Will this be enough to fulfill all the capital requirements needs?

Was this the result of pledged shares? As company was not interested in dilution for now.

Rudra Share recommend Yash Paper as dark horse

Valuation Conclusion

According to Moody’s Investors Service, higher prices and stronger wood product, paper packaging and market pulp demand offsetting rising input costs and lower paper demand will keep the outlook for the global paper and forest products industry stable. 20% of the world’s population today consumes 87% of the printing and writing papers that are produced every year.

Moreover, the rollout of the much-awaited Goods & Services Tax, the radical step to demonetise high-value currency, the large-scale mobilisation of Ian Dhan Yojana, the Direct Benefit Transfer scheme, implementation of the Real Estate Regulatory Authority, rapid progress in highways and electrification and thrust on housing are undoubtedly examples of inspired action towards progress.

Further, Company’s strong clientele, Scheduled debt repayment in the current year coupled with robust cash flow arising out of increased volumes and new project should help in strengthening Company’s gearing ratio. Further, improved performance should facilitate in further reduction in interest rates, Increased focus on cost reduction measures as well as production of value added products, it is expected that the Company shall demonstrate better bottom line performance which should facilitate in strengthening business profitability & value addition for investors going ahead.

a3b1ea91-1479-4464-8d67-d1f3d3780fda.pdf (92.4 KB)

Highest production of egg trays n exports in March’18

1 Like

If quality is not good then how can Railway serve food in this? Indian Thali need to manage wet items. Customers are of wide varieties there on Railway. If few complain then Railway need to revert back to old style.

Cash Generation is bad and reading capax requirement and plan for future, I see change is that cash generation will remain very poor and debt reduction can take long long time. If they start using more depreciation then due to higher capax ahead, profit may be a big hit downward.

Disc: Not Invested.

Chuk Appoints Distributors in Maharashtra

Q4 results are out. Look decent.

Some points:

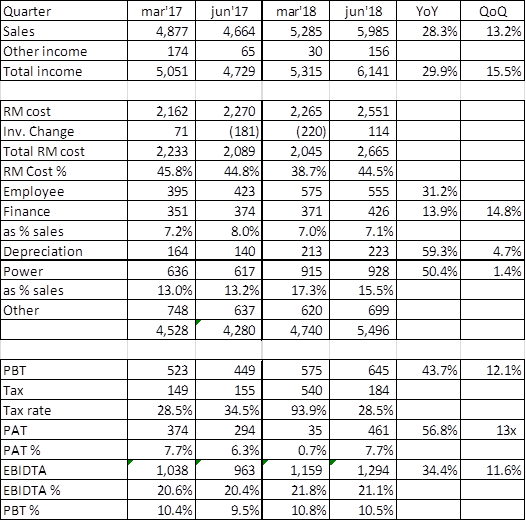

Sales growth – For Q4, sales increased from 49cr to 53cr (8% growth). Excise duty was paid at rate of 5% in FY16 and fy7 and if its impact is adjusted (due to GST being netted off from fy18 sales), sales in q4-17 would have been 46.5cr and thereby Q4-18 sales would have shown a jump of 14%. Sales for FY18 would also have shown growth of 14% if excise is adjusted (instead of 11% shown).

Costs – for Q4, there is significant drop in RM cost which has decreased from 46% of sales to 39%. This is in line with reports of ample production of sugar, which leads to sufficient availability of raw material.

However impact on EBIDTA is negligible due to rise in other expenses.

Employee expenses have increased by 46%, part of the reason could be additional manpower added for chuk plant. Power and fuel costs have increased by 44%.

Since sales are flat, am guessing that the increase beyond normal levels could be for production of chuk products. These have not yet been sold, and are sitting in inventory, which has increased from 59cr to 73cr between mar’17 and mar’18. The increase is substantial from sep’17 inventory levels of 40cr. Its also possible that with sugarcane being harvested and crushed around this time, the company may have purchased and stocked bagasse. It needs to be verified with the management as to how much of the inventory is related to chuk products.

Depreciation for the Q has increased by 30% in line with capitalization of fixed assets. CWIP decreased from 60cr as of sep’17 to 2cr as of mar18 and NFA increased from 92cr to 162cr in the same period, resulting from announcement of commercial production of chuk.

Margins - EBIDTA margin for q4-18 is 21.8% compared to 20.6% for q4-17. PBT margin is 10.8% (previous quarter 10.4%). Tax has impact of deferred tax which needs to be understood.

For the full year, RM cost decreased from 50% of sales to 44% of sales, leading to EBIDTA margin improvement from 17.3% to 20.2%. PBT margin increased substantially 5.9% to 10.8%.

Impact of Chuk:

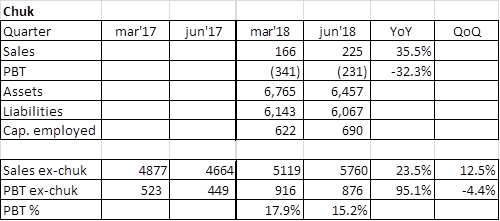

Chuk assets constitute 68cr out of total of 268cr (25%). And it contributed to negligible sales (1.7cr out of total sales of 205cr) and a loss before tax of 3.5cr. The company announced commercial production from 02.01.18 and reported segregation of results between Chuk and Paper from that date onwards. Had loss from chuk not been there, PBT for the Q would have been 9.3cr which is an increase of 78% over PBT of 5.2cr for q4-17. PBT for the year is up 2x and adjusted for this loss, it would have been up 2.3x.

As sales of chuk is ramped up, the overall numbers would improve.

Some doubts/ queries for management (most welcome if those tracking can throw light):

|-| Why sales of paper did not grow since realisations in general have been higher in this quarter due to china issues. Has production been lower?

|-| Need to understand deferred tax aspect.

|-| Are assumptions above correct? Those related to increase in power cost, employee cost, increase in inventory.

|-| Salary to directors have been high at 14% of PAT in FY17. What is the proportion for FY18?

|-| Debt has been flat at around 120cr as of mar17 and mar18. Is this peak debt, or will it increase? When will repayment begin?

|-| 100% of promoter shares are pledged? To whom and against which facilities? What are plans to start depledging?

|-| Company is on record to increase chuk capacity by 2x this year (ie 9 more machines from the existing 9) and further 2x by next FY. What is estimated cost and how will it be funded.

|-| What are expansion plans for regular paper, and how will it be funded?

|-| Are there plans for QIP to fund the above?

|-| As per 2017 AR, debottlenecking was to be done to increase paper capacity from 38550TPA to 45000TPA without much additional cost. Has this been done?

|-| Are all 9 lines of chuk fully operational? What is capacity utilization for chuk and normal paper? Capacity was stated at 11.5TPD as per 2017 AR and was to be increased to 23TPD in FY19. Is this on track?

|-| Has wet plant for bagasse been set up (as was stated in 2017 AR)?

|-| Why company doesn’t give production numbers (volumetric tons) every quarter? Production in tons was flat in FY17 over FY16 (around 36000 TPA). How much was production in FY18?

6 Likes

Thanks for sharing the detailed analysis…you have raised very important questions.

Also whats the update on the trial run of Chuk in Indian Railways…as pointed out earlier by one member there were issues with sogging…

Chuk is 1st being introduced in Delhi habibganj shatabdi and other route rajdhani. Will be extended to other shatabdis and superfast and express trains with pantry cars.

No info on volumes in this article.

4 Likes

Sammy11 sir, net profit sinks mainly due to deferred tax of 3.9cr.Last qtr it was10 Lac credit.So the deferred tax accrued3.9cr against the sale of52cr (?)or sales made on credit and yet to be realised when the payment comes next year. could not understand.

As mentioned in my notes I have not understood the deferred tax aspect.

Why tax rate should be so high? 94% in Q4 and 43% for the whole year while in fy7 they paid 30% tax.

Can anyone explain what could the issue be?

1 Like

Hope the oversupply will bring down the RM costs

No the RM costs wont come down as Yash Papers has long-term (5 year contracts with suppliers)…Hence they are insulated from rise or fall in sugar prices

So, in that case when does their current 5 year contract get over???

Deferred tax impact is due to difference in depreciation calculation of IT and Companies Act on the addition of 55 Cr fixed assets for the new tableware plant…but yes the amount is quite big which needs to be understood

2 Likes

BSE Notification regarding highest production of paper.

This is with reference to the captioned subject, we wish to inform that during the May, 2018 month, the Paper Machine - 2 has recorded highest ever production of Paper i.e.825.50 MT.

The Paper Machine - 3 has also recorded highest ever production of Paper i.e.1943.50 MT during the May, 2018 month.

The Company in overall has also recorded highest ever production of Paper i.e.3575 MT during the May, 2018 month.

2 Likes

Q1 results announced

https://www.bseindia.com/xml-data/corpfiling/AttachLive/e4603cc8-7257-48b2-83cf-ff3941052c32.pdf

Comments:

28% increase in sales yoy and 13% qoq. RM cost was maintained at 45% of sales yoy. Mar Q had seen drop in RM cost to 39% of sales (reason not known). However company has been maintaining 44-45% as RM cost in earlier quarters. Finance cost is around 7% sales, and increased by 14% both yoy and qoq, Depreciation increased by 60% yoy due to Chuk assets and is steady qoq. Similar trend for power cost which has increased 50% yoy and is flat qoq.

EBIDTA increased by 34% with margins at 21.1% (20.4% yoy and 21.8% qoq). Tax rate was 29% compared to 35% yoy (March Q had a huge Deferred tax impact). PBT increased by 44% (margin was 10.5% compared to 9.5% yoy and 10.8% qoq). PAT increased by 57% YOY with PAT margin at 7.7% compared to 6.3% yoy; March Q had seen a much lower PAT due to deferred tax).

Chuk sales were 2.25cr compared to 1.66cr in Mar Q increasing by 36% qoq. It posted loss before tax of 2.31cr, reduced from 3.41cr in Mar Q. Adjusting for Chuk, sales increased by 24% and PBT ex-Chuk increased by 95% yoy.

Ebidta margins are fairly steady at around 21%. There is substantial increase in PBT margins ex-Chuk (from around 10% to 15-18%). If we were to take the numbers at face value, it would appear that at operating level, Chuk and the standard paper business are equivalent, although one would expect margins to improve as contribution from Chuk increases (currently sales are less than 5% of total). Finance cost and depreciation appear to be steady for the standard paper business, however they have both increased due to Chuk project (and hence, PBT margins ex-Chuk in the last 2 quarters are higher compared to earlier quarters). However, this is just an inference, and may be inaccurate.

TTM Eps is 3.5 (appx. 4 if Chuk loss is adjusted). Company will have to show better performance on Chuk if these valuations are to sustain.

Disc. - invested.

5 Likes

@sammy11

Excellent Work Vinay. Just one query, any reason why power cost went up by 50% while sales grown by only 30%? Does company used Diesel based captive power? Generally, Bagasse based paper company have capitve power generation (from recovery of steam of Pulp making process) and hence surprised see such spurt on power cost. Since power is second largest cost element after raw material, it may make sense to get better understanding on this point in my opinion.