ANALYST MEET - from Capital Markets

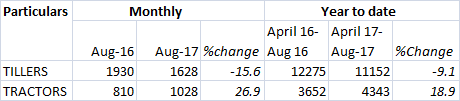

Hopes to do sales of 10000 tractors in FY 2017 against 7700 in FY 2016 and tillers should grow 15%

The company held its investor meet on 11th June’16 and was addressed by key management

Key Highlights

-

Typically a Power Tillers costs around Rs 1.25 lakh as compared to tractors which start at around Rs 2.75 lakh onwards and goes on above Rs 10 lakh depending upon the HP power and specifications.

-

Due to fragmented land and large number of unit farms, Power Tillers remain the most suitable equipment for the farmers having such unit farms and fragmented land. For implementing farm mechanization also, Power Tillers are best way to start with.

-

However the market is more driven by subsidy schemes run by States and is more from push model than on pull basis. As per the management, though through education and awareness, the importance of Power tillers is getting understood, but the capital subsidy plays a significant role in generating the demand.

-

VST Tillers has market share of more than 50% in Power Tillers market in India.

-

The company has an installed capacity of around 60000 units of Power tillers and around 36000 units for tractors. The company is operating around 70% of installed capacity for tillers and less than 25% for tractors. The company has assembly type operations which help it to scale up and scale down its operations depending upon market conditions.

-

In tractors besides entering new markets, the company has launched 2 new models of 25 HP and 30 HP. Currently the company has market share of around 12-14% in less than 30 HP market. The market did not perform well due to lower than expected rainfall in past 2 years, but with the expectation of normal monsoon, there is a pent up demand visible for the segment. The company is expected to sell around 2000 tractors in June’16 quarter up by around 20% on YoY basis.

-

As per management, while this was more to do with the inventory built up by the management, going forward, if the rainfall is as per the planned, then the double digit growth can continue.

-

The company operates in a highly competitive segment in which cheaper Chinese tillers pose a great threat to market share of other organized players. Further lot of other domestic players has started entering this segment looking at attractive returns. Hence competition continues to remain a challenge.

-

For Tractors, Maharashtra and Gujarat continue to account for 75-80% of company’s sales but contribution from the other states will increase going forward. In two years the company expects Maharashtra and Gujarat should come down to around 50-60%.

-

For Power Tillers, apart from Andhra Pradesh, Telengana, Tamil Nadu, Karnataka and Orrisa, the company is entering into new markets for increasing its reach and presence.

-

Orissa has come up to be a major market for the Power Tillers. However the company did lost some market share due to increase in competition both domestic and from Chinese.

-

Going forward, a higher penetration policy and increasing new markets and newer products will drive the sales growth.

-

FY 2017 is expected to be normal monsoon and thus hope that tractors will see good growth. Thus it should do sales of 10000 tractors in FY 2017 against 7700 in FY 2016 and tillers should grow 15%.

-

Subsidy receivable from government sales is Rs 45 crore.

-

Africa is a good market for power tillers but it is dominated by cheap imports from China. The company is not able to compete with Chinese companies there.

-

The company does not have any acquisition plans and is sitting with net cash of more than Rs 150 crore.