One more thing is that South does not suffer from winter and the kind of water rides wonderla offers , a always hot belt will provide business 365 days a year. So, it makes sense to occupy southern locations first. Above data seals it further with additional reasons

1 Like

-

Cannot seem to find a single line of data that shows that the footfall will decrease… so that is good.

-

Management looks top class. Read the credentials of the people on the front line.

-

50% fall in EPS. Yet, cash from operating activities is only 10% lower. honest accounting practice. No doubts there.

-

It has a PE of 54…I wonder if it is okay to buy at PE 54 in the name of growth.

-

company does not generate FCF, too much investment needs to be done every year. Last year 145 Cr, this year 115 Cr invested in fixed assets… but not by raising debt, but from its reserves and profits. So that shows that the management has a long term view… a sensible bunch.

This stock should be bought in a correction.

1 Like

28% GST has been levied. However, I think, the GST it receives ought to be adjusted against the GST it pays; Incoming GST adjusted against Outgoing GST…

Wonderla is spending quite a lot on plant and machinery every year, as it is a growing company… so this GST is all adjusted. Meaning, the company does not have to pay it back to the government… if there is any increase in price in name of gst then it will only increase profit.

1 Like

A report from Motilal Oswal

http://www.motilaloswal.com/site/rreports/HTML/635566606138525979/index.htm

Wonderla is a clear cut winner, mainly due to its management. Adlabs is losing money inspite of it being a costlier affair.

Wonderla won’t come to mumbai, because it would have competition from four other sites.

1 Like

Don’t know if you run a business or not, but all gst paid on supplies is a cash outgo. Say on 100 rs supplies 28 rs extra gst is paid by co. Now if the same supplies with value add is sold at 200 rs with 28% gst comes to 56 rs levied extra to customer. This 56 is to be paid to govt. With 28 rs. Credit received. So total outgo is still 56 rs. @ 28%, paid once 28 rs on supply and once 28 rs after sale. Where is the benefit to co.?

1 Like

Amit,

Wrt to your point on input tax credit, here is the management’s reply -

an excerpt from the Q1FY18 concall:

Rashesh Shah: Sir, just wanted to know what kind of input tax credit you would be getting so what could be your effective tax rate on GST. Would there be some benefit that would add to the margins?

Nandakumar N: Yes, input tax credit is very minimal, so if you see it is about 5% to 6% in our business.

Rashesh Shah: But that would not be added to your effective tax rate would come down by 23% or something like that?

Nandakumar N: Yes, it will be a 23%, but that has already been factored in the post tax environment also, we have been taking the credits, so incremental credit what we would get between GST and service tax environment is only the trading margins on which we diverse the service tax input credit, which is a very small portion.

Rashesh Shah: Thank you.

1 Like

It is just not the the gst%, but gst of sales turnover minus gst on sales and gst on expenses (fixed assets, repairs, salaries etc) made.

Companies also have a way to defer these taxes and adjust them against expenses.

GST would only be an opportunity to increase price.

This is Jan 2015 report.

Chennai Wonderla:

Competitors:

- There are already 4 players in chennai: Queensland, Kiskinta, MGM and VGP. Queensland is the market leader who have 200 acres of land bought around 50000/acre. Have lot of pricing power on the lower side. Ticket price was 350 rupees last year, now revised to 550.

Location:

- Wonderla is going to be in Thiruporur on the OMR road. OMR road itself far-off location and Thiruporur is even off in that road. 55KM from Koyambedu bus stand or 42 KM from Guindy.

Except that the adjacent road ECR already having 2 theme parks (MGM and VGP). Other side adjacent road ( GST road ) there is another theme park called Kiskinta. So it is going to be 4 theme parks in South Chennai once Wonderla comes.

- None of these parks can beat the location of Queensland which is very near to city ( 22km from Koyambedu & you have to cross queensland to enter Chennai, so handy for visitors from other districts ). But it is tough to buy land there due to cost and to compete with Queensland.

Performance:

-

Queensland seems performing very well. On Gandhi Jayanthi leave had 10k footfalls and on Kanum Pongal festival clocked a record 15k footfall. On holiday seasons getting around 5k footfall, in weekdays might be around 2k. All other theme parks are performing poorly comparing to that. It seems MGM had 5k footfalls on Kanum Pongal which is their highest number of footfall in years.

-

Wonderla will beat down MGM, Kiskinta and VGP. But Queensland will continue to be market leader. After the initial euphoria dies down, Wonderla might be able to clock an avg of 2k footfalls a day.

Risks:

- A new park called EVP started just opp to Queensland but closed down due to accidents and aftermath didn’t handled properly. So accidents can be a big threat. Needs to have political clout and learn the art of greasing the local political hands when different issues arise.

My View:

- High capex business.

- Business is very easy to understand & predict return.

- Growth will be average but consistent in long term.

- There will be lot of hard cash flow. Management reputation is very important - which is very good in Wonderla’s case.

- No one can be moat in this business due to nature of the industry.

- Wonderla may be the only one organized player in the industry but they may have strong competition from regional players due to first mover advantage.

- Invest for long term. Buy when share price falls.

Disclosure: Have positions for tracking.

15 Likes

The database https://rcdb.com/ gives a listing of all the roller coasters existing in the world today. Its pretty detailed. After all, whats an amusement park without a roller coaster and a serious contender should have at least 1 RC ride.

Some interesting statistics

-

India has a total of 89 roller coaster rides while China has 1143, that is ~13 times more than India. Since both our cultures & population size are comparable ( roughly though ), this gives us a sense of the opportunity size. One could argue that China per capita GDP & Income is higher than India though and that would be a valid point.

-

of the 89 rides, the 3 parks of Wonderla account for 13 of them with an average of 4-5 roller coaster rides per park. This would imply that compared to other parks with an average of 1-2 roller coaster rides the ticket cost per roller coaster is cheaper. Wonderla is a full service amusement park with roller coasters categorized into thrill, extreme , kids and family.

Recoil is their flagship extreme roller coaster ride and has 3 inversions ( loops) , traveling at 47 mph for about 2 minutes. It has a capacity of 760 riders per hour manufactured by the dutch company Vekoma ( for more info - Recoil (Wonderla Hyderabad) - Wikipedia).

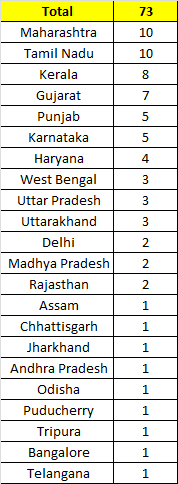

- India has a total of 73 amusement parks distributed as follows -

As can be seen south india account for ~40% of all amusement parks in India & tamil nadu along with maharashtra account for 10 each.

As far as chennai goes, Kishkinta, Queensland and VGP are parks with 2 roller coasters each while MGM Dizzee World has 4 roller coaster rides of a type comparable to Wonderla ( Reindeer Coaster, Roller Coaster, Tornado and Water Coaster). Its Roller coaster ride however has only 2 inversions and the duration is 1.10 minutes compared to Recoil (which has 3 & is ~2 minutes). Neither Queensland, Kishinta or VGP have any extreme rides. They seem to be operating more in the family + kids kind of segment which could possibly explain their low ticket sizes.

The data from the aforementioned website also throws some other interesting insights - related to real estate

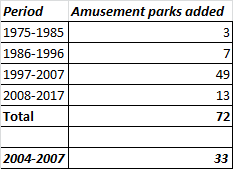

This is the data for amusement parks added in 10 yr blocks

From the data it can be seen that the max amusement parks were added between 1997 - 2007 - 49 to be precise.

1997 - 2003 was a period of plummeting real estate prices in India ( 16 parks added in this period) while 2004 - 2007 was arguably the biggest boom in real estate india has seen (a whopping 33 parks added) ending as we know how it ended. From 2008-2017 only 13 parks have been added - of these 13 parks , 11 have been in the period between -2008 - 2012 ( again a period of boom for real estate).

In the last 5 years only 2 parks have been added ( imagica and wonderla hyderabad)

The conclusion that i can draw from this is that in a period of booming real estate parks added grows significantly - and in a period of slow real estate it contracts significantly - an unmistakable sign that amusement parks is also a play on the real estate cycle

Best

Bheeshma

21 Likes

Queensland will surely be leader by footfall. But the quality overall is very poor and it attracts a mass of crowd who will definitely upgrade to better parks once their affordability improves. I have been to all the parks recently and Queensland is very average and feels unsafe by crowd quality. So I believe Wonderla given their track record of impeccable management of parks will stand to gain. Location wise I believe target audience is concentrated on South chennai. Queensland is in West chennai. Hence I still feel Wonderla location is well thought of.

Discl not invested but looking to enter at lower levels

A month ago I visited Wonderla Bengluru park on a Sunday afternoon. Here are my notes from the visit.

Pros

Park is well built and looks new.

Lots of rides for all ages.

Rides were nice.

Cons

Park looked empty on a Sunday afternoon until I went to the water park area. 70% of the crowd was near the water rides. That area was crowded as it occupied about 20% of the total park area with 70% of the crowd.

Few rides were not operational. Some rides especially for small children had no attendant. I had to call the attendant to operate the ride.

Many of the rides felt like vertigo inducing experience and were similar to each other. I felt the rides were scary than amusing. (and I have been to many amusement parks so I can relate to my earlier experience). this may cause at least some visitors to not return.

Some Wonderla employees (in uniforms) were picketing just outside the park entrance.

Overall, I think there is a demand for a water park as majority of the crowd was in the water rides. this was on a cloudy and not-so-hot Sunday afternoon. I think I paid something like 1150 per head so I am assuming others paid somewhere in that range too. to me it looked like people came for the water park only although there was no separate ticket just for the water park rides.

I have been to other water parks around Mumbai-Pune area and I think the pricing is around 800 to 1200 depending on the season and day of the week. That means wonderla is able to offer an entire amusement park at the price of a water park.

However, I also felt that at present demand exists for water parks which will need a third of the land and presumably will have smaller capital cost to set up. I think a water park close to city (Wonderla bangalore is about 30 km from city center and it takes an hour to 2 to get there) at the same price (800-1200 range) will be a better business model than a bigger amusement park far away from the city. Proximity to city will draw crowds.

Long term there will be a demand for a well managed amusement / theme park but as an investors I would prefer the water parks than amusement parks.

14 Likes

1 Like

For capital reinvestment opportunities to regularly present themselves , there needs to be category growth. Category growth in the amusement park business has dwindled with only 2 large parks added in the last 5 years. Its good to see other operators expanding the category.

Has there been any thought given to the traffic chaos in Bangalore. I was in Blre recently for 3 months and couldn’t go anywhere unless I spend a couple of hours by car. The roads are terrible with traffic at snails pace. I couldn’t go to wonderla, as I couldn’t see the point of spending close to four or five hours in traffic with two small kids. I am sure I am not the only one who has reduced their travel in Blre. Many IT professionals I spoke to, would rather take their kids to a nearby mall or some activity nearby rather than spend the Saturday driving through Blre madness. How is this going to affect the long term business model? ( I live in Australia, I genuinely can’t picture Blre traffic in ten years time)

2 Likes

Metro network is spreading rather fast in Bangalore and the nearest station from Wonderla will not be too far, could be about 13 - 15 km… That will make Wonderla more accessible to city.

3 Likes

Con-call transcript pertaining to Q2FY18 results

http://www.bseindia.com/xml-data/corpfiling/AttachLive/a29bd151-7091-4205-8a20-4fce177df210.pdf

Q2FY18: Unseasonality impacts footfalls, average non-ticket revenue increase

Wonderla Holidays (WHL) in 2QFY18 posted revenues of Rs. 49.4 Cr (up 1.3% Y-

o-Y, down 52% Q-o-Q) due growth in average revenue per visitor by 7.1% Y-o-Y

which was offset by decrease in footfalls by 5.4% YoY due to unseasonal and

excessive rains across markets, price hikes and GST impact. The EBITDA of WHL

increased 21% to Rs 11 Cr due to strict control over cost overheads and increase

in average non-ticket revenue per visitor by 25%. WHL posted PAT of Rs 2.3 Cr

(down 37% Y-o-Y, down 91% Q-o-Q) due to higher interest costs and

depreciation costs of new rides.

Kochi and Bangalore Park showed stellar average ticket per revenue but low

footfalls whereas new Hyderabad Park witnessed good footfall growth. The

Company has acquired 60 acres of land in Chennai for the new Amusement Park

project. Construction is expected to commence within the next 2 quarters and is

expected to be operational by FY21. This along with Bangalore and Kochi and

new park in Hyderabad are expected witness good footfalls going forward given

the rising trend of consumer discretionary spends.

2 Likes

Given the strong footprint in South India and robust expansion plans, WHL is well positioned in the amusement park

space. However, price hikes, higher taxation, and delayed implementation of Chennai plant are some near term concerns.

We thus recommend a HOLD on WHL with a DCF target price of Rs 377, upside of 4% from the CMP.

Key Highlights

Footfalls witnessed de-growth in old parks: WHL recorded a flattish revenue growth in Q2FY18 due to 5.4% decline in

footfalls with Kochi contributing the most due to steep price hikes and excessive rains during Onam season. Taxation has

been a big hurdle for the company as it has to pay 28% GST now vs. 3% in FY14. The company aims to bring back

footfalls by introduction of new rides and incentivizing days like Tuesdays and Wednesdays.

Hyderabad park witnesses breakeven in 1st year, healthy revenue growth to continue in future: The Hyderabad

Parkbecame operational in April, 2016. On a half yearly basis, it has posted 22% increase in revenues and 20% increase in

average revenue per visitor and has become EBITDA positive. The company expects to record ~10 lakh p.a. footfall by

the end of next three years. In addition, as the restaurants at Hyderabad Park are owned by Wonderla, we believe the

company will realize higher margins in F&B segment positively impacting overall margins.