Check NSE pls…it is there…and there is no change for last 3-qtrs.

Rgds

RR

Check NSE pls…it is there…and there is no change for last 3-qtrs.

Rgds

RR

Thanks for Sharing. It is Thiruporur on old mahabalipuram road, not Tirupur

My notes from Q1FY18 conference call (might contain errors/mistakes):

Management Commentary:

Recently re-positioned our brand as a complete family entertainment with new slogan.

Land purchased for Chennai park 40 km from Chennai – target FY20 operational

Footfalls:

Financials

Park details:

1. Hyderabad:

a. Footfalls decline? If remove incremental growth due to inaugural offer last year, growth of 11% in footfalls

b. Expectation for year-end 8L footfall, reasons for this confidence? We look at en catchment area 150-200 km. Places like Warangal and Karimnagar. Increase in Business development team efforts and marketing footprints to be expanded

c. Ticket price increase from INR 676-680 to INR 970

2. Bangalore:

a. Macro economic scenario – slowdown in IT

b. Ticket price increase 17%

c. New rides are introduced

d. Expect footfalls to increase if IT picks up

Misc:

Price hike taken in each park - Taken on 1st April:

(avg weekdays)

Bangalore 19% - INR 1300

Kochi 18% - INR 1100

Hyderabad 27% - INR 1100

Post GST, INR 850+GST (28%), Topline reported net of taxes

Non Ticket revenue – good growth 37%

New park - Chennai:

Margins stability – hoping margins will increase 4-5%

Expenses:

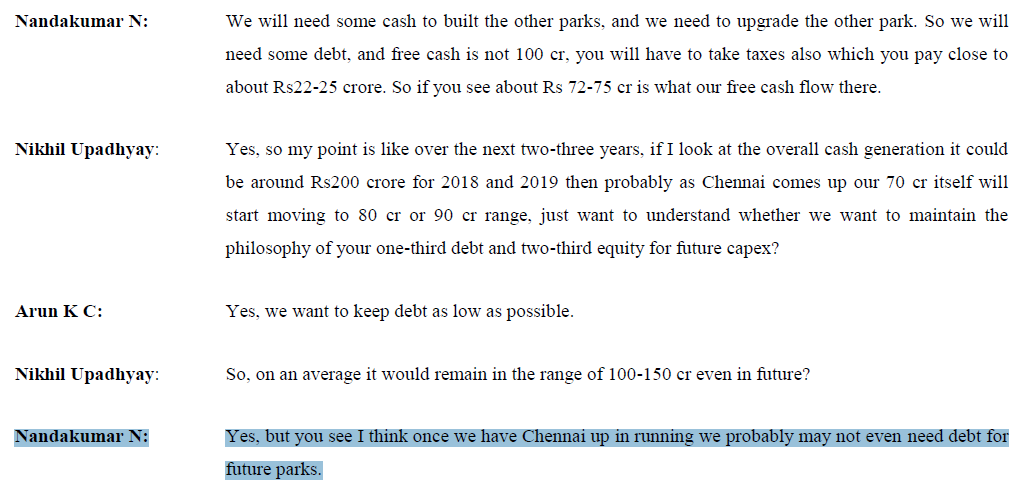

Future plan - what after Chennai?

Need for Debt, why?

Taxation:

Investor presentation:

http://www.bseindia.com/xml-data/corpfiling/AttachLive/23b55b0b-2520-42ce-8ac8-40cbbdcaae51.pdf

Disc: Invested

The June qtr is relatively the most significant of all quarters accounting for the major part of revenue for the year. In the last two years, the distribution of revenue has remained remarkably stable across the 4 quarters with June accounting for ~ 32% of the revenue. This info can help us project the expected revenue for FY 2017-2018 to be about 320 cr ( excluding other income). This comes to an expected growth rate in revenue of about ~19%

Also, another thing to understand about this business is that the June Qtr accounts for almost ~50% of the operating earnings for the rest of the year.

Best

Bheeshma

Further to my earlier post where i had highlighted only the critical aspects, i wish to present a more balanced view. Over the weekend, spent some time analyzing the positive things about the business / stock.

My two cents on Positive factors:

Long runway for growth with multiple growth levers: Wonderla Holidays is in a sweet spot with a long runway for growth.

Some of the Growth levers available:

New parks– In the last 16 years the company has opened 3 parks. The latest one was in 2016 at Hyderabad and has helped the company with increased footfalls. The next one is planned at Chennai for which land has been procured and is projected to be operational by FY 2020. The company has stated in their annual reports their desire to open a park every four years.

New Rides– In the existing parks to keep it fresh, new rides are planned and launched. On an average at least 1 new ride is introduced every year in the existing parks. This adds to the novelty factor as well as aids in bringing in repeat customers.

Non utilized land in existing parks– As per 2016-17 annual report the details of non utilized land available for future development:

Bangalore – 42.55 acres out of total land of 81.75 acres

Kochi – 64.42 acres out of total land of 93.17 acres

Hyderabad- 22.50 acres out of total land of 49.50 acres

There is a combined 130 acres (57% of land parcel) available for future development which is significant and can be used for expansion / new rides / new resorts in the existing parks.

Increased Non ticketing Revenue mix– Non ticket revenue sources include food, beverages, and merchandise from park visitors. Globally the revenue mix of ticket revenue to non- ticket revenue is 45: 55. In India the ratio has been 80:20. This shows the potential available for generating more revenue per visitor which is non- linear in nature.

To their credit, Wonderla has reported a 63% increase in non-ticket revenue last year. Also as per the annual report the average non-ticket revenue per visitor has gone up from INR 155 to INR 214 in FY 2017. Compared to global standards there is still room for further growth of non-ticket revenue share for Wonderla.

Increased revenue from Resort business– Wonderla operates a 3 star 84 room resort in its Bangalore Park. The resort also has a well-equipped board room along with conference facilities for targeting the corporate segment in addition to targeting the traditional retail recreational & leisure segment. As per the latest annual report the resort business generated 11.97 Cr in FY 17 with a 56% occupancy rate.

There is further scope for growth in occupancy rate as well as launch of new resorts in existing parks of Kochi & Hyderabad based on market demand.

Other Positives:

Strong tailwinds for the Industry– Amusement parks and theme parks are part of the leisure and entertainment industry. Globally the Industry is expected to grow at CAGR of 7.5% to reach INR 3.86 trillion. The Indian industry according to research studies are expected to grow at a much faster rate than the global average at CAGR of 19% to reach INR 70 billion by year 2021 from the present INR 30 billion.

With rising per capita income, increasing urbanization and sustained focus by government on improving the physical infrastructure / last mile connectivity, the Industry as such is having strong tailwinds for growth which should be favorable for Wonderla as well.

Management – Among many other things, one of the most significant criteria an investor should look before investing is the quality & integrity of the management as well as to see if there are any actions in the past which are minority shareholders’ unfriendly.

Wonderla is run by the Chittilappilly family, the same group behind V-Guard (listed since 2008) and have a reputation for being able and prudent. Also there have been no instances of any shareholder unfriendly actions.

They have been conservative in capital allocation but forward looking with a good pulse of the trends in the Industry. The management is now investing in the next generation technologies of Augmented Reality (AR) and Virtual Reality (VR) with the first video being shot at Hollywood.

Virtually Zero debt Company– The latest debt to equity ratio stands at a very healthy 0.04. Being in a capital intensive business it is commendable that the capital allocation policy has been prudent with growth coming through internal accruals. Even if the management decides to take on debt for future parks the company has sufficient leverage leeway.

Cost savings through Internal R&D – The management has done a brilliant thing of investing in own R&D capabilities to design and build rides. This gives the company significant cost advantages as it does not have to depend fully on local vendors or foreign suppliers.

As per the annual reports the company is able to internally design and build one-third of the new rides in a park with a cost savings of around 30%. This internal capabilities also lead to faster execution of new rides as well as quicker maintenance / refurbishment of existing rides.

Please highlight if any other key advantage has been missed out.

The rest of my thoughts like the business model , financial metrics and key concerns, if you are interested can be accessed here https://www.stockandladder.com/stock-thoughts-on-wonderla-holidays/

Cheers

Can VR disrupt this business?

@Ravichand08 ,

The other positive points IMO:

Pricing power

Ticket increased 25% but not much drop in foot falls as compared to the price hikes.

Can deploy capital for good returns

ROIC > 40% for mature parks and ROIC > 25% for new parks. And best of all, after Chennai, we might not even need debt to fund future parks or upgrade existing ones. Management commentary:

Good ratings and that too consistently over the period of time.

Great potential to improve

more disposable income, more entertainment options, urbanization etc

First mover advantage and difficult for others (moat?)

My thoughts:

I feel the company has limited pricing power. For me the gold standard in pricing power is ITC. The govt can raise the taxes as much as they want , ITC simply passes it on and the smokers willingly die for it (pun intended). In wonderla’s case there has been a drop in footfalls in existing parks which can also be attributed to increased prices. Also the company employs an active discount strategy for different business segments. Discounts imply lack of pricing power whatever be the reason. For comparison we never hear discounts on cigarettes. You get the drift right.

Not sure how you arrived at 40% & 25% ROIC. I refer to screener.in and it says ROIC of 15.67% which is justaverage / par for the course.

http://www.screener.in/company/WONDERLA/

I am of the opinion that the company surely enjoys competitive advantages but not really sure about the moat part. Think what a player with deep pockets can do ( a la Reliance Jio). Disney has opened their new park at Shanghai in 2015 at an investment of USD 5 billion. Compare this to the budget of 350 crores planned for the Chennai park.

Assuming Disney or Universal studios open a park in a city where Wonderla operates (say Bangalore), Can the company withstand the magic / pull of a Disney without business getting impacted? I don’t think so.

Just my personal views.

Cheers

Ravichand

I don’t know how the ROIC part is calculated by screener but not 40/25% as posted by me also. That figure was taken before just when HYD park was operational (before provisions for tax disputes) from this thread only.

[quote=“Ravichand08, post:174, topic:1053”]

I feel the company has limited pricing power.

[/quote]I agree about the limited pricing power unlike ITC but definitely some pricing power. It would be interesting to note the price hikes CAGR over the past 5 years and footfalls CAGR for the same period. Also note that decline in Bangalore footfalls cannot be attributed to price hikes alone. There are other factors like late school season, political issue (Kaveri river), IT slowdown, etc.

Even Jio is yet to prove if it has really cracked the market! Everyone quotes this Jio example. Even Thyrocare management said the same thing.

Anyway I’m aware of Wonderla’s problem as explained by you (though not agreeing to all of them in the same light, IMO). Wonderla is a good business and worth a look for investments but one should be aware of the risks.

ROIC is a critical factor and I have generally found Screener.in to be accurate. ROIC from couple of other sources for you :

Value Research- 11.75 ROIC

Reuters- 15.80

http://www.reuters.com/finance/stocks/financialHighlights?rpc=66&symbol=WOHL.NS

Cheers

Pricing power agree that they do not have full pricing power but then how many business have full pricing power. Coming to big players, true for future parks but for already existing parks, it is not possible to achieve same return on investment as cost of acquiring land itself would be way much higher (30% of cost is land). The other reason why deep pockets only cannot disrupt current and future park is the in-house manufacturing and maintenance capability which leads to provide same infra at much lesser cost. Now, combine historical brand image with historical land bank with in house manufacturing and maintenance capability. Does not look so easy to replace just by having deep pockets  . Also, target segment for something like Disney and Wonderla is totally different. Wonderla does not plan to get into that segment as of now.

. Also, target segment for something like Disney and Wonderla is totally different. Wonderla does not plan to get into that segment as of now.

As a side note I see there is a fast track ticket with which you can skip queues. The cost of the ticket is more than 2x. But, from below review it looks like it’s difficult do all the rides in one go. So, people are expected to go multiple times to enjoy to the full. I am not sure what % of people do that?

Jatin Khemani of Stalwart Advisors has posted a video explaining his thesis on Wonderla Holidays. For anyone interested in learning more about Wonderla Holidays, it’s a time well spent 51 minutes video.

It appears GST is having a negative impact. The company was forced to increase ticket prices to pass on GST, this along with offseason and rains appears to have resulted in a time correction.

I don’t think so. It’s also a family out time, picnic.

Hi @madhug

in my opinion, Wonderla seems has shrugged off its time correction woes. Confirming its nice operating performance in the June qtr ( its most important qtr) , the price has broken the 50d - an important intermediate moving average after retracing to the 78.6% fib level and now lies just under the 200d - a commonly accepted long term average. From a valuation point of view, I believe its priced at a 25% growth level - something that it has been achieving consistently for the past so many years - before running into a year long speed bump but it seems to have recovered its rudder once again. As is the case with all good businesses the PE has been increasing consistently despite the slowdown - a sure shot indication of how the market perceives the company & its business. The Chennai park when it comes onboard coupled with its intent to add a park once every 4 years confirms its ambition to grow at the aforesaid 25% level.

The unutilized unmonetized land bank (50% of the land it owns is unutilized) would add a further cushion to its valuation in the event it gets monetized.

Negatives

Since this is a business that is heavily dependent on discretionary spending , fluctuations in the economic well being of its customers will always be a threat to footfalls and there is not much the management can do about it except play around with prices a little bit. A family of 4 should spend on an average 6k-10k on a day trip to Wonderla something that pinches the wallet. In times of economic stress , discretionary spending is curtailed dramatically and Wonderlas business is almost certain to take a pounding.

Best

Bheeshma

Disc-Invested and added some in the correction

To me, this looks like a very difficult business. Operating expenses, depreciation expenses, costs for setting up new parks will escalate at a much higher rate as compared to growth in revenue. The only thing going for this company is an ethical management - in my books, this will be a good buy when the next big crash happens. This should and will correct big time. As of today, from a minority shareholder’s perspective, this is a decent business available at a bad price.

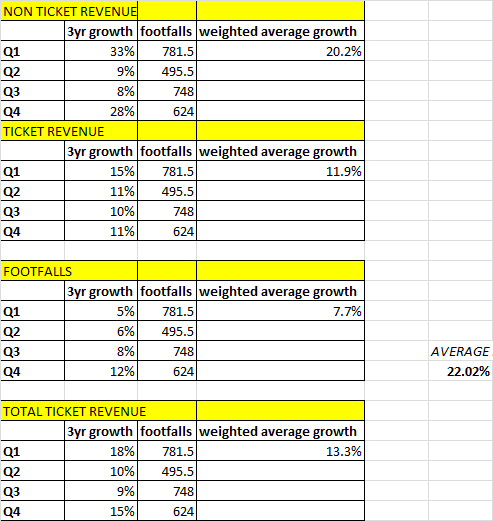

Looking at the 3 yr ticket, non-ticket, footfall history , the weighted average growth in overall prices ( ticket & non ticket) has been 13.3% & average growth in footfalls has been 7.7%. This gives us a likely growth rate of 113.5% x 107.7% = 122.02% or 22% on an average.

Wonderlas capital structure is currently very very conservative and they have indicated willingness to take on debt for the Chennai park. This will improve the PE multiple.

In the recent concall the management has indicated that Goa, Gujarat & Mah are on their radar for possible expansion - these are amongst the richest states in India on a per capita level - so the possibility of increasing ticket & non ticket prices at a rate higher than the current rate is likely in the future

Best

Bheeshma

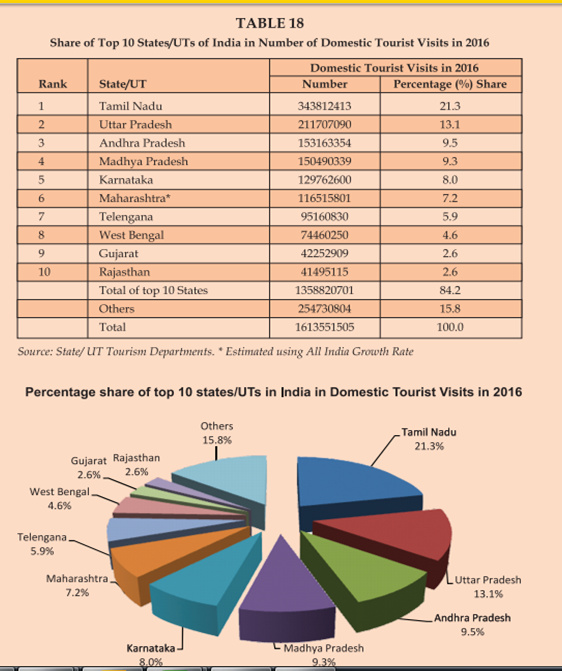

Another interesting table i came across on the ministry of tourism website concerning trends in domestic tourists vacationing in other states of india.

in 2016, there were 161cr all india domestic tourist visits. TN accounted for 34cr of them - a lions share of 21.3%. The data suggests that the southern states depicted in the table accounted for almost 45% of all domestic tourist visits. With the chennai park coming onboard, this obviously will add another dimension to the growth rate, with TN occupying pole position in domestic tourism

Best

Bheeshma