Hi @Vivek_6954,

Any thoughts on the upcoming NSE SME IPO (secur credentials)?

Seems to be niche company on Background checks services , sales appear to be on path for doubling (or more) compared to last year, priced around 12-16 PE .

There are no listed peers in the market.

Funds look to be completely used for future business expansion needs…

2 Likes

Sorry missed your message.

On close reading SCPL seems to be an interesting company with several positives. Did u apply in the IPO? Price is still in reasonable range . Whats your take on co & sector? How much are margins N can they improve? Any other point you may like to highlight?

Not yet studied it. What all u like in the co?How is the promoter n business quality? any concerns?

My concerns… Is it common that all board of directors are inducted less than an year ago? One of them is just a matriculation. Minor civil litigations.

Positives… Better PE, high growth industry, niche business.

SCPL :

Any one from Gujarat can help , How their products are except in the market ? Again lots of potential in the very competative industry.

It seems fairly priced to me around 40+ times earnings.

1 Like

SCPL Promoter though not highly educated seemed workaholics who understand their business well. CAGR & RONW is good.

With easy power availability in Indida & co plan of expansion icecream n other related food product consumption is bound to grow.

FMCG cos trade at higher valuation.But we need to dig more n do more scuttlebutt on co n promoters.

All help from Saurashtra n Gujarat based VPers is most welcome n will be v useful.

-

Factors in support :

- Nascent industry , no listed peers.

Increasing numbers of industry sectors seem to be adopting this service as an HR practice.

Both National & International presence

Promoter holding is 74%, so he seems to have his "skin in the game " …

EPS for the period ended June was 4.18 ( If this is indeed only for the June quarter AND one can extrapolate this to the entire year,

the company is available at a PE of (205/(4.8 * 4) = 10.6) which is quite reasonable & leaves something on the table post listing. -

Risks: Very small company, so no economy of scale benefits

Management has indicated high working capital requirements, negative cash flows have been encountered (such as june 2017)

Data is this company’s raw material. So any hacking of its database could be catastrophic.

Also, any changes in the IT ACT esp in the privacy related laws, might adversely affect this company

Couldnt find much info on Rahul Belwalkar,CEO. So not much idea on promoter reputations but is of age 43.

I will decide whether to invest on nov 3rd, based on the subscription status.

2 Likes

As June quarter is peak summer quarter, extrapolation of EPS of June quarter may not be appropriate.

Summer quarter - I don’t Understand nthe logic. The above comments pertain to Secur service ipo

Thats some run - great job. 12X in 5 years is a CAGR of 65. Thats incredible.

Just curious though - Has the X in 2012 has become 12X or does it also include new money that has been added to the portfolio over the last 5 years?

It was about SCPL, I understood it as Sheetal Cool Products Ltd.

I feel whole FMCG sector is trading expensive …

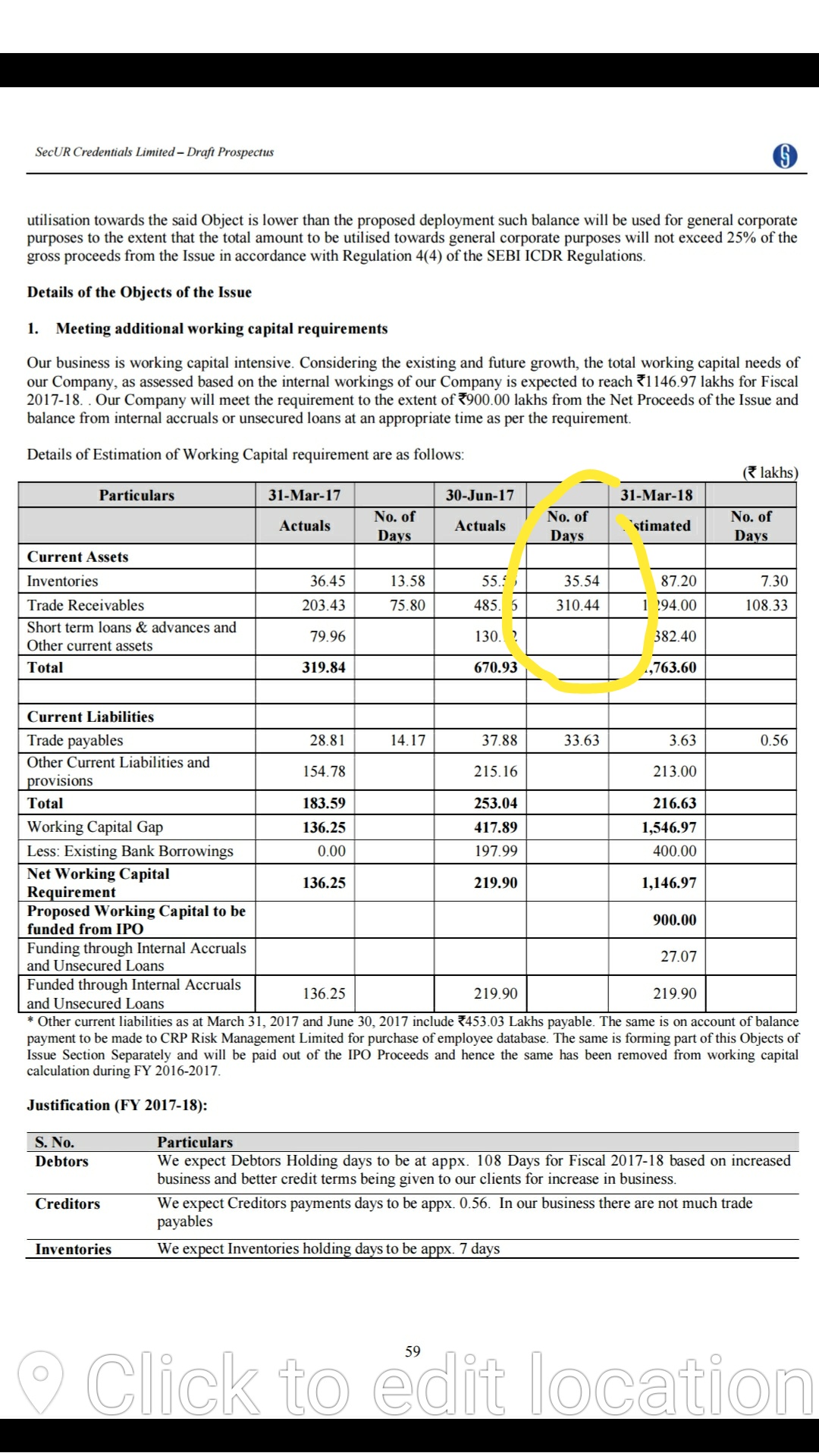

My notes from the DRHP of secUR

• Total outstanding shares : 0.48 cr ( post listing)

• mcap would be roughly 100cr ( at 205/share)

• At Fy17 net profit of 1.8 cr : PE 54 times

• Taking net profit of 1.24 cr of June quarter : PE comes to 20 if we extrapolate it into full year, (EPs : 1.24x4/0.48.)

The good:

• niche business

•. No listed peers

•. Catering to multiple industries

• Data driven business( data being the new gold as I have heard often)

•. Sales have doubled since last year from 4.4 cr to 10.16 cr mainly by exports which were nil before and now account for almost 50%

• asset light

• promoter not taking salary

**The bad:

• high trade receivables and consequently working capital requirements. From receivables days of 75 days in March 2017, it has grown to 310 days in June. Estimated year end stands at 108 days.

• negative operating cash flow due to above ( in June quarter).

**Total debt:

Working cap loan: 1.97 cr

Loan from promoter: 54 lakhs( interest free)

**Use of IPO proceeds

- 9 cr for working capital

- 7.28 cr for symphony ( which seems to be the database and operating system for their purpose)

PS: at current valuation there seems little comfort in applying IMHO, though it may be lapped up in the raging bull market with a niche player. Will think it through.

5 Likes

secUR: Is it really worth to have a 100 cr marketcap for a company with 10 cr sales?

1 Like

That’s a question ,I cannot answer.

They have done 10 cr sales in June. My estimation is they should so 25-30 cr this fiscal as export is going to be major component this year. That would still make it 3 times sales. If they do 30 cr , their PAT margin is 21%, so their Fy 18 EPs comes to be 13, giving a forward pe of 15. Anybody’s guess is as good as mine, with regards to valuation.

1 Like

Not much addition to X of 2012 as I dont have any business/ investment in FDs or for that matter in mutual fund which would have been maturing & invested. I am a direct equity investor.

Like most salaried employees out of 30 days I was working for GOI for 12-15 days thanks to IT & other taxes.For another 7-8 days was working for Axis bank to payoff EMI for a 2nd home I had foolishly bought at peak of 2012 in NCR. Rest of the days of month went in school n college fees and other running expenses of household.

Just imagine the amount which I invested in 2nd apartment is not even 1 X but has depreciated & virtually impossible to sell. Had it been added to my investible X of equity returns would have been even better as allocation matters.

Offcourse I have to thank bull market & domestic liquidity for a good performance of my portfolio.

11 Likes

IMHO best wealth is created when you bet on a first gen workaholic ethical entrepreneur with growth mindset who executes well. We will find many such examples in Gujarat. But SCPL is still a small co .We need to evalaute its performance over next few qtrs,Discl- I have a small exposure to SCPL with a 2 year POV.

2 Likes

Vivekji, does strong HNI interest in reliance nippon IPO indicate the fireworks at the time of listing? Like what we have witnessed in indigo, avenue supermarket etc. What does it implicate? Your view please… Thanks.

Receivable are only 78 days as on 30/06/17.