Concept of averaging is never a nad idea however you have to 99.9% sure of knowing the things happening in sector, stock. Once invested and have conviction, i just go and do averaging in stocks i have selected in core portfolio, you should be happy as aquisition price go down hence return in investment go up.

Hi @homemaker

I would like to add that I am in the startup phase of my investments - so ones strategies should be aligned to ones experience in the markets. Typically beginners like myself enter the markets with half baked know how and are ignorant about important aspects of investing. To cross the chasm one needs rules that protect you in this phase from too much harm as mistakes are inevitable. One should be flexible and discard notions that don’t work and retain the ones that do.

As one acquires skill to avoid the bad apples , the good apples pile up and then you can breathe a sigh of relief. No seasoned investor I know uses 15% exits - but that’s due to their better abilities at picking winners.

Best

Bheeshma

2 Likes

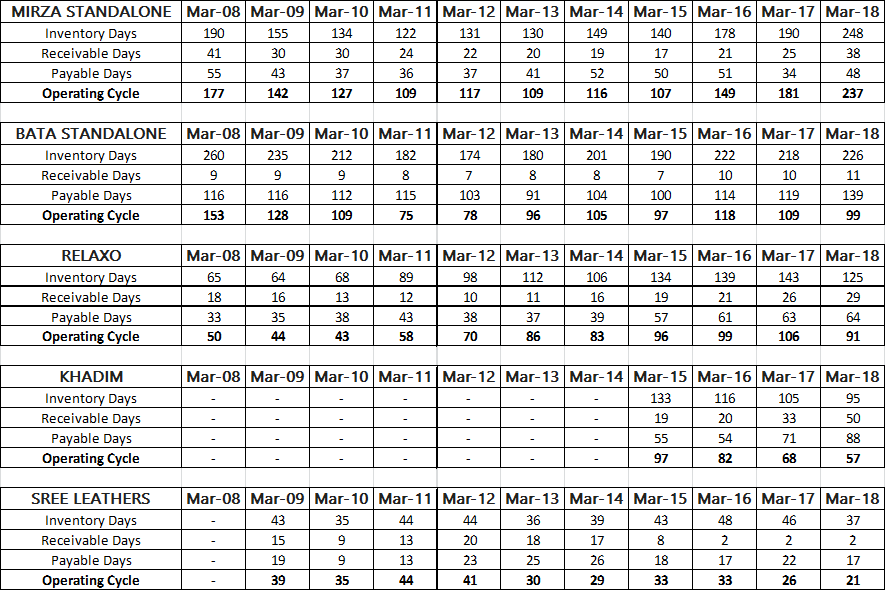

This is one of the. Best article on working capital changes with some practical example

I always study cash flow and working capital changes before investing and this article given me lots of awareness on this topic , read it numerous times

Hope it may be helpful to you also

Thanks

Ashit

7 Likes

Thanks @ashit

Yes, looking at WC changes and movements holds a lot of promise as a tool to identify well run cos. Looking at the operating cycles of footwear cos for e.g - one can easily identify the ones facing issues from the ones that aren’t

14 Likes

hi @bheeshma Thanks for the sheet. Shouldn’t we be careful about the companies which operate with the borrowing? The sheet has taken the borrowings into account. If the borrowings are high & cash flows/cash is not present then it should be treated as negative, right?

receivables days is calculated by dividing receivables by sales * 365. since sales also has the profit component of any transaction, it is used as the denominator when calculating “days”. so its like to like.

on the other hand, the denominator for calculating inventory days and payable days is cost of sales (or cost of goods sold) because that is the financial value (cost) incurred to generate that level of inventory and payables.

hence i am not quite clear what you were trying to say when you said it cant be taken from the balance sheet and has to be estimated.

The receivable days as you said is like to like. However, the figure of receivables present on the balance sheet has a profit component. Do let me know if am making a mistake somewhere.

If cash flows are insufficient to cover WC then the co will need to resort to borrowing. If that situation continues for a while then the co will be in a soup else it will need to scale back.

1 Like

James Simmons - undoubtedly the greatest quantitative (read mathematical) investor of our times

He ends his talk with his 5 guiding principles

- Do something new

- Collaborate with the best people you possibly can

- Be guided by beauty

- Dont give up

- Hope for some good luck

4 Likes

This is a short writeup by a friend of mine on his 3 month learnings on the stock market. He is not the one to dabble in the stock market at 41 but he did and this entertaining account not only contains some good genuine learnings but also is useful for some vicarious experience. Not to mention he is an extremely good writer. For those who want to reach out to him do ping me.

The Lockdown Robinhood.pdf (642.3 KB)

5 Likes

Nice Article He has nicely explained the process, Thanks for sharing

insightful presentation…thank you for sharing it

Dear @bheeshma Bheeshmaji,

Sorry that we don’t see your posts in this forum often. I spotted this and read it after 3 years!

Since he looked at an investing horizon of 3 years, i would love to see a sequel to this story to see what happened, so far.

Also, like to see the how your journey as an.investor progressing.

1 Like

Hi James

Thanks for the reply. I’ll ask my friend to write a sequel and post it here!

As for my journey - In the last 6 years - I have witnessed several market downfalls and seen a significant part of my networth getting eroded and… coming back up again.

Some of the painful memories are exiting early from many multibagger cos - I bought Safari at 400 levels and exited at 600 and last i checked it was at 4500. Then others are HLE glascoat, Dmart, Technocraft Industries, Axtel and many more

Some good calls are RACL Geartech, ADF foods, GRSE, HBL, TD power, REC which have given handsome returns.

Some learnings which if you go through all the threads you would already know so nothing new

-

The golden formula for multibaggers is low PE + explosive earnings growth. Several cos like ADF , RACL etc were purchased at a PE of 10 - 12. High PE is actually a low PE if the co is going through a rough earnings patch and Low PE is high PE if for some reason earnings are unnaturally high as is the case with many packaging film cos like Cosmo.

-

Try and allocate as much as you can - you can lose only that much but upside is manyfold

-

Have a look at the chart even if you are a pure fundamentalist - some price patterns keep repeating and it helps many times

-

Return on Equity is the main driver of share prices in the long run. Try and invest in cos that have a good ROE (18%+). Price to Book ÷ Price to Earning = ROE = Margins x Turns x Capital Structure. One can clearly see the link ROE plays between market prices and Business Performance through this formula. The co that comes to mind currently is Premier Explosives which is has gone from Low ROE to High ROE in the last few qtrs and market prices have followed suit. If you ask the owner of any business they will invariably be looking for highest margins with lowest capital being locked up.

-

Simple things work best , avoid complex discussions, complex cos and complex math. I remember doing some complex calculations for Mirza and not investing. For a while it felt intellectual and share prices also tanked so I felt vindicated. However , look at all the wealth it has created over time esp after the demerger. Lesson learnt

-

Act quickly when the chance arrives and don’t chase prices (up or down). So what if some get away there will always be chances. Be sure you are not overpaying.

-

In general , market sizes are small in India (5000 crores or less) and those big juicy massive market sizes exist only in a handful of sectors.Try to estimate market size first. If one gets a sense of the total earnings pool then the overall market cap of the sector can be calculated and compared with the co in question. Also that’s how businesses decide to enter a market , there should be enough revenue potential in a market to launch a product. I remember RJ and RD describing their call of investing in United Spirits. You were getting a market size of 20,000 crs in some 300 crores at one point.

Thats it! It’s great to be a part of VP and though I have been little less active I read all messages daily that people post here and pick several ideas from this forum

The Collab corner esp has some great writeups and contributions on businesses and their triggers.

13 Likes