There is no market mayhem, which is causing them to raise money desperately. They have enough money for growth for next few quarters. Plus current demonization will provide them decent CASA for growth.

I feel what have they raised money at 9.5?

There is no market mayhem, which is causing them to raise money desperately. They have enough money for growth for next few quarters. Plus current demonization will provide them decent CASA for growth.

I feel what have they raised money at 9.5?

Thanks to RBI that we know something what many were aware and used to discuss off the record. UBS was ahead of curve in analysing MCA data to bring out true state of affairs. Many dismissed these reports as alarmist etc.

And yes I will not allow a lady to get legitimate due by joining a board since doing a scam is so manly thing.

Though you must congratulate them for the timing of their QIP.

Absolutely! they are still the smartest in the town. Despite the revelation their NPA is better than any other corporate focused Pvt bank. It is also because their credit appraisal is still fairly centralised unlike HDFC.

Strange case of same auditor behind two NPA divergent banks.

Good homework by the journalist…

Hi

Yes bank extends credit line to Myntra.

Rgds

Just thinking out aloud with a little bit of skepticism…

Assuming 2500 jobs are being cut and they were being paid around anywhere between 10000 to 50,000 per month … The annual amount saved may be 24 crores to upto 150 crores… Short term steroid effect to boost the pat??.. If so then the growth achieved through this will be short lived…

Last years pat was 3500 crores… 150 crores will amount to roughly 5% of last years pat…

Disc: invested since 767 levels ( face value 10)…hope my holding period in yes bank will roughly equal buffets favourite holding period…

In my portfolio I have NBFC: Ujjivan (avg: 330), Manappuram (avg:104), HF: GIC (avg:307). Since I wanted to add a banking scrip to my portfolio for a longterm I’m considering “Yes bank”. The only hindrance is the valuation. Is it still OK to enter at this valuation ?

Although PE is a little outside my comfort level, I find this stock the cheapest available new age private sector bank as compared to Kotak, Indusind, RBL etc.

Disclosure: invested at an average price of Rs316. Added more at Rs360.

RBI penalises Yes Bank & IDFC Bank for violations

Penalty was for non-compliance with RBI directions on Income Recognition Asset Classification (IRAC) norms and delayed reporting of information security incident involving ATMs of the bank

Disclosure: Invested in Yes bank ( 7.25 % of my portfolio )

This quarter will be a big test for Yes Bank with Axis bank reporting poor numbers. Whether Yes Bank warrants rerating will depend on the NPA slippages for the quarter. Hoping for a good quarter as advance tax numbers were good.

Yes bank has posted good result (net profit raised 25.1% YoY), but overshadowed by NPA, which has jumped to 1.82 per cent from 0.97. Something concerning !

Divergences are shocking again. This is my biggest concern. We had this issue of Yes Bank under reporting for last year. I thought they would have learnt from mistakes and did the right thing this year. But it is quiet bad under reporting by Rs6,000Crs. As per correct provisions, last year profit was only Rs2000cr rather than the reported Rs3.2kCrs. Based on this, the PE is 35 now and the perception on the management has taken a beating as well.

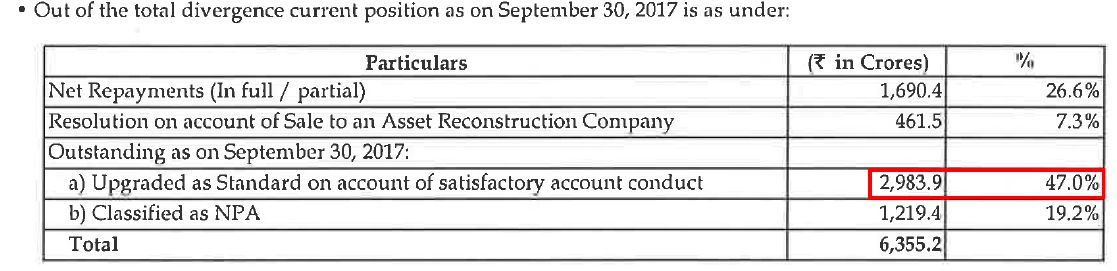

Out of a total divergence of 6355 Cr in gross NPA, 1690 Cr have already been repaid and another 2984 Cr have been upgraded as standard on account of satisfactory performance within six months of RBI calling it as non-performing.

Upgrades are done by the bank so RBI can still come back and call it non-performing. I guess this will go on. What’s more important to watch is the net repayment of 1690 Cr. To me Yes bank was right in classifying these as standard in March 2017 since these were fully repaid within six months. Still 1219 Cr worth of loans were classified as NPA so to that extent Yes bank under-reported bad loans.

What is concerning is that whether an account is performing or non-performing should be like black and white. There should not be so much divergence between regulator and bank. May be that’s what RBI is saying while Yes Bank is trying to avoid volatility in NPA numbers from quarter to quarter.

Axis also reported divergence but Yes Bank had a far higher divergence in % terms. With NPA above 1% of assets, Yes Bank is no longer in the league of HDFC Bank and IndusInd Bank in terms of asset quality.

Disc: Invested.

You are right. There should be no reasons for divergences between regulator and banks. While Kotak Mahindra Bank with a GNPA / NNPA of 2.59 / 1.25 is bigger than Yes Bank, they reported zero divergence. While Yes Bank reported lower NPA, most of us would not trust their numbers. Management is loosing credibility. Perhaps this separates wheat from chaff!

The original research was done by UBS which was ahead of curve in calling YB’s NPA bluff. They maintain 160 target expecting acceleration in recognition of NPA going forward.

Yes Bank Investor presentation and Research report from Motilal Oswal

Investor Presentation: http://www.bseindia.com/xml-data/corpfiling/AttachLive/916331c0-b3cc-4f45-826c-787803d2ff3a.pdf

Motilal Research Report link: http://www.motilaloswal.com/site/rreports/636446920244634303.pdf

Motilal Oswal Report highlights:

Motilal reports are almost always over bullish on stocks under their coverage, so I won’t give any credence to their views.

Overall, it appears to be a big negative that divergence in NPA exists to the extent of almost a billion dollars for a bank which until very recently had a loan book in the vicinity of 10 billion dollars. Generally recent accounts don’t turn NPA so soon.

I would say the risk/reward in yes bank was always unfavourable for a long term stock investor although it turned out to be a great momentum stock and the same has turned negative now.

People who are looking at long term should also understand that the key man risk for this bank is the highest. Although highly paid the second rung management at yes bank hardly inspires any confidence if one goes by the concall.

As long as the research is done objectively, it should be ok. Why are you not saying the same about UBS report quoted by another boarder. Infact there are many others like Bank of America - Merrill Lynch report which said that this is a just a temporary blip and gave targets of 475 and Deutsche Bank gave target of 385 post Q2 results. So lets not discuss the credibility of individual brokerage houses here and restrict the discussion to the merits of the case.

Infact people said momentum turned negative even 2 quarters back but it has not happened and the stock surged to 1900 presplit. I feel there is a lack of clarity in RBI’s guidelines in treatment of NPAs (mind you - these are only guidelines and not rules). Even HDFC bank was asked to consider a big steel account as NPA, post its results (which it did not consider before)and they acknowledged it and that will be factored in soon (maybe in next quarter’s results)