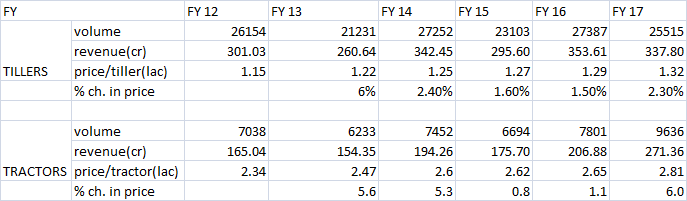

last five yr tiller and tractor number for VST. Management has guided for around 5% growth in tillers and 15% growth in tractors.

Volume growth may vary depending on monsoon,govt policy…etc.

Value growth depend on price,competitiveness,HP range.

In FY 17 value growth for tractor segment is 6%.Probably due to higher HP tractor (27 hp) launch.

During AGM, CEO mentioned that EBITA margins will remain around 16%.It may increase with increase in higher HP tractors which is expected in FY19.

ESCORTS ltd which has tractors ranging from <30 HP to >50 HP, has EBITA margins of around 10%in fy17.

Few important points from above report:

1.86% of farm holdings are small and marginal.

2.Tiller industry remains underdeveloped currently developing 35k-40k units/yr.

3.Two Indian companies VST,BEGALURU and KAMCO ,KERALA caters to 68% of market share.(45% VST, 23% KAMCO).Remaining 30% is power tillers imported from China . Total capacity of Indian manufacture is 90k units/yr. They are unable to utilise full capacity due to Chinese competition.

4.Chinese tillers are 10-20% cheaper than domestic tillers hence the demand for imported tillers is growing. The market share of china tillers has grown significantly from a low of 10% few yrs back to 30% currently.

5.Subsidy was given to all power tillers ,i.e. whether imported or indigenous, provided these tillers are tested by testing institute and meets the minimum performance requirements. Many power tillers importers have not submitted samples for testing but still continue to be eligible for subsidy.

Chinese imported at cost of 65 to 75k, gets subsidy of around 60k but farmers are being charged at 1.25 to 1.5 lakh. ( 2 to 3 times import price.)

5.Many companies(Shrachi and Kranti) import power tillers from China .However they claim as manufacturers and quote their tillers as indigenous.

6.Imported tillers lacks in after sales service and concerns about availability of spare parts.

7.It is difficult to find out the performance difference between indigenous and imported tillers.

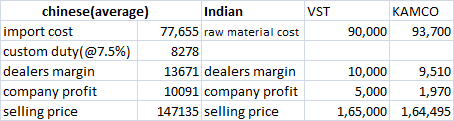

8.look at the table to know the price difference between domestic and Chinese players

Recomendations:

1.Domestic tillers must b given preference over imported one

2.Increasing the customs duty up to 25% from current 7.5% on imported tillers.

3. Import quota for power tillers may be fixed as 10% of the total annual market of power tillers in India.

4.Making regulations and internal taxes less onerous to domestic manufacturers to boost make in India .Ways to incentivise the domestic industry through production subsidy/duty exemptions on assemblies and spare parts. Export related incentives for domestic manufacturers. Lower rate of interest(7%) and simplifying norms to extend institutional credit for purchase of tiller. Simplify procedure of subsidy distribution and timely release of subsidy.

5.Indian power tiller manufactures to be cost competitive with china, upgrading quality of tillers, expand dealers network and availability of spare parts.

6.Improve the quality of evaluation/testing of tillers by testing institute. Making more stringent norms for standard testing and for repeat/supplementary testing.

VST has entered into technology transfer agreement with Korean company M/S Kukje machinery Co. Ltd for transfer of technology to manufacture higher Hp tractors in India. 0530c636-5015-4cf1-8415-a078c82647ea.pdf (252.6 KB)

Tillers segment has shown good growth for the month. Difficult/wrong to assume the same for future considering various factors like subsidy which influence tillers sales.

Tractors growth story continues. Overall it was very good month for tractor industry with big brothers of VST recording good sales. Mahendra tarctors domestic sales increased by 52%, Escorts tractors domestic sale up by 34% for the month of Sept-17.

Check Jana blog. On few posts he has discssed beautifully the importance on capital structure n ROCE. Also on VP check thread related to investments ,they are worth reading again n again. In case you are not aware of these terms, would suggest to read good investment finance books to start with. I learnt a lot from Pat Dorsey five rules of investment

Tractors have played major role in farm mechanisation over the years. With growing population ,decrease in percentage of population engaged in agriculture & increasing urbanisation it is important to increase the productivity/hectare by farm mechanisation to meet the ever increasing food demand in India. Govt has set seven year plan to increase farm power availability from current level of 2.02 Kw/ha to 2.8 Kw/ha by 2022 and to establish customer hiring centres in 2.80 lac villages and it has released substantial amount compared to previous years for this purpose.7 years Action Plan .pdf (996.2 KB) fund rel.pdf (482.1 KB)

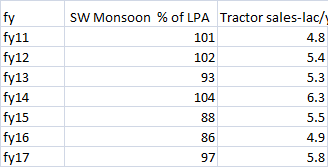

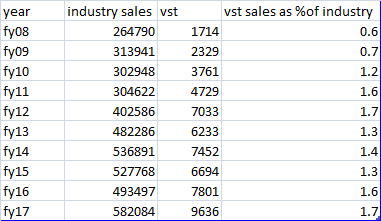

Indian tractor industry has grown gradually to reach nearly 6 lac tractor sales in fY 17. If we look at the past few years tractor industry sales has direct correlation with the southwest monsoon in India.

(source:aurum eq/Mahindra ar)

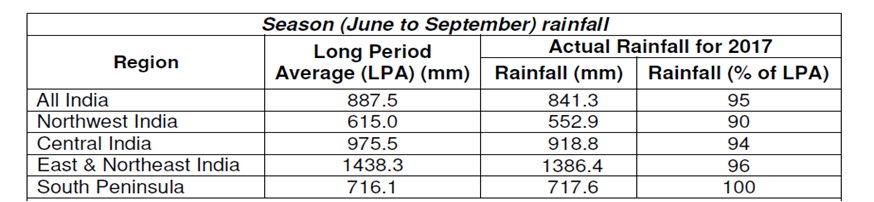

Monsoon during the year 2017 has been slightly below the normal (95% LPA) . Gujarat /Maharashtra and southern states have received normal/excess monsoon which are important markets for VST tractors.

VST has been focusing on growing tractor segment from last few years . Tractor revenue contribution has grown from low of 162Cr (30%)in FY12 to 271Cr (39%)in FY17. Compared to overall industry sales ,VST tractor sales is minimal ,which gives them large opportunity to grow.(table)

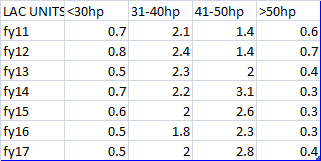

VST was selling low Hp tractors 18.5, 22, 17& 27 Hp(launched in fy16) mainly in the Guj and Maharastra where low HP tractors are preferred by cotton/sugar cane farmers due to small width of tractor. Once a dominant player in compact segment (<30 HP) VST has lost market share with competitors entering this segment over the years to current market share of 30% in compact segment. Tractor industry growth was mainly lead my higher HP tractors as evident in the below table.

source:eaurum eq.

I have interacted with few farmers and few points:

*most farmers prefers higher HP (35 to 45hp) tractors.

*low HP tractors mostly used to supply water.

*brand of tractor doesn’t matter much to them.

*most important is after sale service

*prefer to own tractor than hiring for rent.

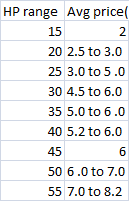

VST has plans to enter higher HP tractor segment from FY19 for which it has recently entered into technology agreement with S.korean company . Selling higher HP tractor will increase the revenue/tractor and margins. Below Table gives rough idea about HP range and price of tractor.( it is not accurate data ,price may vary significantly base don certain models/specification…I have taken average based on availavble data)

Competition and capacity: there are more than ten players with excess capacity which makes tractor industry highly competitive which can put pressure on margins. It is difficult to get exact market share and capacity as many players are unlisted. Mahindra has 44% market share and its capacity may be in excess of 3 lac/yr considering they have sold around 2.5 lac tractors in fy17. TAFE which sell massey ferguson /eicher brand tractor has 25% market share with capacity of 3 lac/yr. ITL selling sonalika has 12% market share with 3 lac /yr capacity. Escorts another listed player has around 10% market share with ability to produce 1lac tractors/yr. Remaining players include HMT,JOHN DEERE,VST…etc.

Having worked in Tractor industry, my thoughts are as under.

Small tractor of VST is used mostly for inter-culture of Sugarcane & cotton in Maharashtra & Gujarat resp. However VST has big competition from Kubota who is market leader in this small segment. Every other competitor has identified this niche segment which has market size of around 40,000-45000 annual from 6 lac tractor industry. So every competitor has either collaborated with small tractor manufacturers ( Field Marshal with Mahindra with model Yuvraj, Tafe has collaborated with Captain) or bringing their own model as Sonalika has done. However Kubota has well identified customer needs in this segment & their both Models B 2420 & A211 are selling more.

I think VST is doing well from product point of view in Power tiller.

Tractor industry is divided in various market segment by HP of Tractor.

31 to 42 HP- 2 to 2.5 lac

42 to 50 HP- 2.5 to 3 lac

Above 50 HP- 50000 to 60000 nos.

Below 30 hp- 40000 to 45000 nos.

Buying decision of tractoris based on how much acre field farmer owns or to be cultivated, finance available, mileage & productivity of tractor, brand name & presence of strong dealer.

There is tough competition in tractor market. A small example is, John Deere even though number one in world, still has market share of 8.5% in India since year 2000.

31 to 42 HP segment has less margin & is volume game segment while as we go for higher HP, there is scope for higher margin. This make dealers to push for higher HP tractor in market.

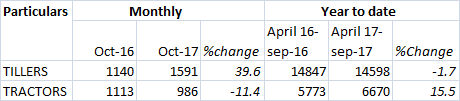

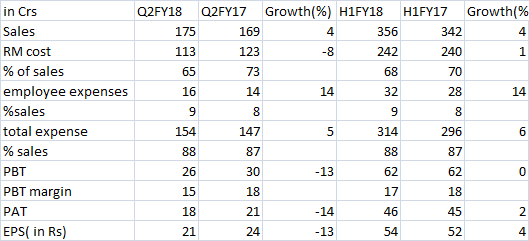

Net revenue for Q2 is 175 cr which is growth of 4% YoY v/s 159 cr. Lower revenue growth is due to lower tillers sales and GST impact. Operating margins are low due to increase in employee cost/other selling expenses. Focus is to grow top line which may improve in H2. Selling expenses are likely to remain high with launch of new products. Margins likely to improve by 1% if the sales increases in H2FY18.

Tractors: Revenue from tractors is 89 cr in Q2.Sold 5,684 tractors in H2FY18 v/s 4656 in same period last year (3,159 tractors Q2 v/s 2,555 in q2 fy17). Growth of 22% compared to industry growth of 14% in compact segment. No of 27 hp tractors sold is 1,230 in H1FY18( 849 IN Q2FY18). Market share in compact segment is 15% against 14% last year.

Expect the tractor segment to continue good growth in H2FY8. Working on new product variants.

Tie up with Kukje Machinery ltd for higher HP Branson tractors. 47HP tractors will be launched in phased manner.

Phase 1: will be marketing entirely imported unit . During this time vst will obtain necessary Govt approvals.

Phase 2: components will be localized and sold in market by next year end. Investment of around 18 Cr for the same.

Phase3: Fully indigenous one including engine will be manufactured.

Target to sell 11,000 to 12,000 tractors in Fy18.

Tillers: Revenue from tillers is 88 cr in Q2. Sold 5,888 tillers in Q2fy18 v/s 7,119 in Q2fy17. VST market share is 62% compared to 61% in fy17. VST had negative growth of 5% in 6 months against industry growth of -7%.

Lower tiller sales is due to unseasonal rains in Karnataka and delay in release subsidy in certain states. Ex. Andhra has launched DBT scheme. Orissa has increased no of permits for tillers. Better monsoon/rain during September will drive further tiller sales. Expecting better tiller sales in H2.

Overall tiller market to grow in single digits . 12 HP tillers contributes to 90% of tillers market.

Vst will be launching 15 HP tiller. Expected market size for the same is around 5,000/year.

Target to sell 27,000 tillers in fy18.

Not much changes in Chinese tillers growth. Kuboto has been gaining market share.

Working capital may slightly get better( by5days) by year end with release of subsidiary by states like Karnataka/Andhra and Orissa. Most of the price contract with Govt is for one or two years and will be revised accordingly.

Sales data shows excellent growth in tillers probably aided by good mansoon across southern states Govt subsidy/DBT also would have played key role. Central Govt making certain regulations like mandatory CMVR must have helped indirectly by reducing chinese import.

Tractor segment which has been focus area for company and expected to drive the revenue has degrown for the quarter. Other players like Mahendra /Escorts continue to show good growth in tractor sales.

I and @ananth visited VST office. Few points from the interaction(there may be few mistakes while noting down) TRACTORS: Q1: What is market size of 47 HP tractors . How many tractors we are importing from Kukje ltd. Revenue agreement with Kukje. Selling price and expected ebita margins. Target sales no in next one or two yr after launch?

A: Total market size of 30-50hp is 6.6 lac tractors/yr. 31-40hp tractors is 2.7 lac/yr. 41-50 hp: 3.4 lac. Premium segment (47hp): 1lac(30%). We will be entering the premium niche segment of 47 HP with VST Branson brand and competing with players like John dheere/escorts…etc. VST has paid upfront(?amount) to KUKJE for technology. Royalty of 40$/tractor( approx:2.5k) sold will be paid to kukje. Waiting for CMVR approval from govt. Process is on, likely to get approval by July/Aug subsequently it will be launched.

We already imported 10 tractors. Initial phase 250 tractors will be imported completely from Korea. Target is to sell 150 tractors by end of 2018. Initially it will be loss making for the company. Subsequently in phase II all the components will be indigenised except engine and target is to sell more tractors by end of 2019. In phase two it will positive for the company. Selling price of these tractors will be much higher than present tractor price… Q2. Kukje ltd 25 R series has 35 to 60 HP. Our agreement is only for 5025R? that means only 47 hp tractor? Not any other higher range HP tractors?

A: Agreement with kukje is for 5025R series only that means only 47 hp tractors not any other higher hp range. Q3. After sales service is one of the important factor for farmers. How you are preparing our dealers for the same considering its new technology/imported one.

A: In order to prepare the dealers to provide after sales kukje team is visting vst and updating/sharing knowledge about new brand/technical aspects. VST team also visiting Korea to learn about the same. Q4. Why/how did u select Kukje co. Any specific advantages.

A: Kukje was approached by VST 5 years back but things didn’t materialise then . With new CEO/management they were also looking for new markets . Finally we could reach agreement with them. We were in talks with one Japan company for the same purpose but it did not progress. Kukje Branson has good brand. They have various other agri equipements which we may launch if something materialises but nothing planned as of now. Q5. Till what HP we have own technology to launch tractors. What are new variants of tractors we are working on presently (other than 47 HP)? Anything in pipeline for this year/next year launch.

A: VST can launch 30-40 hp tractors by own technology. Will be launching other higher hp tractors hp tractors by the end of 2018. For these higher hp we will using engine from Kirloskar. 30 hp tractor will be launched in present year. Most of these new launches will be done at NASIK. Farmers at Nasik are more demanding. You will get immediate feedback for the product. If we succeed at Nasik it will easy to do the same in other parts of country. Q6. Low hp tractors are preferred by sugar cane/cotton farmers in Guj/Maharastra due to advantage of low width where VST has significant presence. Why we could not replicate the same in sugarcane growing areas of Karanataka/Tamil Nadu and cotton growing areas of Telangana/Andhra. How VST is growing in UP which is another important sugarcane growing area.

A: We are not only strong in Guj/Maharastra but also in AP and karnataka. UP which is a big tractor market where our presence is less . More demand from UP will come once we launch higher HP tractors. Our new dealer in UP doing well. Andhra most of tractor sales happens through govt subsidy for low HP tractors. Q7. When all other players registered significant growth in tractors VST tractors sales have been flat during last few months in spite of significant rise in selling expenses from last year. Please let us know the reason for the same. How is our tractor sales going to be present /next quarter.

A: After launching Virat+/Samrat tractor ,received feedback from farmers about problem with gear box.(Virat is having 8+2 gear box. Samrat is single cylinder engiene competing with Mahindra yuva). VST wanted to solve this issue before pushing for sales. It took some time to solve /problem with supply chain and now started bulk supply from December. Wanted to reduce the stock/receivables from dealers which was increasing, it also impacted the sales. Guj elections also impacted the sales through subsidiary which is restarted from mid JAN. Going ahead tractor sales will improve. Q8. This year our target to sell 11000-12000 tractors . Next two- three years how many tractors we can sell ?

A: We should be selling 11k tractors by fy18 end. Target for fy19 is to reach 14.5k . With all the new launches/higher hp tractors planned our total tractors sales will be much higher in next two-three years and our target is to gain overall market share of 3%. Q9. Any significant progress in exporting tractors. No of tractors this yr. Expected EBITA margins?

A: Export of tractors this year is not good due to issue with EU homologation. Exported around 170-200 tractors against target of 500. In Fy19 target is to export around 500 tractors. Q10. What is the major raw material component? % of metals/tyres/battery for total cost? impact on margins.

A: Steel constitutes major raw materials (70%),tyre cost is around 3 to 4%. Steel cost has gone up significantly. Our margins will be affected by 2 to 3%. Could not pass on the rise in cost to farmers due to stiff competition in market. Competition in low hp segment is increasing with all major players entering the compact segment. Q11. Tractor EBITA margins as per different HP segment.

A: 22HP tractor has margin of about 18%. 18HP margins are around 14%. 47 HP after one year may reach 12-14% which can further increase with indigenisation.

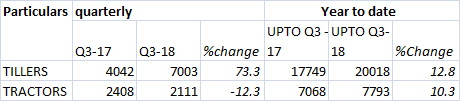

TILLERS: Q12. Last three months tillers growth is impressive (70%) but on a low base due to demon of q3fy17. If we compare with q3fy16 tiller growth will be around 12% only which is still good. expected growth rate for tillers next 1 to 3 years.

A: We should be able to sell around 28k tillers this year. Its mainly driven by Govt subsidy. With Govt supporting farm mechanisation tillers should have decent growth going ahead. Marginal farmers should be supported by various measures /by removing middle men so that they get benefit and continue with agriculture. Q13. Any new variants in tillers launched by VST in jan ? what HP? Market size. 12HP higher selling tillers - 50000 units makes up for 90% of tillers market . Who is strong competitor for us/any new competitor in this segment.

A: VST will be launching 16 HP tillers in MAY 2018(which is delayed a bit). Market size for the same is around 5000 tillers. Q14. Any significant change in Chine’s tillers growth after Govt mandating Batch testing/CMVR before subsidy. Measures from GOVT to promote mechanisation /tillers and comment on competitor products.

A: Govt has taken certain measures like mandatory batch testing/CMVR for tillers. Other things which is proposed by VST/ongoing discussion with Govt is to fix minimum price for the tillers and makes 2yr mandatory period. These measures should help VST . We have better quality tillers with good service to farmers.

Chinese players market share has reduced to 15% from 24%. Other players like kirloskar(14hp tiller) seems to be good and found good response from dealers/farmers. Honda seil has has rotay tillers of 5HP/7Hp but nothing much about products. Kamco, being a govt company doesn’t seems to be doing much with its 12hp/8hp tillers .Kubota tillers price is higher.

OTHERS QUESTIONS: Q15. DBT Scheme how has it progressed. Is it really implemented in any state? Orissa this year - is it happening fast? Other states following modified DBT? Do we expect receivables to come down dramatically in next few years due to this?

A: Orissa DBT is fully implemented. Andhra DBT is in force from last 2-3 months. No others new states have implemented DBT scheme fully. With elections in next year, its difficult to tell how Govt will take decision about this. Once DBT gets fully implemented our receivables should be down by 20 days. VST has good relationships with Govt authorities to manage receivables/subsidy and price negotiation. Q16. Are we going to stop manufacturing tillers at Whitefield over next few yrs. Management view for possible monetisation of land and progress of new plant at MALUR.

A: New plant at Malur is nearing completion and will be inaugurated in few months. Will be shifting the tillers capacity (not completely ) to new plant. Whitefield plant will be utilized for production of higher HP tractors as it requires separate line which is not possible at Hosur tractor palnt. Monetising of whitefield land is unlikely in near/medium term. Q17. Any new launches in Agri equipment sector from VST expected? self propelled power reaper ? how big is market size vs competition ? Can any of these have significant impact on revenue?

A: Other agri equipment products include VST/MTD power weeder( US company product) which is marketed by us. FY18 will sell around 800 power weeders ( total market size may be around 5k). Weeder cost is around 82k. This is also driven by Govt subsidy. Along with reapers/ attachments of tractors and tillers the contribution to revenue should be around 10% of sales in next 3 years. We have around 50 attachments for tractors and 30 for tillers. Q18. How many hires we have done in past two years that caused employee cost gone up ? Present dealers no (total/tractors/tillers and combined). How is the plan of expanding dealer network progressing. Main focus is to increase tractor dealers?

A: Presently have around 300 dealers . Common dealers: 130. Exclusive tractor dealers and tiller dealers 260 and 220 respectively. Target is to reach 400 dealers with majority additions being tractor dealers. Around 120 people hired in last two years for strengthening R&D and other departments. Current employee cost is around 8.5% which will come down to 7-7.5% once sales growth is acheived. Q19. Update on CHSC tender by GOVT of Karnataka. VST getting benefitted from the same like previous tenders.

A: VST is not participating in CHSC this time as it was found to be difficult to manage/loss making for dealers. Those who has taken franchise during earlier tenders seems to be loss making during last two years.

VST continued good growth in tillers sales for the quarter and year. Tractor sales are back after tepid Q2 sales due to various reasons as mentioned by management. Overall it was excellent FY for tractor industry with Mahindra and Escorts recording growth of 21% and 26% respectively.

I have gone through the company profile and related information. In my opinion,it’s a good investment keeping in mind the government’s emphasis on increasing income in agricultural sector.The numbers and ratios keep on changing due to so many factors,but when there is combination of strong brand equity,growing sector and healthy financials the company usually provides good returns in a reasonable period-in this case I suggest a five year period (keeping 2022 in mind).