New Chennai Park to drive growth: The Company plans to set up a fourth park by FY20 in Chennai & has

already acquired 60 acres land for the same. The construction for which will began in next two quarters

subject to approvals. The park is expected to be operational by FY21E. This along with the Hyderabad plant

we believe would be the next leg of growth for the company going forward.

EBITDA margins improve due to higher contribution from non-ticketing revenue: The Company’s EBITDA

margins have increased from 18.8% in Q2FY17 to 22.5% in Q2FY18. The share of Non-ticket revenue

improved from 23.1% in Q2 FY17 to 26.9% in Q2 FY18. Higher non-ticket revenue was driven by introduction

of new F&B offerings and sale of costumes which were made mandatory for water rides on introduction of

dress code. The management expects to increase the share of non-ticket revenue to the global standards which

is ~34%. This will further improve the company’s performance.

Well positioned in the amusement park space: WHL is well placed in the amusement park space where it

has strong presence in south India. In addition, introduction of new rides and new park at Hyderabad &

Chennai respectively will continue to keep healthy footfalls growth in coming years. Also, the company’s

focus on increasing non-ticket revenues is expected to drive margins.

Wonderla launches space flying experience ride at Hyderabad park7c5eb5a0-2d2b-4921-8a5d-c764eb0a60ab.pdf (144.8 KB)

Has sanjay bakshi exited wondela , found somewhere written that sanjay bakshi has exited

no sir…not as per Dec shareholding pattern.

GST for Theme parks and water parks reduced to 18% from 28% in the GST council meeting. Should help Wonderla

The company had said the last year that q3 footfalls were low on account of demonitisation. However the footfalls of q3 fy 18 were even lower than qe fy 17. Stagnating footfalls is a big cause of concern for a company that trades at such valuations

Disc: not invested

It’s a stock for very very long haul. Just keep accumulating it through SIP. There will not be any fireworks  in this stock. However, it will compound wealth over 10 years with a 80%+ probability. One can look at life cycle of similar operator in US NYSE:FUN

in this stock. However, it will compound wealth over 10 years with a 80%+ probability. One can look at life cycle of similar operator in US NYSE:FUN

i thought of performing an analysis on the profitability of Wonderla after hyderabad park became operational. Company doesnt provide any details relating to park wise profitability so i had to take certain assumptions for arriving at the impact

Observation 1

Revenue for 9 months based for bangalore and Kochi park for the last 3 years have more or less remained stable- May be because of introduction of introduction of Service tax in FY 15-16 on amusement parks and Introduction of GST @ 28% in the current year. However the government has reduced the rates of GST to 18% from Jan 18. Hope that a stable tax regime continues from hereon.

| 9 months Comparative analysis | Rs. In Lakhs | ||

|---|---|---|---|

| Particulars | 2017-18 | 2016-17 | 2015-16 |

| Bangalore- Park | |||

| No. of Footfalls | 7.6 | 8 | 9.18 |

| Avg Ticket Revenue | 961 | 931 | 791 |

| Avg Non Ticket Revenue | 268 | 213 | 170 |

| Revenue from Park | 9,340 | 9,152 | 8,822 |

| Bangalore- Resort | 850 | 943 | 815 |

| Kochi | |||

| No. of Footfalls | 6.9 | 7.7 | 8.23 |

| Avg Ticket Revenue | 724 | 696 | 659 |

| Avg Non Ticket Revenue | 224 | 154 | 137 |

| Revenue from Park | 6,541 | 6,545 | 6,551 |

Observation 2

As per my assumptions the company is yet to reach cash break even for hyderabad park. However it has reduced its cash loss from 17 Crores to 5 Crores for 9 months. i believe hyderabad park will reach reach from loss to profit in the next 2 years and from then this should become an interesting story.

i have assumed the operating expenses from Kochi and Bangalore park is same for all 9 months period for FY 15-16, 16-17 and 17-18.

Attached my calculation sheet

Disclosure: Invested. on the assumption that hyderabad park will reach profitability and as the profitability for last 3 years has been adversely affected by impact of indirect taxes collected from customers which has reduced the demand.From hereon its effect should stabilise

Wonderlaa 9m analysis.xlsx (10.6 KB)

will the kaveri river water disputes going on, political pressures effect the park construction in chennai ?

Even IPL in chennai seems to be jeoperady due to this

any views will be appreciated

Sir,

What is the discount rate for the DCF target of Rs 377.

Regards,

Santosh

Management interview about the current business environment

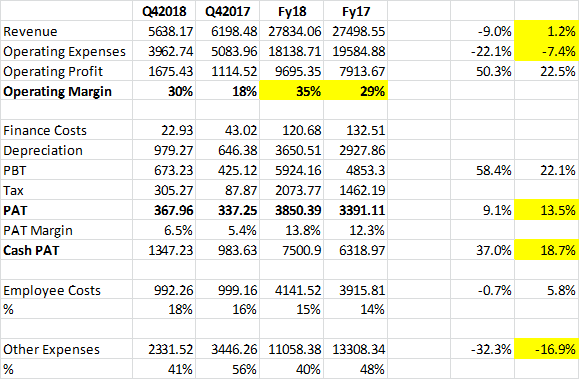

Wonderla came out with a mixed set of results. The topline is more or less flat YoY but the operating margins have seen a substantial jump to 35%. The main reason driving this is the reduction in costs. Operating Expenses have come down by 7.4% over Fy17. Employee costs have actually gone up but Other expenses have seen a steep reduction by almost 17% over fy17. It will be interesting to see where these reductions have taken place.

Footfalls

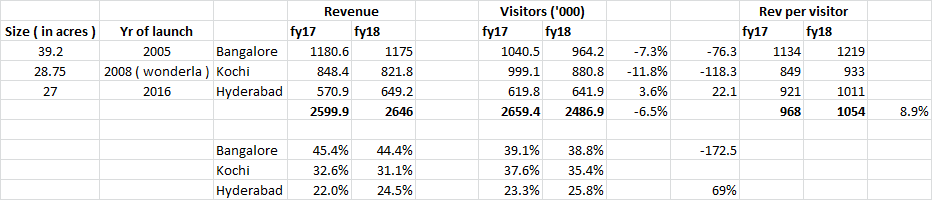

The main thing worrying investors is the reduction in visitors. YoY visitors across all parks have come down by 1.725 Lakh or 6.5%. This reduction is mainly contributed by Kochi - their oldest park. 69% of this 1.72L reduction is accounted for by Kochi. Bangalore also has seen a reduction in vistors by 76000. Both these parks are quite old and mature. Bangalore was launched in 2005 while Kochi was launched at Wonderla in 2008 and has existed since 2000. Both these parks get roughly the same number of visitors i.e between 8L to 10L per year - which seems to have topped out.

The Hyderabad park however is quite new and comparable in size with the Kochi park. it was launched in 2016 and footfalls have been increasing here. YoY footfalls have increased by 3.6%. Over time one can expect moderation of footfalls in the older parks while footfalls in the hyderbad park catch up to the run rate of the other ones. Hyderabad received 6.41 Lakh visitors in fy18. Hyderabad contributes to to about 1/4th ( 24.5% ) to the topline , up from contributing 22% in the earlier year.

In sum, the degrowth in footfalls is not as terrible as envisaged - its the nature of the business - the older parks overtime get a stable number of visitors and top out at some point ( unless some reimaging exercise is carried out or there are some new rides). The newer parks drive the footfalls and there will be this undulation in the footfall curve.

Best

Bheeshma

well, if wonderla doesn’t open new parks frequently (may be one new park in every couple of years ) its a pretty risky game .

I think sooner or later mature parks are going to have stable number of visitors over time. But how they can grow is by

- Increasing per ticket price of parks

- Opening new parks (which management indicated they would)

These may have been discussed earlier. They can do number 1 if if there is not good competition available, competition being other avenues of entertainment and their experience vs others. Other risks still remains though. Its not gonna be risky bet for sure but I think one needs to evalaute risk/reward game here.

Wonderla is simply a cash cow since very minimal maintainance capex is required. Not always do we need growth in top and bottom line. What’s required is steady cash flows too. .