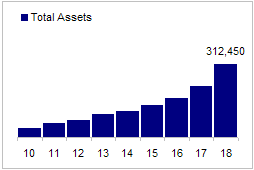

I normally analyze a financial company by calculating P&L items as a % of average total assets.

Yes Bank’s total assets has reached 312,450 Cr.

Source: Capitaline

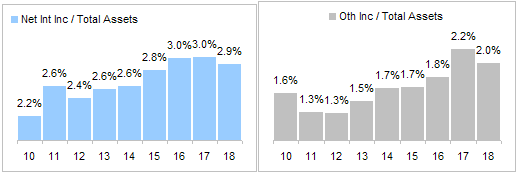

Yes Bank has 2 primary sources of income, Net Interest Income and Fees or Other Income. Both have seen a drop (as a % of average total assets) mainly because of strong growth in assets.

Source: Capitaline

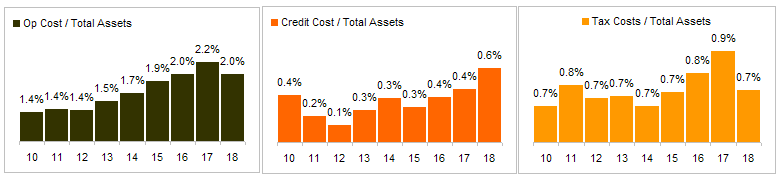

Out the total income, bank has to pay operating costs like salaries, rent etc, make provisions for debt that has gone bad or that are likely to go bad and taxes. Operating cost and tax cost have dropped which has nearly offset drop in operating income (again as a % of avg total assets). It’s the credit cost that has seen a jump from 0.4% to 0.6%. This is mainly because of divergences.

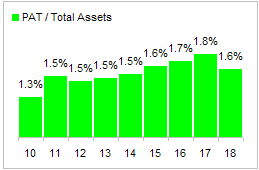

Whatever is left is reported as PAT or ROA when measured as a % of avg total assets. ROA has declined from 1.8% to 1.6% mainly because of 0.2% rise in credit costs.

Source: Capitaline

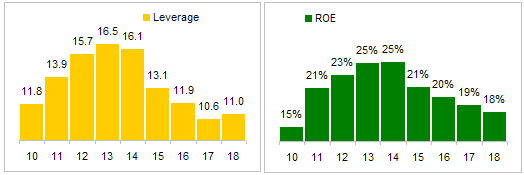

Since banks earn such a low ROA, they leverage equity with debt to earn a decent ROE. Yes Bank’s ROE has steadily dropped from a high level of 25% mainly because of dropping leverage (which is not bad) but this year ROE has dropped because of a drop in ROA (which is bad). Leverage has actually gone up in FY18 but not nearly enough to offset drop in ROA.

Source: Capitaline

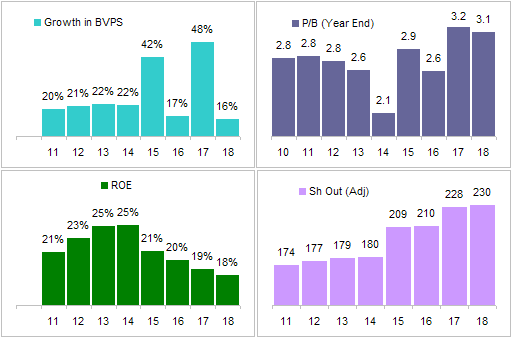

However, an ROE of 18% is excellent for a business that is this large and still growing at 30% with plenty of room to grow. In comparison, HDFC Bank has an ROE of 18% and Indusind Bank has an ROE of 16%. I think ROE should stabilize around these levels. ROE is an important factor in determining Price to book value.

The growth in corporate loan book is astounding at 46% at not such a small base. I think best of private sector banks HDFC Bank, IndusInd Bank, Kotak bank etc. are growing at much smaller pace. For me personally, when a bank grows at such brisk rate - there has to be either a smaller base or bank’s history of prudent conservative lending to make a case for investment.

Almost all operational metrics of the bank have grown at 25%+ except for two that matter the most for investors. The EPS growth is at 17%. The book value has grown from 96.6 to 111.8 - growth of around 16%. When loan book grows at 45%+, I want EPS/Book value to grow by at least 30%. EPS/Book value numbers of Yes Bank to me represents significant dilution + more provisioning.

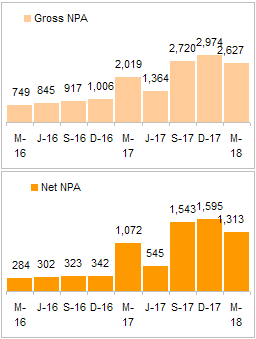

Apart from this, I like to look at NPA ratios in the context of growth. When loan book of a bank grows by 45%+, there is very high chance of NPA ratios decreasing (due to higher denominator) because probability of new loans becoming NPA is pretty low. I like to look at absolute NPA numbers. The even better metric would be to look at (NPA for the year/Loans disbursed in that year) to really gauge quality of underwriting. This ratio is a little bit difficult to get. So when a bank which is not growing reports decline in NPA vs. a bank which is growing at high rate report declining NPA, it really means former is really doing some work on resolutions.

One more point on which I have not done any work is asset liability mismatch for Yes. I have seen several announcements of fund raising in $$. I am not sure if there are corresponding $$ assets or appropriate hedging mechanisms. If anyone has done work in this area, I would be very happy to look at it.

Book value grows at the rate of RoE.

A bank having 10% ROE will see its book grow by 10% in 1 year or 60% growth in book value in 5 years.

A bank having 25% ROE will see its book grow by 25% in 1 year or 205% growth in book value in 5 years.

Further to what @rupeshtatiya said, book value can grow faster than ROE if a company issues shares at a premium to book value. Banks typically issue shares regularly as they can grow faster than their self-funded growth rate (ROE * retention ratio) and also because RBI wants promoters to dilute their stake over time.

Yes Bank has issued a large batch of shares at a significant premium in 2015 and 2017. As a result book value grew faster than sustainable growth rate (ROE * retention ratio). This year again, board has approved raising upto $1 billion of fresh capital which should take outstanding shares to approximately 255 cr.

Source: Capitaline

Note: FY 18 P/B is as of Apr 26 2018.

In general, higher the growth of book value, higher will be the P/B ratio.

Lower growth of EPS and BVPS in FY 18 is due to higher capital base in FY17. Yes bank raised 5000 Cr almost at the end of FY 17 and this capital is not yet fully put to use so it is not earning peak returns. Fy 19 should see ROA pick up a bit but then there is another round of funding which should further depress EPS and BVPS growth. As long as share are issued at a huge premium existing shareholders stand to benefit from additional capital raising.

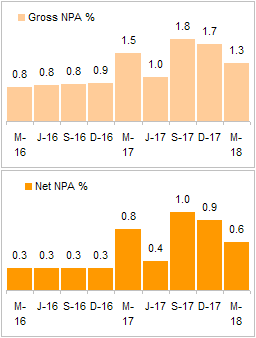

NPA situation is elevated but under control. Real bright spot is that restructured exposure is only 0.16% and Feb 12 circular from RBI has no impact on asset quality (Axis opened a can of worms once the circular came out).

Source: Capitaline

NPAs as a % of assets is dropping for second quarter in a row.

Source: Capitaline

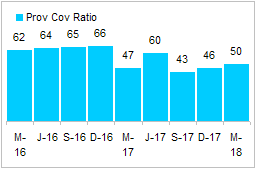

And PCR is precariously low at 50% but off lows and growing

Source: Capitaline

and bank is planning to raise it above 60% by Sept 2018.

I still have doubts over yes bank NPA’s. Yes Bank has large exposure to Power companies wheres Axis has declared them as NPA yes bank hasn’t declared yet, either management is very confident of spreading pain across next 4 quarters & manager NPA in percentage terms of book,

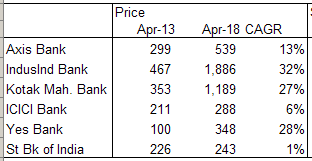

Isn’t it surprising that a bank like Axis reports a GNPA ratio increases of ~2.0% to ~6.8% in two years. What has changed for them in the last two years? Was the economic situation worse than ever in the two year. In fact, things have significantly improved for high stress sectors like steel in the last two years. How come we suddenly we see ~3.5x jump in GNPA ratio?..because RBI (initiated by Raghuram Rajan) took it upon itself to clean the pile of filth hiding under their fat paychecks and huge ESOPs and cosy relations, sweat-heart deals with promoters of the large defaulting businesses groups. It made them disclose what should always have been disclosed…however they chose to support the powerful defaulting business groups(handful…can be counted on fingers), at the expense of the billion souls in the country. One of the key reason for such recklessness and profiteering is because, they are only the managers of the business not the promoters. Whenever there is erosion of capital because of NPA, a part of promoters capital goes to another business, which can’t be acceptable to the promoter. Further, he has to bring in more of his capital to sustain the business. That is where I think, the likes of Axis and ICICI is different from Kotak, IndusInd and Yes. One may argue that these managers have net worth tied in ESOPs, but firstly its not substantial component of wealth, it has been diversified (maybe in offshore assets too) and they can always decide to reduce the exercise price of ESOPs to increase their wealth (the way ICICI Bank did it last year).

I will trust YES management as they will not violate RBI guidelines. Last

year was different - as it was the first such audit for all banks. Even

HDFC bank had divergences.

Market is treating ICICI And Axis as PSU banks and their prices move in tandem with SBI than other private banks. Gap between ICICI, Axis and rest of the big private banks will only widen in future.Prices of these banks started diverging once RBI started Asset Quality Review in 2015.

Yes Bank was at the top until mid 2017 when disclosed divergences. I think over next few months some repricing of risk is possible.

Hiii…What emerges out from this is the significance of promoter’s holding in the bank…a good amount of the top management can be used as a differentiating factor…it also gives out the hope that yes bank management will avoid any kind of shady practices…

But is the current price fair enough to make an entry…on a relative valuation, yes bank is cheapest as compared to other good banks with a substantial promoter’s holdings…Request for your guidance…

First sorry for the naive question…if the bond yields continue to raise… will the companies which borrow from bond markets shift to banks for loans? as anyway i think banks can raise capital from QIP or some low cost instruments…So in this raising interest rates around the world…would banks be beneficiaries ?

In rising interest rate scenario, private corporate lenders will benefit as PSU banks can’t lnd due to RBI restrictions. NBFC will face the heat. Yes bank is very well placed to gain market share further.

It is easy for companies to borrow from banks than to go to bond markets (except for very large companies. Banks (read good banks) generally lend to credit worthy borrowers so others can go to NBFCs which in-turn go to banks or bond markets. NBFCs are growing but they are still small compared to banks. It is the credit quality rather than interest rates that decide if companies can borrow from banks or not. Banks are also interested in making large ticket loans so that is another criteria.

Banks are intermediaries that earn the interest rate spread. i.e. they borrow at a rate lower than the rate at which they lend and earn the difference. In a rising rate environment, their borrowing rate and lending rate both will increase although not by the same amount and not at the same time. This can cause spread to increase or decrease. Unless the general level of interest rates are either too high or too low or changing too fast, banks are good at managing spreads. With current rates in India not too high or not too low, I don’t think rising rates will affect spreads in any meaningful way.

Ability to borrow and lend depends on capital adequacy ratio and not interest rates. With PSU banks reporting losses, their CAR is dropping so RBI is restricting them from making any new loans. CAR of private banks is high so they can continue to lend.

All PSU banks are under PAC which will restrict them from lending untill government infuse further capital. Yes bank has only gray area in power sector exposure however due to high growth it will sustain net NPA figure. Find best in private banking space with current BV. CASA is improving every quarter.

Yogesh…EPS of RBL is growing at faster rate when compared to Yes Bank… while I have both in portfolio, which one is more appealing for further Investments.IMHO RBL is at stage where Yes Bank was around10 years back.