long as RBI exists - If 4th largest banks fails then deep trobule in system

1 Like

Interesting question bank . My questions will start from following

The first question one must ask is why Yes bank inspite of being corporate bank never faced NPA issues like other corporate banks like ICICI , AXIS and SBI …

Then look at last 10 year stock price movement across ICICI , AXIS and YES - and try to understand if the price premium given to Yes bank was justified and if so why … CASA % , Cost to income ratio etc …

2 Likes

Has the RBI audit report of YES bank for FY 17- 18 been released. It was supposed to be released in Sept 18.

Somewhere I read , it may in Feb-2019 …if I’m not mistaken … This is one my checklist though …

Why Yes bank not fairly priced so far even before this correction - Market does not like uncertainty and sceptical about growth and NPA figures - even with 3 times BV we may reconsider with exit strategy - somebody can say , BV can be wiped out if any issues like this with no time - Yes , agree … Risk always there in equities … looking for no brainers - In India , most of them people loose money , not because of business but because of fraud - Here in Yes bank , trust Our big brother RBI and I agree that Big won’t fail and that in banking sector as long as RBI watchdog .

1 Like

I find it very difficult to say what is fair price for leveraged financial services stock . Things can move fast on both sides …

If history is any guide then ICICI bank is great case to study … If we look at how ICICI bank performed after KV Kamath exit . It had a great run in 2000 - 2007 - then Almost 10 years of near zero returns till 2018 … with multiple shocks across years … This was inspite of having great subsidiaries with good market shares .

4 Likes

@kb_snn

Can you share more details of ICICI Bank case study. May be we YB investors can relate some themes with Yes Bank. 10 years of zero return is huge opp cost. By equity terms that’s equivalent to 75 % loss of capital. What was the reason for such prolonged stagnation… Was it overvaluation, loss of RMS, rise of HDFC, NPA and Kochhar Videocon issue…

I agree with you, the same question I would also have. The same question was moving around few months before yes bank crisis. Looks like market knew what’s brewing. At some point Yes should be a good buy, but you never know in financial companies how deep issue is. I will wait and watch with no regrets if I should miss an opportunity.